Rishi Sunak, the ex-hedge fund UK Chancellor, has presented the first budget of the Johnson government. The first thing is that the government is increasing spending by £30bn this fiscal year (of which £12bn is for handling the coronavirus outbreak) and plans to spend £175bn more than previously in this parliament.

The government’s policy decisions increase the budget deficit by 0.9 per cent of GDP on average over the next five years and add £125 billion (4.6 per cent of GDP) to public sector net debt by 2024-25. All this borrowing is intended to achieve 2.8% p.a. real growth in current public service spending, after a decade of cuts. In effect, the Sunak budget is reversing all the cuts that previous Conservative governments made under Cameron, Osborn & Co.

This may be the “largest sustained fiscal loosening” since the pre-election budget in 1992, according to the Office for Budget Responsibility (OBR). But all it does is stop the beating up of public services, local authorities and welfare that the government applied in the last ten years of misery. Ironically, after attacking those like the Labour Party, who demanded an end to austerity and increased government spending as being ‘profligate’, now the Johnson government announces the biggest fiscal spend nearly 30 years!

As Jeremy Corbyn said in parliament: “The government’s boast of the biggest investment since the 1950s is frankly a sleight of hand. It’s in fact only the biggest since they began their slash and burn assault on our services, economic infrastructure and living standards in 2010. Having ruthlessly forced down the living standards and life chances of millions of our people for a decade, the talk of levelling up is a cruel joke.”

Of course, there are very good reasons why the Johnson government must do this. First, Brexit has already cost the economy £26bn a year in slowing growth since the 2016 referendum, and the government will still be shelling out a net annual £11bn to the EU during this parliament. The OBR put it like this: “We estimate that the economic effects of the referendum vote have so far reduced potential output by around 2 per cent, relative to what would have happened in its absence. Part of this reflects lower net inward migration, but mostly it reflects weaker productivity growth on the back of depressed business investment and the diversion of resources from production towards preparing for potential Brexit outcomes. Real business investment has barely grown since the referendum, whereas our March 2016 forecast assumed it would have risen more than 20 per cent by now.”

And second, global growth was already slowing fast, reducing the trade prospects for a weak UK economy. And finally, there is the coronavirus ‘shock’ that has still to affect the economy over the next six months or so, at least.

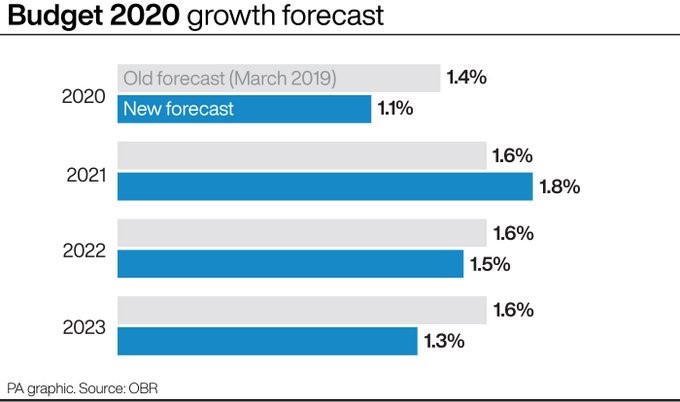

Sunak says he’ll invest an extra £175bn over next 5 years, which he says OBR calculates will add 0.5%pt to GDP growth. But all that does is compensate for the reduction in growth forecasts that the OBR has already made for the next few years. UK economic growth is optimistically forecast at a pathetic 1.1% this rising only to 1.8% next year. And this forecast takes into account the extra government spending – but not the impact of virus epidemic on production and investment. Moreover, the forecasts for real GDP growth in 2022 are just 1.5%; 2023 1.3% and 2024 just 1.4%. So that’s on average less than 1.5% a year during this parliament, and that assumes no global slump either.

This shows that the biggest fiscal spend in nearly 30 years is way too little and too late. With such poor growth figures, there is no way that with annual budget deficits rising to 2.8% of GDP in 2022, it will not lead to a rise in the public sector debt ratio. But even if a rise is avoided, the debt ratio will still be double where it was before the Great Recession in 2008. Ten years of cuts to lower the debt burden have totally failed.

Sunak says he is increasing investment in R&D to a record £22bn a year. As a percentage of GDP, he says, it will be the highest in nearly forty years – higher than the US, China, France and Japan. Public investment will be the highest it has been in real terms since 1955. But that is not saying much, as UK public sector investment has been falling for decades and is way below the OECD average.

If it works out, government investment as a share of GDP will rise from under 2% to 3%. Business investment is about 15% of GDP, so raising government investment from 2% to 3% will hardly make a difference if, in a slump, capitalists reduce their investment by say 25%, or 3% of GDP. Anyway, capitalists are just not investing enough to improve the productivity of labour. The OBR notes that “persistent weakness of productivity growth has prompted us to lower our steady-state assumption again. We now assume growth of 1.5% a year, down from 2%.”

And what about measures for working people? The living wage is to be raised to two thirds of median earnings by 2024. That means £10.50 an hour in four years time – still way below what really is a living wage. And there is no end to the iniquitous universal credit scheme for welfare benefits or any rise in the welfare spending cap.

There is to be a doubling of investment in flood defences over the next six years to £5.2bn protecting over 300,000 properties. But that does not even restore the 50% real cut in flood defences and the fire service over the last ten years, which has meant huge damage to thousands of homes from regular floods.

And talking of extreme weather and climate change, fuel duty is to be frozen. So given the recent sharp drop in oil prices, there is every incentive for increased fossil fuel spending. The decade-long freeze and fast-rising public transport fares have caused an extra 5 million tonnes of greenhouse gas emissions by encouraging people to abandon public transport in favour of their car. Luckily, the virus and the global recession is likely to do more in reducing carbon emissions than the budget!

Sunak talks of carbon capture and storage (CCS) as the sort of climate change technology where the UK should be excelling and says he will spend £800m to establish two or more CCS clusters by 2030. Apart from the fact this spend is tiny over 10 years, CCS is not a proven or effective way of reducing emissions, while the fossil fuel companies go untouched.

Austerity may be over, strictly defined, but the misery of the last ten years cannot be reversed. This budget will prove to be too little, too late, when the global slump comes.

No comments:

Post a Comment