by Michael Roberts

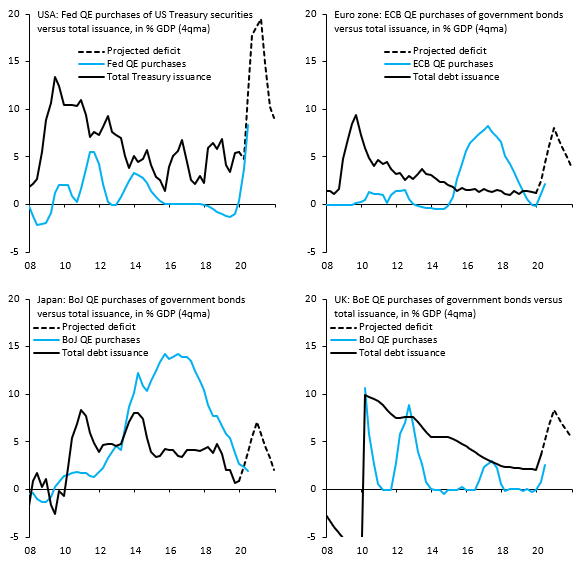

Optimism reigns in global stock markets, particularly in the US. After falling around 30% when the lockdowns to contain COVID-19 virus pandemic were imposed, the US stock market has jumped back 30% in April. Why? Well, for two reasons. The first is that the US Federal Reserve has intervened to inject humungous amounts of credit through buying up bonds and financial instruments of all sorts. The other central banks have also reacted similarly with credit injections, although nothing compares with the Fed’s monetary impulse.

As a result, the US stock market’s valuation against future corporate earnings has rocketed up in line with the Fed injections. If the Fed will buy any bond or financial instrument you hold, how can you go wrong?

The other reason for a stock market rally at the same time as data for the ‘real’ economy reveal a collapse in national output, investment and employment nearly everywhere (with worse to come) is the belief that the lockdowns will soon be over; treatments and vaccines are on their way to stop the virus; and so economies will leap back within three to six months and the pandemic will soon be forgotten.

For example, US Treasury Secretary Mnuchin, reiterated his view expressed at the beginning of the lockdowns that “you’re going to see the economy really bounce back in July, August and September”. And White House economics advisor, Hassett reckoned that by the 4th quarter, the US economy “is going to be really strong and next year is going to be a tremendous year”. Bank of America’s CEO, Moynihan reckoned that consumer spending had already bottomed out and would soon rise nicely again in the 4th quarter, followed by double digit GDP growth in 2021!

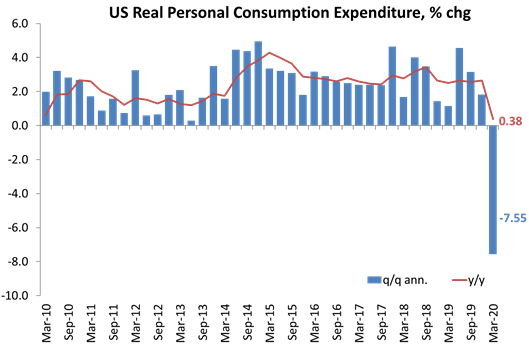

That US personal consumption had bottomed out seems difficult to justify when you look at the Q1 data. Indeed, in March, personal spending in the US dropped 7.5 percent month-over-month, the largest decline in personal spending on record.

But it’s not just the official and banking voices who reckon that the economic damage from the pandemic and lockdowns will be short if not so sweet. Many Keynesian economists in the US are making the same point. In previous posts, I pointed to the claim by Keynesian guru, Larry Summers, former Treasury Secretary under Clinton, that the lockdown slump was just the same as businesses in summer tourist places closing down for the winter. As soon as summer comes along, they all open up and are ready to go just as before. The pandemic is thus just a seasonal thing.

Now the Keynesian guru of them all, Paul Krugman, reckons that this slump, so far way worse on its impact on the global economy than the Great Recession, was not an economic crisis but “a disaster relief situation”. Krugman argues that this is “a natural disaster, like a war, is a temporary event”. So the answer is that “it should be met largely through higher taxes and lower spending in the future rather than right away, which is another way of saying that it should be paid for in large part by a temporary increase in the deficit.” Once this spending worked, the economy would return just as before and the spending deficit will only be ‘temporary’. And Robert Reich, the supposedly leftist former Labour Secretary, again under Clinton, reckoned that the crisis wasn’t economic but a health crisis and as soon as the health problem was contained (presumably this summer) the economy would ‘snap back’.

