“The war in Ukraine is like a powerful earthquake that will have ripple effects throughout the global economy, especially in poor countries”. That’s how IMF chief Kristalina Georgieva described the impact of the war on the world economy. Nobody can be sure the magnitude of this quake but even on the most optimistic view, it is going to damage significantly the economies and livelihoods of not just the people of Ukraine and Russia, but also the rest of the 7bn people globally. And it is happening just as the world economy was supposedly recovering from the plunge in output, incomes and living standards suffered from COVID pandemic slump in 2020 – which was the widest and deepest global contraction (if relatively short) in over 100 years.

But let us start with Ukraine itself. Already 3m people have fled the country from the bombs and destruction of their homes and another 6m have been displaced within the country. As with all wars, people’s lives and livelihoods have been lost. Economically, an IMF staff report, completed on March 7, concluded that the country was paralysed. “With millions of Ukrainians fleeing their homes and many cities under bombardment, ordinary economic activity must, to a large extent, be suspended.” Then there is the physical damage. A week ago, the Ukrainian president’s economic adviser put the damage at $100bn already. Half of the country’s exports rely on the port of Mariupol, which is now suffering the most savage siege.

The IMF’s tentative projection is for output to fall 10 per cent in 2022 — if the war does not last long. And that is beginning to look optimistic, as the IMF comments, “Downside risks are exceedingly high.” This 10% compares with a decline of output of 6.6 percent in 2014, which was followed by a decline of just under 10 percent in 2015, during the earlier Russia-Ukraine conflict in Eastern Ukraine. However, the IMF warned that “data on wartime real GDP contraction (Iraq, Lebanon, Syria, Yemen) suggests that annual output contraction could eventually be much higher, in the range of 25-35%.”

Then there is Russia. Putin’s invasion has provoked an unprecedented response in the form of economic and other sanctions against Putin’s friends and supporters and against its banks and institutions, even leading to the seizing of the country’s foreign exchange reserves – and increasing attempts to block or boycott Russian exports (including oil and gas). Preventing the Russian central bank from deploying its international reserves and making it impossible for it to liquidate its assets, is part of an economic war designed to undermine Russia’s economy and war effort. The French finance minister said that “[w]e are waging total economic and financial war against Russia, Putin, and his government”

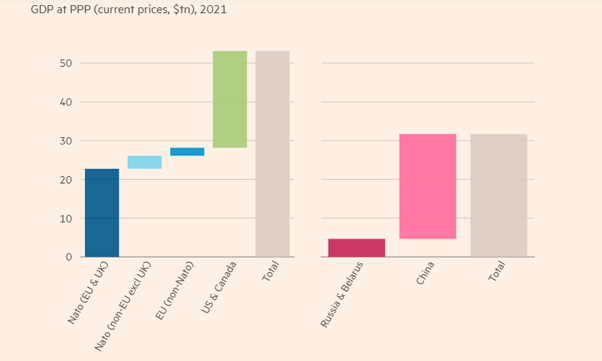

The Russian economy is not large compared to the G7 economies. In total, the economic forces against Russia amount to an annual GDP of $50trn compared to the puny $4trn from Russia and Belarus.

And when it comes to military firepower, Russia is heavily outspent by the NATO countries.

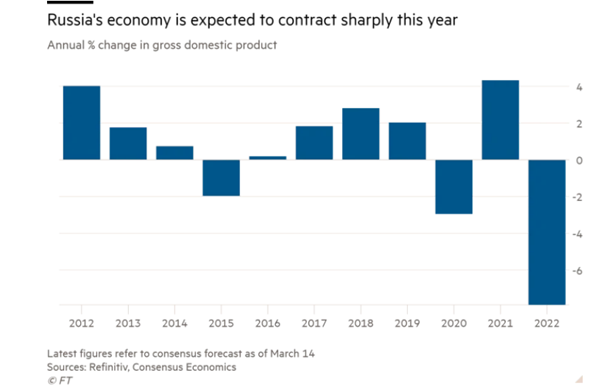

So a combination of economic disruption, NATO country sanctions and spiralling inflation is going to drive the Russian economy over a cliff. Forecasts of the output contraction vary. The consensus puts it at about an 8% fall this year.

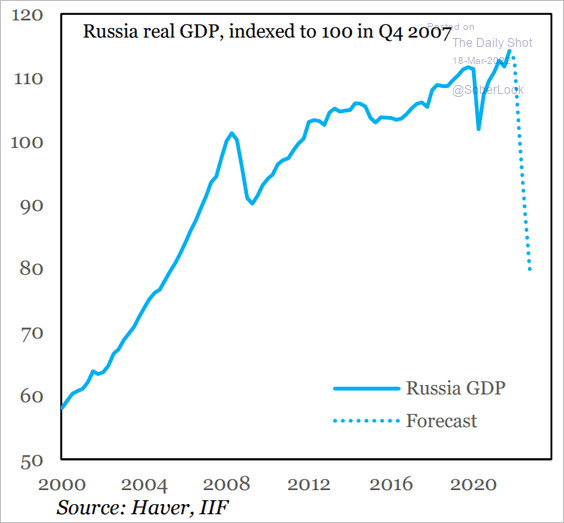

But the International Institute of Finance (IIF), which looks closely at Russian export and import flows, as well as capital flows, is much more pessimistic and expects a 15% fall – something not experienced in Russia since the collapse of the Soviet Union in the 1990s , taking the Russian economy back to levels of more than 20 years ago.

