Stock markets around the world head towards new highs. And this is not surprising because recent economic data and surveys suggest that there has been a pick-up in activity in the advanced capitalist economies last month. Despite weak employment figures in the US last week and very weak GDP figures for Q2 (see my post, http://thenextrecession.wordpress.com/2013/07/31/the-us-economy-bigger-but-not-healthier/) , it seems that the US had a better July.

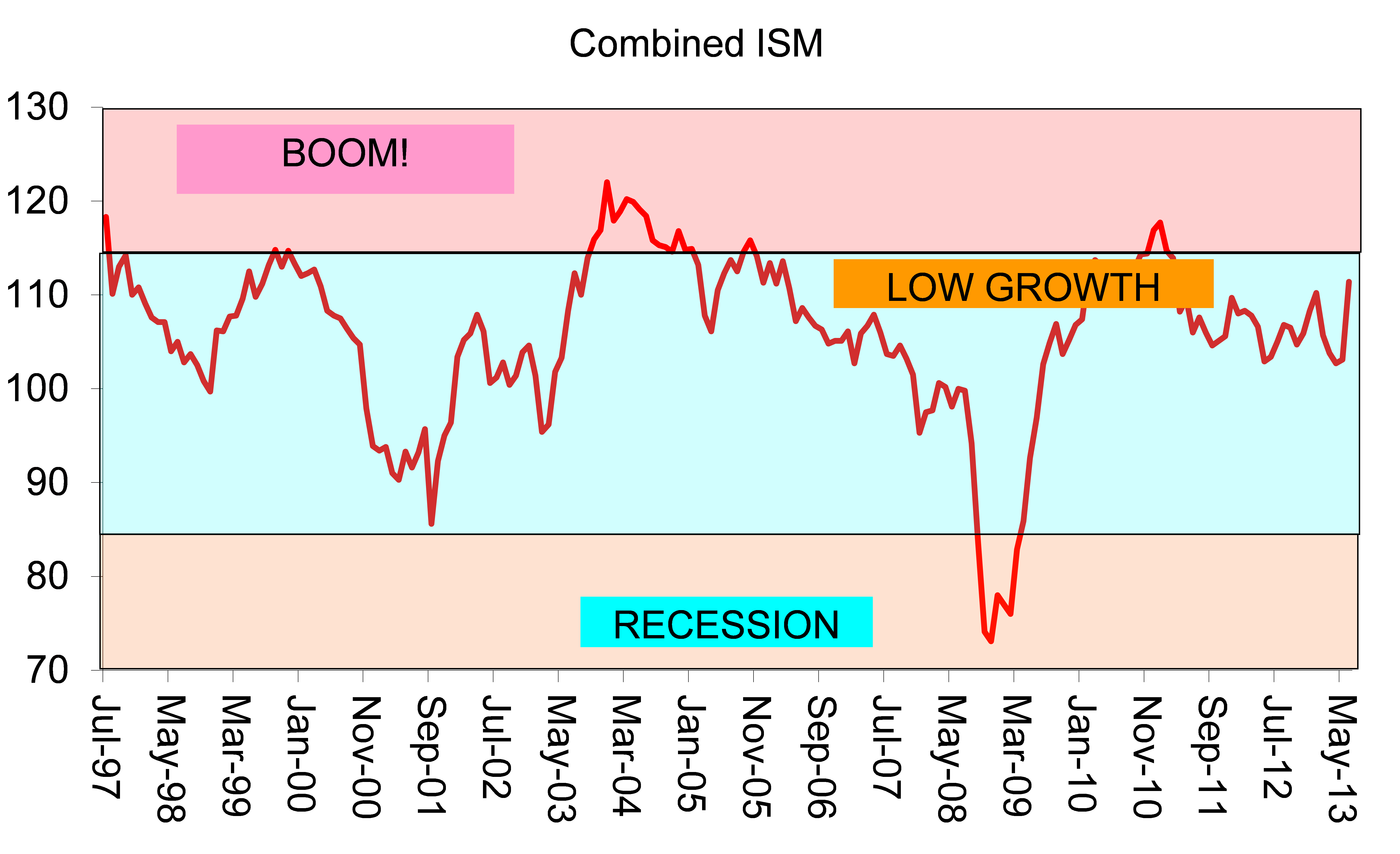

My measure for US economic activity – a combined ISM index for manufacturing and services sectors – ticked up in July.