You would expect the Trump advisors and Wall Street chiefs to proclaim a quick return to normal (even though economists in investment houses mainly take a different view), but you may find it surprising that leading Keynesians agree. I think the reason is that any Keynesian analysis of recessions and slumps cannot deal with this pandemic. Keynesian theory starts with the view that slumps are the result a collapse in ‘effective demand’ that then leads to a fall in output and employment. But as I have explained in previous posts, this slump is not the result of a collapse in ‘demand’, but from a closure of production, both in manufacturing and particularly in services. It is a ‘supply shock’, not a ‘demand shock’. For that matter, the ‘financialisation’ theorists of the Minsky school are also at a loss, because this slump is not the result of a credit crunch or financial crash, although that may yet come.

So the Keynesians think that as soon as people get back to work and start spending, ‘effective demand’ (even ‘pent-up’ demand) will shoot up and the capitalist economy will return to normal. But if you approach the slump from the angle of supply or production, and in particular, the profitability of resuming output and employment, which is the Marxist approach, then both the cause of the slump and the likelihood of a slow and weak recovery become clear.

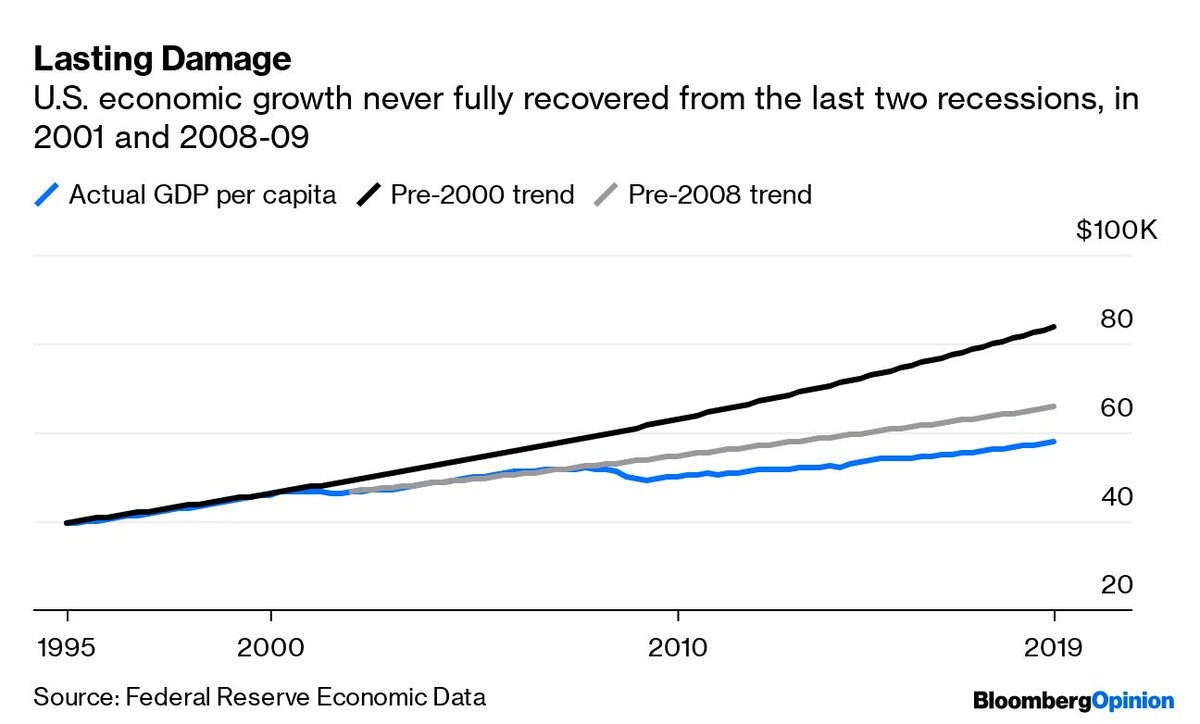

Let us remind ourselves of what happened after the end of the Great Recession of 2008-9. The stock market boomed year after year, but the ‘real’ economy of production, investment and workers’ incomes crawled along. Since 2009, US per capita GDP annual growth has averaged just 1.6%. So at the end of 2019, per capita GDP was 13% below trend growth prior to 2008. That gap was now equal to $10,200 per person—a permanent loss of income.

