Getting longer but lower

by Michael RobertsThe first three months of 2019 have shown a significant slowing in global economic activity. Global manufacturing output (as measured by JP Morgan economists) is actually falling.

So too is global trade for the first two months of this year.

And just today US retail sales for February also showed a slowdown.

We’ve had falling economic activity indicators in many major economies; and contracting industrial production in Europe and Japan. The business activity indicators in the US are the highest among the G7 top capitalist economies, but even there, they are beginning to fall back. Here is the latest Markit indicator for US manufacturing – still above 50 but dropping.

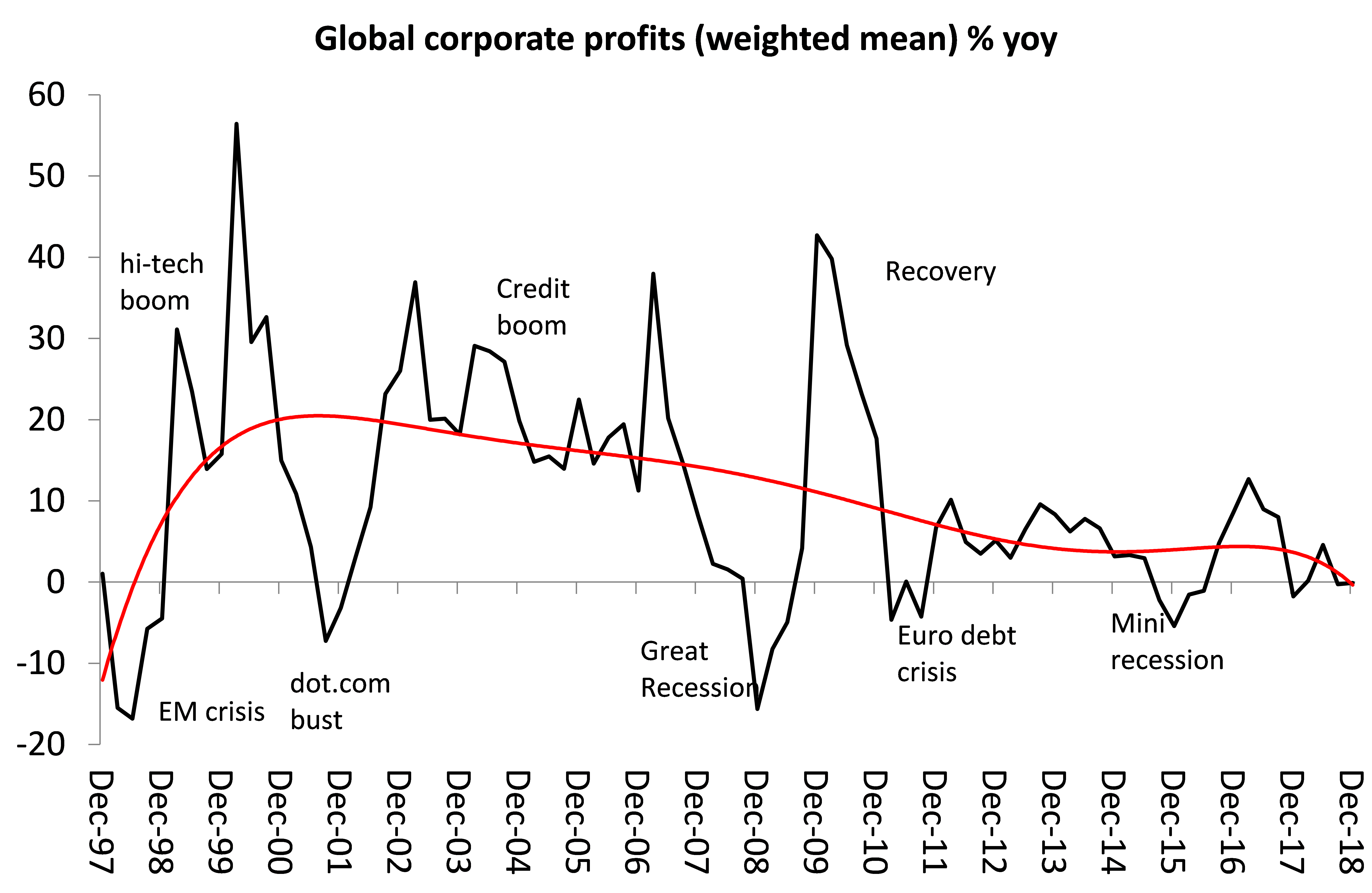

Corporate profits, which is the main driver of investment growth (usually with a one-year lag), are also slowing in some of the top economies. Indeed, China has just announced the biggest drop in industrial profits in ten years, down 14% in Jan-Feb over last year.

The forecasts for economic growth in the first quarter of this year which has just ended have all been lowered from previous estimates. In the US, after achieving near 3% a year in 2018, the average forecast is for just 2% annualised growth in Q1 2019 and even lower in Q2.

As I said in my last post, it appears that what I call the Long Depression in the major capitalist economies since the end of the Great Recession in 2009, is not over. I define this Long Depression as one where global growth in real GDP, trade, investment and wage incomes are well below the previous pre-crisis rate up to 2007 and the differential between where GDP and investment would be if trend growth had continued over the last ten years and where they actually are remains, with little narrowing at all.