The use of economic sanctions against a G20 country like Russia is unprecedented. It shows the role that ‘sanctions’ can play as an alternative to military action against governments which do not follow the wishes and dictates of imperialism in the 21st century.

Topically, economic historian Nicholas Mulder had just published a book entitled, The Economic Weapon: the rise of sanctions as a tool of modern war. Mulder points out that economic sanctions started to be used by imperialist powers when the League of Nations was set up after the First World War. The leading powers in the League “believed they had equipped the organization with a new and powerful kind of coercive instrument for the modern world.” The then US president Woodrow Wilson described economic sanctions as “something more tremendous than war” that could bring “a nation to its senses just as suffocation removes from the individual all inclinations to fight.” There would be no need for force. “It is a terrible remedy. It does not cost a life outside of the nation boycotted, but it brings a pressure upon that nation which, in my judgment, no modern nation could resist.” In that sense, sanctions remind me of medieval sieges, where cities were starved into submission, without military action. Economic sanctions were a new 20th century weapon along with chemical weapons and nuclear bombs.

Mulder argues that economic sanctions were used first by European imperialists against peoples who lived outside the ‘civilized world’. Then the US rise to global power in the 20th century saw both negative sanctions (oil embargoes) and positive sanctions (Lend-Lease). “America’s sanctionism has been shaped by three factors: its unique military dominance, the ideological inflection of Cold War politics, and the role of US financial markets in the world economy.”

John Maynard Keynes saw ‘positive’ sanctions as beneficial, ie through aid and subsidy to the good guys, while applying bans, blockades and punishments to the bad guys. And he reckoned the financial system sanction was the most powerful – and that is now being put into practice against Russia. Of course, the larger and more powerful a country, and the weaker and less firmly it is applied by an alliance of countries, the less its impact will be.

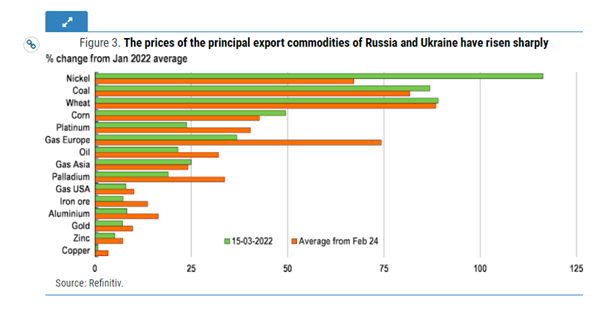

But what about the global impact of the conflict? Although Russia and Ukraine are relatively small in output terms, they are large producers and exporters of key food items, minerals and energy. Ukraine and Russia together account for more than a quarter of the global trade in wheat and a fifth of corn sales. The longer Russian forces remain in Ukraine, the longer tractors and combines to harvest the nation’s crops stay idle, it threatens food security far beyond the region, the IMF has warned.

For example, Egypt imports 80 per cent of its wheat from Russia and Ukraine. With many countries in Africa and the Middle East being similarly exposed, Europe could soon have another migration crisis on its hands, on top of millions of Ukrainian refugees. Then there is Ukraine’s role in supplying many of the rare gases needed in industrial processes — such as neon, krypton and xenon — including already beleaguered semiconductor production.

Energy is the main spillover channel for Europe as Russia is a critical source of natural gas imports.

This is going to hit output across Europe.

The IMF reckoned that “the prolongation of Russia’s aggression towards Ukraine, in addition to the humanitarian and economic losses, will also lead to significant spillover effects throughout the world: deterioration of food security, surging of energy and commodity process, rising inflationary pressures, disruption of supply chains, increasing social spending for refugees, and increasing poverty. The global economic damage of this war will be devastating.”

In its report, the OECD also presented a dismal picture if the war continues for much longer: “global growth could be reduced by over 1 percentage point, and global inflation raised by close to 2½ percentage points in the first full year after the start of the conflict. These estimates are based on the assumption that the commodity and financial market shocks seen in the first two weeks of the conflict persist for at least one year, and include a deep recession in Russia, with output declining by over 10% and inflation rising by close to 15 percentage points.”

And if energy imports from Russia fall by 20%, either through sanctions or counter-sanctions, it would reduce gross output in the European economies by over 1 percentage point, with significant differences across countries.