And now Goldman Sachs is forecasting a drop in per capita GDP that would wipe out even those gains of the last ten years!

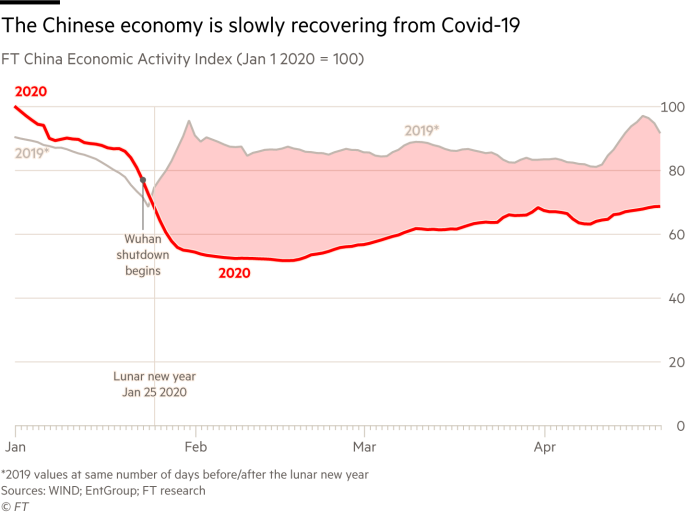

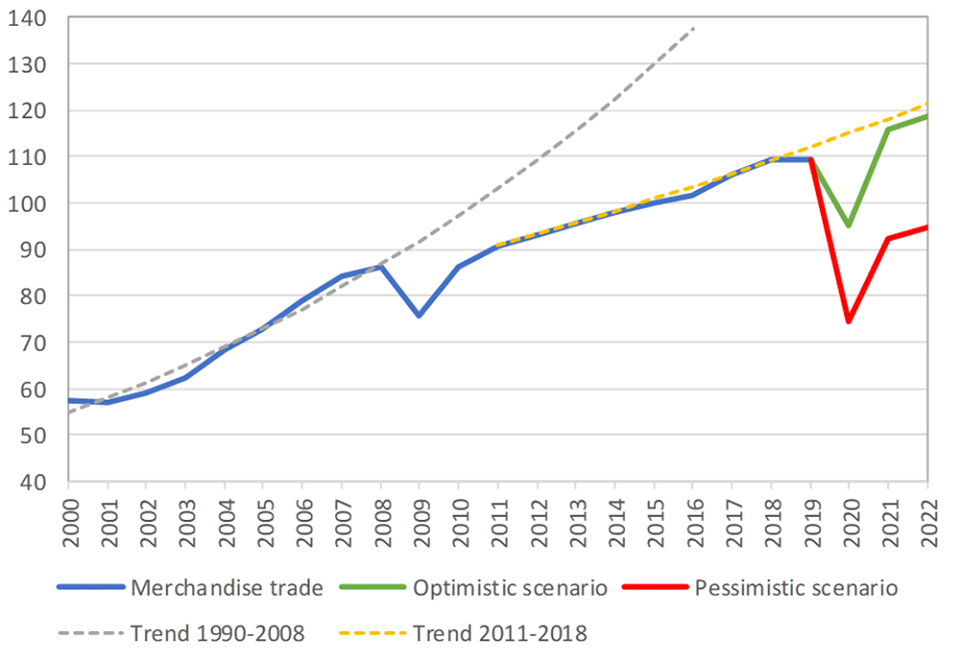

The world is now much more integrated than it was in 2008. The global value chain, as it is called, is now pervasive and large. Even if some countries are able to begin economic recovery, the disruption in world trade may seriously hamper the speed and strength of that pick-up. Take China, where the economic recovery from its lockdown is under way. Economic activity is still well below 2019 levels and the pace of recovery seems slow – mainly because Chinese manufacturers and exporters have nobody to sell to.

This is not a phenomenon of the virus or a health issue. Growth in world trade has been barely equal to growth in global GDP since 2009 (blue line), way below its rate prior to 2009 (dotted blue line). Now the World Trade Organisation sees no return to even that lower trajectory (yellow dotted line) for at least two years.