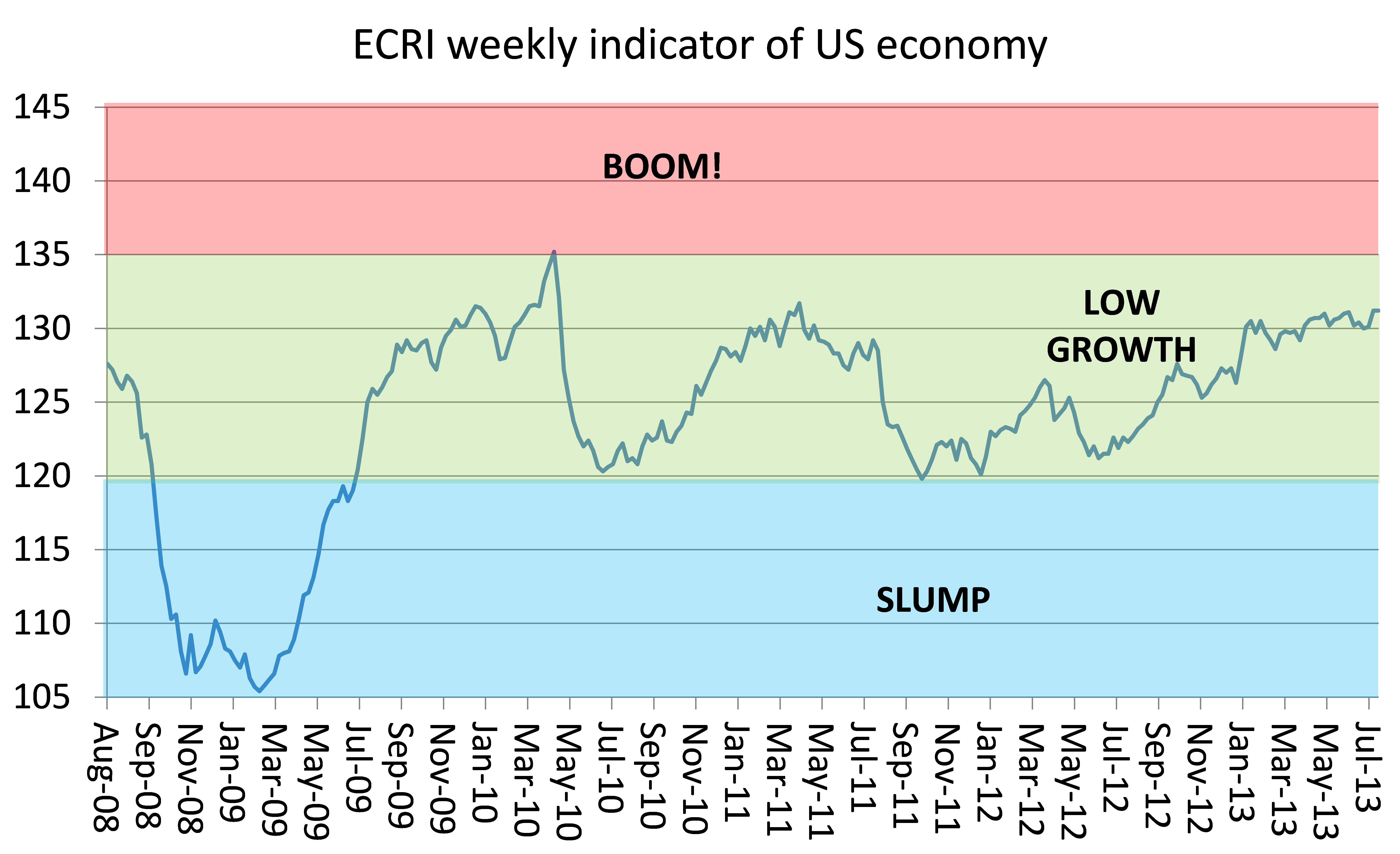

The more frequent but less reliable ECRI weekly indicator of US economic activity also supported that trend.

And for the first time since 2010, the purchasing managers’ indexes (PMIs) for the major economies all rose, even in the Eurozone, which is no longer contracting. The UK PMI in particular leapt forward after several quarters of stagnation, if not contraction. Indeed, the pace of expansion is the fastest since 2006..

But don’t get carried away, like the stock markets are. The PMIs just show the pace of expansion or contraction not the level of manufacturing output or services growth or decline. All the UK PMI shows is that the UK economy is growing at last after stagnating. Indeed, real GDP growth is still likely to be little more than 1% this year. And UK manufacturing is hardly cracking along.

At the same time, manufacturing PMIs for key emerging economies indicate that the pace of growth is slowing, not accelerating.

Overall, world GDP growth is modest at best, with the average real growth rate well below that before the crisis.

No comments:

Post a Comment