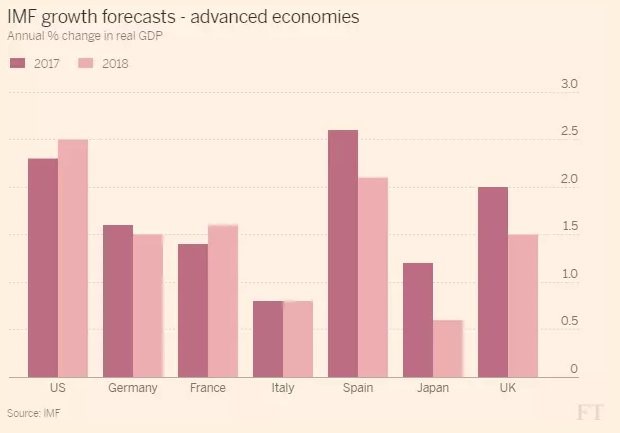

At its semi-annual meeting that started this week, IMF economists announced an upgrade in their forecast for global economic growth. This is the first upgrade that the IMF has made for six years. It was only a slight increase in its previous forecast of growth made in January. The IMF now expects world real GDP to rise 3.5% this year (compared to 3.4% before) and 3.6% next year (unchanged).

As the IMF chief, Christine Lagarde put it, “The good news is that, after six years of disappointing growth, the world economy is gaining momentum as a cyclical recovery holds out the promise of more jobs, higher incomes, and greater prosperity going forward.”

But the IMF also warns that: “the world economy may be gaining momentum, but we cannot be sure that we are out of the woods.”

Nevertheless, there is a growing confidence among mainstream economists and official international agencies that the world capitalist economy is finally coming out of its slow and weak recovery since the Great Recession of 2008-9. Below trend growth, weak investment and hardly any uptick in real incomes in most major economies since 2009 has been described variously as ‘secular stagnation’ or in my case as The Long Depression, similar to that of the 1930s and 1880s.

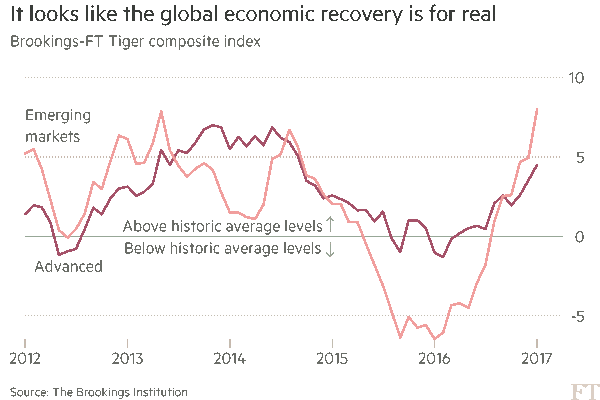

But maybe it is all over. Only this week, the FT’s economic forecaster model was showing a sharp pickup. The Brookings-FT Tiger index — tracking indices for the global economy — suggests growth has picked up sharply in both advanced economies and emerging markets in recent months.

The index, which covers all major advanced and developing economies, compares many separate indicators of real activity, financial markets and investor confidence with their historical averages for the global economy and for each country separately. The Tiger index suggests growth in emerging markets has picked up sharply since the oil price fall hit output in 2015. Having languished well below historic average levels this time last year, the index for emerging market growth has climbed to a level not seen since early 2013. China and India appear to have weathered recent rocky periods and indicators for growth are back above historic averages for both countries.

And the main economic indicators in the US and global economy have been picking up. The purchasing managers’ indexes (PMI) are surveys of companies in various countries on their likely spending, sales and investments. And the PMIs everywhere are well above 50, meaning that more than 50% of the respondents are seeing improvement. The global PMI now stands at its highest level (54) for three years and, according to JP Morgan economists, it suggests that global manufacturing output is now rising at a 4% pace compared to just 1% this time last year.

Things are also looking better in the so-called emerging economies. China has not crashed as many expected this time last year. On the contrary, the Chinese economy has picked up and, as a result, there has been increased demand for raw materials. The Chinese economy expanded 6.9% year-on-year in the first quarter of this year that ended in March, slightly up from 6.8% growth in the fourth quarter of last year. Investment and industrial production also had a slight uptick.