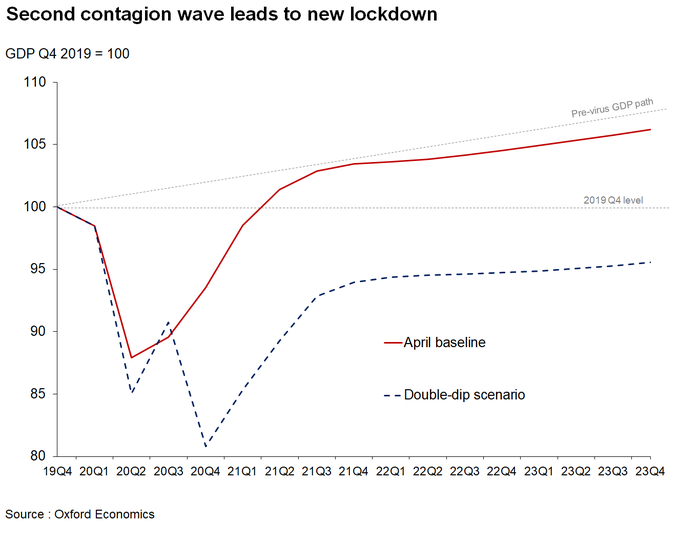

The massive public sector spending (over $3trn) by the US Congress and the huge Fed monetary stimulus ($4trn) won’t stop this deep slump or even get the US economy back to its previous (low) trend. Indeed, Oxford Economics reckons that there is every possibility of a second wave in the pandemic that could force new lockdown measures and keep the US economy in a slump and in stagnation through 2023!

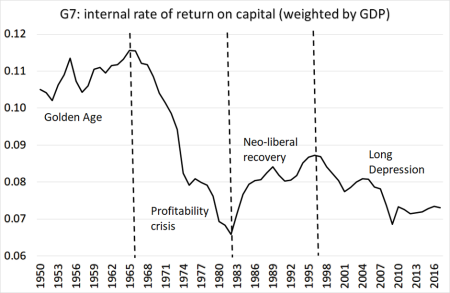

But why are capitalist economies (at least in the 21st century) not jumping back to previous trends? Well, I have argued on this blog in many posts that there were two key reasons. The first was that the profitability of capital in the major economies has not returned to levels reached in the late 1990s, let alone in the ‘golden age’ of economic growth and mild recessions of the 1950s and 1960s.

And the second reason is that in order to cope with this decline in profitability, companies increased their debt levels, fuelled by low interest rates, either to sustain production and/or to switch funds into financial assets and speculation.

But linked to these underlying factors is another: what has been called the scarring of the economy, or hysteresis. Hysteresis in the field of economics refers to an event in the economy that persists into the future, even after the factors that led to that event have been removed. Hysteresis is the argument that short-term effects can manifest themselves into long term problems which inhibit growth and make it difficult to ‘return to normal’.

Keynesians traditionally reckon that fiscal stimulus will turn slump economies around. However, even they have recognized that short-run economic conditions can have lasting impacts. Frozen credit markets and depressed consumer spending can stop the creation of otherwise vibrant small businesses. Larger companies may delay or reduce spending on R&D.

As Jack Rasmus put it well in a recent post on his blog: “It takes a long time for both business and consumers to restore their ‘confidence’ levels in the economy and change ultra-cautious investing and purchasing behavior to more optimistic spending-investing patterns. Unemployment levels hang high and over the economy for some time. Many small businesses never re-open and when they do with fewer employees and often at lower wages. Larger companies hoard their cash. Banks typically are very slow to lend with their own money. Other businesses are reluctant to invest and expand, and thus rehire, given the cautious consumer spending, business hoarding, and banks’ conservative lending behavior. The Fed, the central bank, can make a mass of free money and cheap loans available, but businesses and households may be reluctant to borrow, preferring to hoard their cash—and the loans as well.” In other words, an economic recession can lead to “scarring”—that is, long-lasting damage to the economy.