And yet this is after what John Mauldin, the investment blogger calls: “years of astonishing, amazing, unprecedented, and astronomically huge monetary stimulus by the Federal Reserve, Bank of Japan, European Central Bank, and others. In various and sundry ways, they opened the spigots and left them running full speed for almost a decade. And all it produced was the above-mentioned weak recovery.”

And it is not just the top economies in Europe and Asia that are slowing fast. Australia, the so-called ‘lucky’country, has avoided a recession for over 27 years – only China has a better record. But with the slowdown in China and elsewhere, the Australian economy has entered what some call a ‘growth recession’, where real GDP growth no longer matches the expansion of the population, so GDP per person has been falling for the last two quarters of 2018. After a mega housing boom taking household debt to GDP to over 120%, one of the highest in the world, with household debt to disposable income near 190%, house prices have started to collapse, falling 14% from 18 months ago.

And then there are the so-called emerging markets. This is what I said last May:

“Rising global interest rates and the growing trade war initiated by US President Trump are going to hit the so-called emerging capitalist economies like Turkey. The cost of borrowing in foreign currency will rise sharply and foreign investment is likely to reverse…..Turkey is now near the top of the pile for a debt crisis, along with Argentina (already there), Ukraine and South Africa.”

Increased costs of borrowing in dollars and the fall in global trade, along with the risk of an outright trade war between the US and China have led to foreign investors holding back from putting their money into weaker or troubled emerging economies like Turkey, Argentina, Venezuela, and even Indonesia. Their currencies have plunged driving up costs of borrowing even further and leading a flight of capital by rich Turks or Argentines. William Jackson, the chief emerging markets economist at the consultancy Capital Economics, said: “The scale of the tightening of financial conditions is similar to that during the 2011-12 eurozone debt crisis.”

With the news that Turkeys’s Trump, Erdogan has lost local elections in the big cities like Ankara and Istanbul because the economy has gone into a slump, the Turkish lira has gone into meltdown. Turkey’s central bank has used up one-third of its dollar reserves in trying to prop up the Turkish lira and after that failed, the government is now blocking ‘short selling’ and banks lending money abroad. Erdogan has refused IMF funding because it would mean severe austerity and loss of control over government policy. But the lira is still slipping.

In contrast, Argentina’s right -wing government under Macri did opt for a huge IMF loan, indeed the biggest in IMF history – $57bn, as the IMf tried to prop up a government prepared to impose austerity and privatisation under the diktat of the IMF But this seems to be to no avail either as the economy tanks. The peso is sliding again amid a deepening decline in the domestic economy as Argentina approaches a general election in October.

Ukraine has also been a recipient of IMF aid, imposed on the country amid the deep recession of 2016 and during the civil war that broke out between the centre under a right-wing government in Kiev and the Russian-speaking east, backed by Putin’s Russia. Although the economy has made a mild recovery in 2017 and 2018, following the global pick-up in commodity prices, the level of corruption is unprecedented.

As a result, Ukraine electors have turned away from the main contenders, like President Poroshenko and the favourite of the West, Yulia Tymoshenko, and opted for a TV comedian who professes that he is clean and anti-corrupt. “Under Poroshenko, our standard of living lowered even more. I became a pensioner under his administration. I have a 30-year work experience as a kindergarten teacher and I receive 1,600 hryvnia [$58], they recently raised it by 100 hryvnia [$3.6],” said on Ukrainian voter tearfully. “I am very unsatisfied with the current government. They are all ‘thieves in law’.”

And then there is the tragedy of Venezuela. There is no space to go again into the terrible situation there, with daily power blackouts, hyperinflation (by the IMF’s calculations, Venezuela’s annual rate of inflation for 2019 will be 10m %) and shortages amid an attempt at a coup by right-wing interests backed by the US and its underlings in other Latin American countries. They have seized financial control of the state oil company (although not on the ground). The Maduro regime hangs on with the limited support of Russian and Chinese aid. Venezuela’s GDP meltdown since 2013 rivals the fall of the Soviet Union.

The advanced capitalist economies are slowing down fast and many so-called emerging economies are going into recession. Even in the US, fear about a possible recession has led investors to hold government bonds, driving down the yield (effective interest rate) below the level found for short-term borrowing by banks. The so-called inverted yield curve has been a fairly reliable indicator of a recession coming – because it reflects the unwillingness to invest for production even when interest rates for borrowing are very low.

How will any global recession emerge? The most likely pivot point is corporate debt. Since the end of the Great Recession, global non-financial debt has continued to rise. Household debt has fallen because people have defaulted on their mortgages or they are unable to get one. Government debt rocketed as governments bailed out the banks and borrowed to cover deficits caused by falling tax revenues and rising welfare benefits. But government debt has more or less stabilised (as share of GDP). However, corporate debt goes on rising.

So far the interest cost of servicing this rising debt has been manageable – at least for most companies, although it is estimated by the Bank for International Settlements (BIS) that around 20% of companies are ‘zombies’ ie are not earning enough profit to cover their debt costs. If interest rates were to short up (they cannot go any lower!), and/or profit were to dive, then whole swathes of companies could in trouble and start defaulting on their bonds or loans from the banks.

Maybe, the current downturn is just a mild one – as the fall in GDP growth in 2015-16 was. But it seems this time that it is wider in scope and may well be much deeper.

No comments:

Post a Comment