So now Socialist leader Pedro Sanchez will take over as prime minister of the world’s 13th largest and the Eurozone’s fourth-largest economy. Sanchez was an economist and ‘political adviser’ for the European parliament – so has never done a proper job in his life. Sanchez’s doctoral thesis was published as “La nueva diplomacia económica europea”, where Sanchez appears to consider the relationship between the state and the corporate sector and how politicians should engage in ‘economic diplomacy’, namely how the Spanish national state engages in relations with a supra-national entity like the EU. Now Sanchez will be testing his thesis in practice.

He takes over as PM in a minority socialist government depending on the votes of Podemos and the nationalists. And he faces a lot of economic challenges that the PP had failed to solve. As I argued at the time of the 2016 general election (which left Rajoy without a majority in parliament), before the Great Recession, economic growth in Spain had been largely due to investment in property, unproductive in capitalist terms.

Spain’s much-heralded economic boom saw 3.5% real growth a year during the 1990s but it stopped being based on productive investment for industry and exports in the 2000s and turned into a housing and real estate credit bubble, just like Ireland’s Celtic Tiger boom did. As the IMF summed it up: “The pre-crisis period was characterized by decreasing productivity of capital, measured as output per units of capital stock, both in absolute terms and relative to the euro area average. This is because capital flew to nontradable sectors, in particular construction and real estate, characterised by higher profitability but lower marginal returns. By contrast, investment in information and communication technologies or intellectual property remained below that of other euro area countries.”

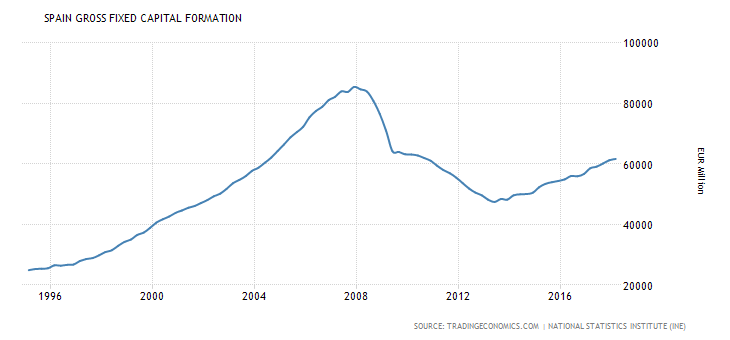

Since the end of Great Recession things have improved for Spanish capital only by keeping real wages down and employing cheap labour rather than making investments in new technology to raise productivity. Gross fixed capital formation in still well below pre-crisis levels. And this includes all investment, private and government; productive investment has recovered even less.

Indeed, the Spanish investment rate to GDP has fallen way more compared to pre-crisis rates than its EU rivals.

Why is this? As I said in my book, The Long Depression, the Achilles heel of Spanish capitalism is the long-term decline in its profitability. Every measure of Spanish capital’s profitability reveals the same long-term decline. Here is the AMECO measure as calculated by me, but in our (Carchedi, Roberts) upcoming book, World in Crisis, Juan Pablo Mateo has more comprehensive measures that confirm the AMECO version. And Maito, Esteban – The historical transience of capital. The downward tren in the rate of profit since XIX century also agrees.

The recovery in profitability since the end of the Great Recession has been modest. The rate of profit is still some 7% below where it was in 2007. And that is despite the huge cuts in government spending, reductions in employment and wages.

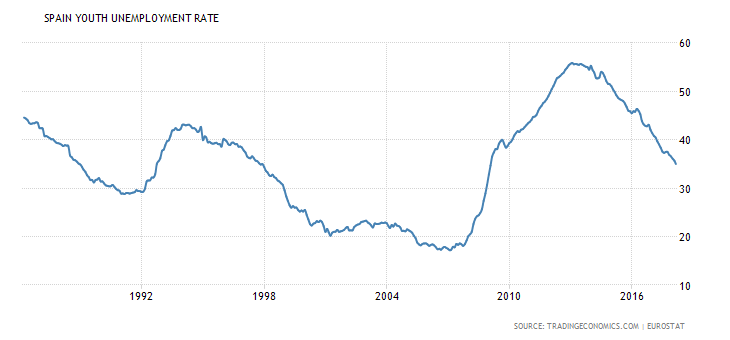

I quote from the IMF’s latest report on Spain: “Since 2009, unemployment has declined for all age groups, but remains higher than before the crisis disproportionately affecting low-skilled workers Those out of jobs more than a year account for roughly half of the unemployed. Involuntary part-time employment remains high, well above the EU average More than a quarter of workers are under temporary contracts

and the share of temporary employment among the youth is above its pre-crisis level.”

http://www.imf.org/en/Publications/CR/Issues/2017/10/06/Spain-2017-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-by-the-Executive-45319

Moreover, Spain recorded the lowest real wage growth of all EU countries in 2017 – namely zero! And this year, real wage growth will be negative, only Italian and British workers will suffer a larger fall.

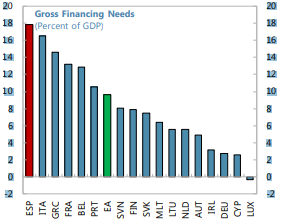

Although ‘austerity’ in the guise of cuts in government spending, higher taxes and running budget surpluses (before interest costs) stopped in 2015, the state is still heavily burdened with debts built up from bailing out Spain’s reckless and corrupt banking system. According to the IMF, annual gross financing needs are the highest in the euro area…even higher than debt-ridden Italy.

No wonder, the IMF reckons that “post-crisis, potential growth is projected to remain subdued with a lower investment rate.”

This long depression has also begun to break up the Spanish state, as last year’s unresolved Catalan separatist crisis exposed. Spain’s regional governments are deeply in debt and yet are being asked to make huge spending cuts. That’s why richer regional areas with their own nationalist interests, as in Catalonia and the Basque Country, have been making noises about separation from Madrid. The Sanchez government will now be depending on their votes.

I don’t need to change what I said back in my 2016 post. “The Spanish depression is a result of the collapse in capitalist investment. To reverse that requires a sharp rise in profitability. Until investment recovers, the depression will not end. And there is the probability of a new economic recession in Europe ahead, while the political leadership of Spanish capital is divided and uncertain what to do.”

No comments:

Post a Comment