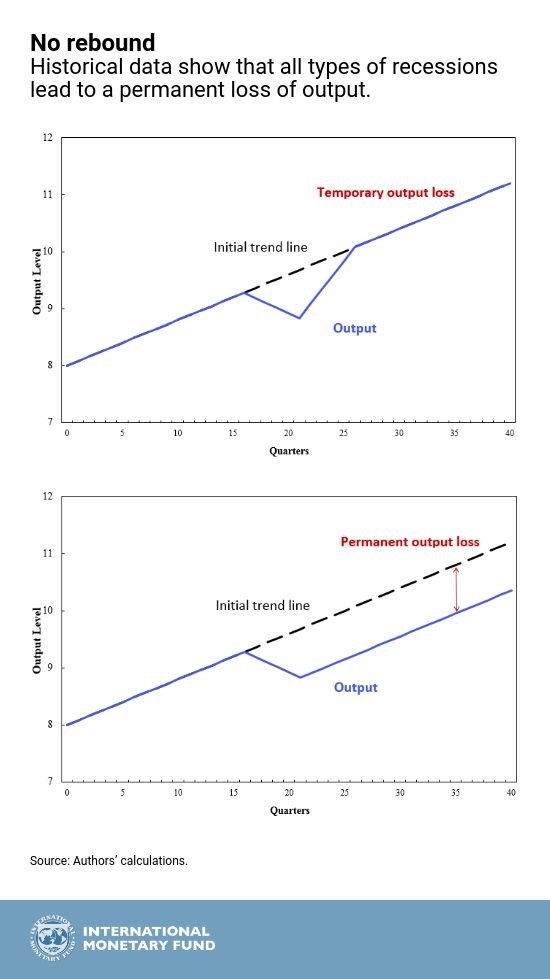

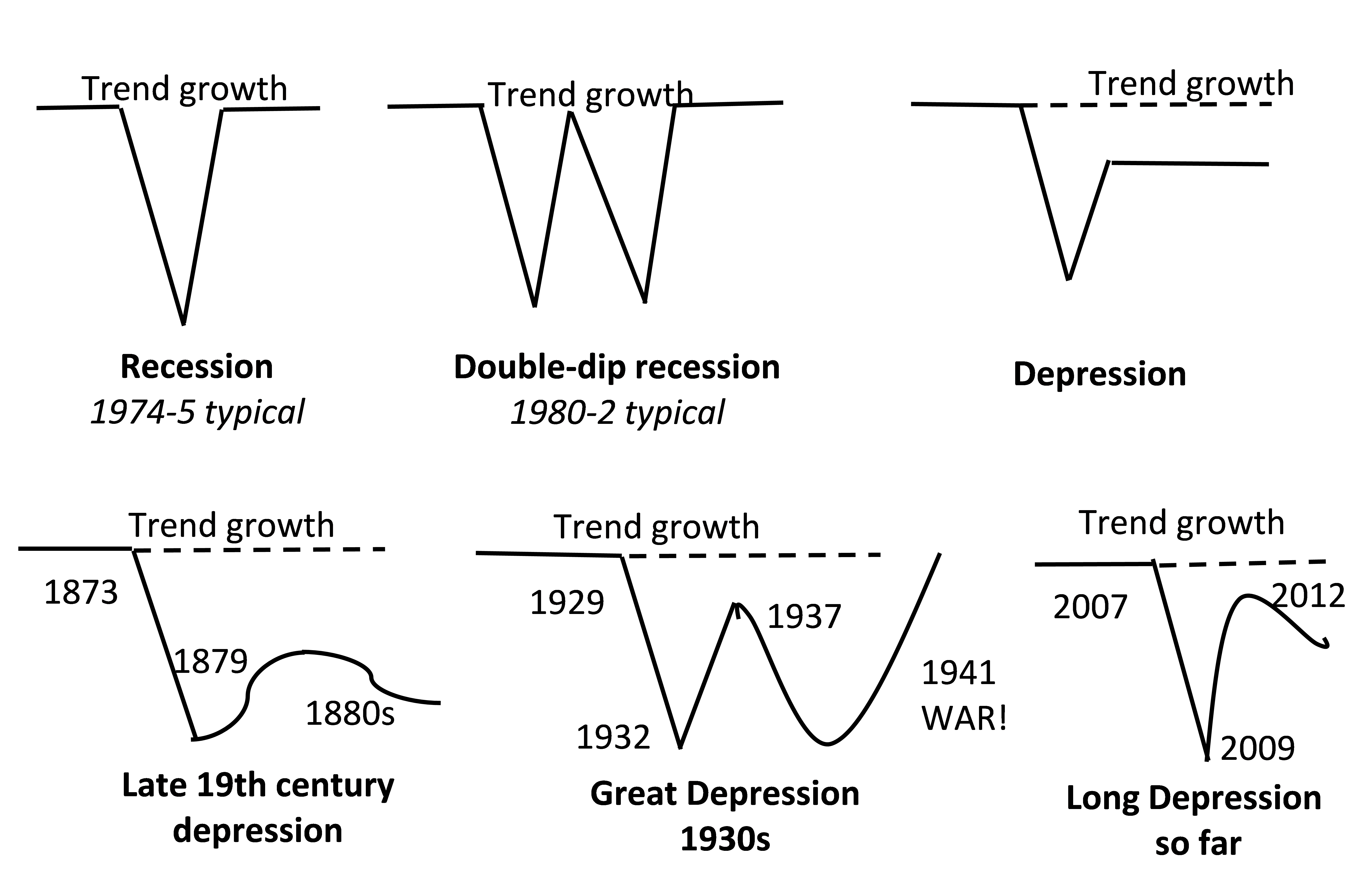

A couple of years ago, the IMF published a paper that looked at ‘scarring’. The IMF economists noted that after recessions there is not always a V-shaped recovery to previous trends. Indeed, it has been often the case that the previous growth trend is never re-established. Using updated data from 1974 to 2012, they found that irreparable damage to output is not limited to financial and political crises. All types of recessions, on average, lead to permanent output losses.

“In the traditional view of the business cycle, a recession consists of a temporary decline in output below its trend line, but a fast rebound of output back to its initial upward trend line during the recovery phase (see chart, top panel). In contrast, our evidence suggests that a recovery consists only of a return of growth to its long-term expansion rate—without a high-growth rebound back to the initial trend (see chart, bottom panel). In other words, recessions can cause permanent economic scarring.”

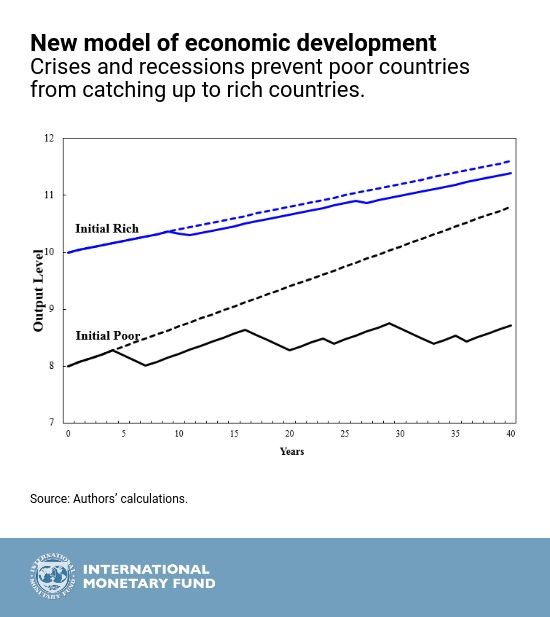

And that does not just apply to one economy, but also to the gap between rich and poor economies. The IMF: “Poor countries suffer deeper and more frequent recessions and crises, each time suffering permanent output losses and losing ground (solid lines in chart below).”

The IMF paper complements the view of the difference between ‘classic’ recessions and depressions that I outlined in my book of 2016, The Long Depression. There I show that in depressions, the recovery after a slump takes the form, not of a V-shape, but more of a square root, which sets an economy on new and lower trajectory.

