by Michael Roberts

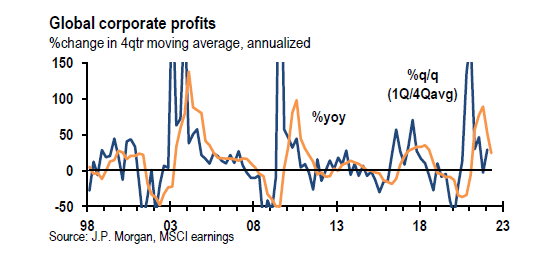

Global corporate profits growth is heading south, according to

analysis by JP Morgan economists. JP Morgan estimates that, after

surging a humungous 89% (4q moving ave) in 2021, global corporate

profits moderated to a still-solid 24% in the year ending in 2Q22. And

they reckon that “on net, the level of profits is 17% above its pre-pandemic trend, but still making up for lost earnings through the pandemic.” However, JP Morgan expects “slowing

in profit growth in the coming quarters as inflation cools while labor

markets remain tight. Additional pressure is coming from rising

corporate borrowing rates as central banks press on with the steepest

tightening cycle in decades.” The scissors of a future slump (falling profits and rising interest rates) are beginning to close.

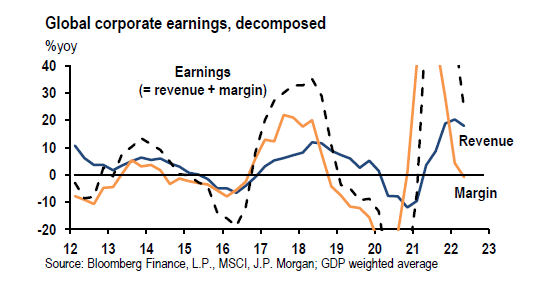

During the post-pandemic recovery, corporate profit margins (that’s the difference between revenues and costs per unit of production) reached multi-decade highs as the surge in inflation boosted corporate pricing power while wages languished.

But things are changing in 2022. Profit margins are sliding down as costs of production rise and revenue growth slows.

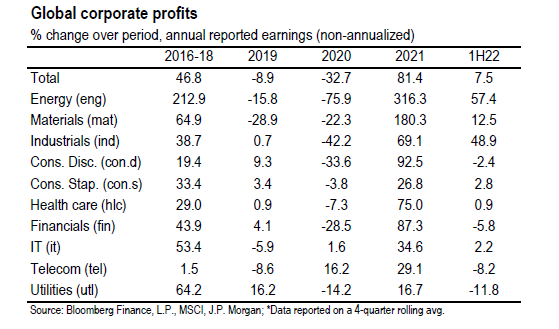

When broken down by sector, JP Morgan finds that each of the 10 sectors comprising the total economy show a slowing in earnings growth from multi-decade highs posted in 2021, although only four have experienced outright contraction since the beginning of the year. Although the profits boom in 2021 was broad-based in all sectors, it is clear from the data that the bulk of profit gains were in energy and raw materials including food. And that’s where the biggest falls are coming.

In the past, I have constructed a measure of global corporate profits. My measure is a GDP-weighted average of year-on-year corporate profits from five countries (US, Japan, China, Germany and the UK). This is a smaller universe than that compiled by JP Morgan economists. They track MSCI corporate earnings from 29 countries. That sounds better but there are some serious caveats to the JP Morgan measure. First, it is based on reported earnings in company accounts that always exaggerate earnings. My measure relies on more accurate national government measures of profit. And second, JP Morgan measures the change in those profits on a 4q moving average, not year-on-year for each quarter. That tends to make the up and down changes more exaggerated than year-on-year measures.

On my model, the change in global corporate profits to H1 2022 looks like this:

Several things emerge from this figure. First, global corporate profit growth had ground to a halt even before the COVID pandemic broke and lockdowns and the collapse of international trade ensued (-2.1% yoy in Q4 2019). Second, the huge statistical recovery in 2021 (peaking at 54.4% in Q2 2021) has now given way to a fast slowdown in year-on-year profits in 2022 (to just 6.2% in H1 2022).

How does the JP Morgan model compare with mine?

Considering the differences in the data between the two models, there is still quite a similar trend found. There was a boom in profits after the mini-recession of 2016, then a fall in 2019 (heralding a new slump in investment and GDP in the major economies), and then the fall in the pandemic (although my figures show a small rise). The recovery of 2021 is more moderate with my data than JP Morgan’s. The first half of 2022 is comparable.

Both data show what JP Morgan concludes, “relative to its pre-pandemic trend, cumulative global profits since the pandemic are still over 20% depressed.” And now profits growth is disappearing. JP Morgan forecasts that “pricing power is expected to ease––particularly in energy––while wage pressures are unlikely to moderate as quickly. Combined with rising interest rates, profit margins will fall, dampening overall earnings.” What I have called in the past, the scissors of slump (rising interest rates and falling profits), are beginning to close.

Why does tracking the change in the profits of the capitalist sector globally matter? As I have argued in numerous places, profits are the driving force of capitalist investment and therefore employment and income growth. If the profitability of capitalist investment falls and eventually leads to a fall in total profits, it is the strongest indicator of an impending slump in capitalist production. The close (if lagged) relationship between profits and investment is well established by several studies including my own.

JP Morgan is certainly convinced of the relationship between profits and investment, with the former leading the latter: “we expect corporate profit growth to slow further in coming quarters. This weakness will negatively feed back on business capex.”

No comments:

Post a Comment