Management consultants McKinsey also predicted nasty outcomes for Europe’s economies, in particular. In McKinsey’s hoped-for scenario, where the end of hostilities is in sight by the second half of 2022 and sanctions do not extend into the energy sector (so that energy exports from Russia to Europe keep flowing), McKinsey reckons that GDP growth in the eurozone and Germany would stagnate in 2022, but then recover to 2.1 percent in 2023 and 4.8 percent in 2024. That’s bad enough, but if there is a protracted conflict that intensifies the refugee crisis in Central Europe and where Western countries and Russia further extend sanctions, leading to the shutdown of oil and gas exports from Russia to Europe; then the eurozone would tip into recession in 2022 and 2023, led by Germany.

And just as there was long-term ‘scarring’ of capitalist economies from the Great Recession of 2008-and the COVID pandemic slump of 2020, the Ukraine-Russia conflict is adding more damage. ‘Globalisation’ (the extension of world trade and capital flows) was an important counter-tendency for imperialist economies to falling profitability of productive capital domestically in the last two decades of the 20th century. But globalisation, the expansion of untrammelled imperialist capital flows and trade, stuttered in the 21st century, and under the impact of the Great Recession, went into reverse. World profitability fell to near all-time lows. This is the underlying cause of intensifying economic crises and geopolitical conflicts in the last two decades.

And now that this apparently ‘regional’ war that has been revved into a world issue, it could fundamentally alter the global economic and geopolitical order as energy trade shifts, supply chains reconfigure, payment networks fragment, and countries rethink reserve currency holdings. After the Trump period US protectionist tariffs against China, Mexico and Europe, now there is this increased geopolitical tension, which further raises risks of economic fragmentation, especially for trade and technology.

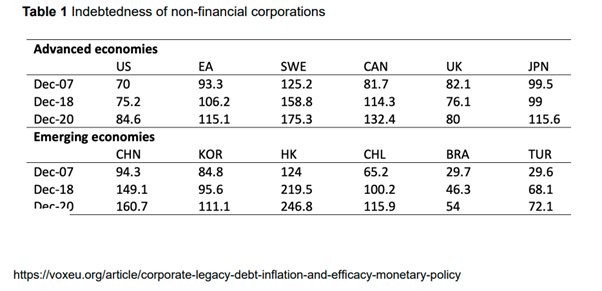

Then there is debt. The COVID-19 pandemic coincided with a further rapid increase in corporate indebtedness. Corporate debt had already been increasing globally since 2007, but the pandemic crisis has led to a further sharp increase. US corporate indebtedness rose by 12.5% between 2018 and 2020, much more than the increase in the entire decade leading up to COVID-19.

Now falling growth in output, even recession, weaker investment and lower corporate profitability, alongside rising inflation, threaten to deliver widespread bankruptcies among corporate ‘zombies’ and ‘fallen angels’. This makes the plans of central banks to hike interest rates to control accelerating inflation difficult at least, and impossible at most. One recent empirical analysis reckons that “when the level of corporate debt is sufficiently high, a contractionary monetary policy even increases inflation”, reminiscent of the stagflation episode in the 1970s after the oil ‘shocks’ then. The paper concludes that “our work suggests that monetary policy will not be effective in reducing inflation gently towards a soft landing. This means that central banks ultimately have to choose between generating a recession, with significant bankruptcies, or accepting continuing stagflation.”

‘Liberal’ economist Wolf, is deeply worried. “A new world is being born. The hope for peaceful relations is fading…. No one knows what will happen. But we do know this looks to be a disaster…....The combination of war, supply shocks and high inflation is destabilising, as the world learnt in the 1970s. Financial instability now seems very likely, too. A prolonged bout of stagflation seems certain, with large potential effects on financial markets.” In the long term, the emergence of two blocs with deep splits between them is likely, as is an accelerating reversal of globalisation and sacrifice of business interests to geopolitics. Even nuclear war is, alas, conceivable.”

Wolf claims that this war is a battle between the forces of ‘democracy’ (as represented by NATO) and the forces of ‘autocracy’ (as represented by Russia and China). This is nonsense – where does NATO ally Saudi Arabia, or the military dictatorship in Egypt, or the autocracy of NATO member Turkey, fit into this categorisation? Instead, the Russia-Ukraine conflict has exposed the increasing contradictions in the world capitalist economy between the imperialist powers on the one hand and those countries which try to resist the policies and will of imperialism.

IMF chief Georgieva pronounced that “We live in a more shock-prone world.” Yes, the shocks have been coming thick and fast in the 21st century. Georgieva continued: “And we need the strength of the collective to deal with shocks to come.” Indeed! But it is not the collective will of the capitalist powers that can deal with these shocks: they have failed over climate change; over preventing and stopping the COVID pandemic; and over ending poverty and keeping world peace. Instead, all will depend on the collective will of organised working people.

No comments:

Post a Comment