I suspect that there will be plenty of scarring of the capitalist sector from this pandemic slump. Min Ouyang, an associate professor at Beijing’s Tsinghua University, found that in past recessions the ‘scarring’ of entrepreneurs from the collapse of cash flow outweighed the beneficial effects of forcing weak companies to shut down and ‘cleansing’ the way for those who survive. “The scarring effect of this recession is probably going to be more severe than of any past recessions….If we say that pandemics are the new normal, then people will be much more hesitant to take risks,” she says.

Households and companies would want more savings and less risk to protect against possible future shutdowns, while governments would need to stockpile emergency equipment and ensure they could rapidly manufacture more within their own borders. Even if the pandemic turns out to be a one-off, many people will be reluctant to socialize once the lockdown ends, extending the pain for companies and economies that rely on tourism, travel, eating out and mass events.

And this slump will accelerate trends in capitalist accumulation that were already underway: Lisa B. Kahn, a Yale economist has found that after slumps companies try to replace workers with machines and so force workers returning to employment to accept lower incomes or find other jobs, which pay less. Research After all, that is one of the purposes of the ‘cleansing’ process for capital: to get labour costs down and boost profitability. It scars labour for life.

“This experience is going to leave deep scars on the economy and on consumer/investor/business sentiment. This is going to scar a generation just as deeply as the Great Depression scarred our parents and grandparents.” John Mauldin

No comments:

Post a Comment