Gavyn Davies, former chief economist at Goldman Sachs and now a columnist for the Financial Times in London, pointed out that “Global activity growth has rebounded sharply, and recession risks have plummeted. Growth in real output is now running at higher levels than anything seen since the temporary rebound from the financial crash in 2009/10. Importantly, recent data suggest that the growth rate of fixed investment is beginning to recover, which is a body blow to one of the central tenets of the secular stagnation school.“

Behind this apparent recovery is a small recovery in corporate profits, which up to the middle of 2016 had been falling quarterly. Since then, corporate profits have recovered somewhat around the world and, according to JP Morgan, business investment has reversed its decline of the last year.

All this sounds promising, even convincing. But as the IMF warned, maybe these optimists are jumping the gun. The US economy remains the key driver of global growth, not Europe or China and there seems little sign of any uptick from the sluggish growth of 2% a year that the US economy has achieved over the last six years on average.

The stock market has been booming (until recently) on the expectation that President Trump would boost profits and investment through corporate profits tax reductions and a programme of infrastructure spending by the federal and state governments. But so far, nothing has happened. And anyway, in a previous post I showed that the impact of such measures on overall investment and growth would be minimal.

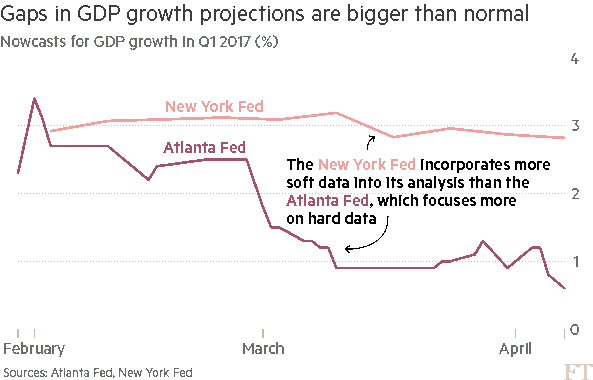

Indeed, what has happened is a growing divergence between economic data based on surveys of opinions about the US economy (‘soft data’) and actual figures (‘hard data’). According to Morgan Stanley economists, “the divergence is stunning.” In other words, everybody is very optimistic about the prospects for the US economy over the next 12 months but the current data don’t show it. This divergence is revealed by the huge differences in forecast US economic growth by the main economic forecasting agencies. The New York Federal Reserve reckons US real GDP will be up 2.6% in the first quarter that ended in March, while the widely respected Atlanta Fed forecast has dropped to just 0.5% for the same quarter. The difference is caused by New York including more ‘soft’ data and Atlanta excluding it.

Also investment analysts are now forecasting huge rises in corporate profits or earnings. First-quarter earnings are expected to rise 15% yoy for European companies, 9% for those in the US and 16% for Japanese firms – a complete turnaround from previous forecasts that predicted a slowdown in 2017 to follow the slowdown of 2016. Yet the very earliest profits results for the top US companies released this week were very disappointing.

Indeed, when we consider the hard data, the situation is not so rosy. The final reading of US national output for the fourth quarter of 2016 confirmed that the US economy grew only 1.6% in 2016, the weakest annual rate of growth for five years. The pace of growth did pick up in the second half of 2016 from a near stop in early 2016, but was still growing no more than 2% a year in the fourth quarter.

The bright spot was a significant pick-up in US corporate profits. Between the beginning of 2015 and the second half of 2016, corporate profits had fallen by 9%. However, in the second half of last year profits rose back 6% and in the last quarter were up 9.3% yoy and even more after tax.

Business investment had followed profits down three quarters later in 2015, confirming again my thesis that profits lead investment in the capitalist economic cycle. Business investment fell yoy in every quarter last year and equipment investment, the most important part of business spending, is down 5% from mid-2015. But with profits now rising, investment may pick up in 2017 – we’ll see.

But the latest measures of what will happen to investment and lending in the first quarter made by the St Louis Fed do not suggest any pick-up at all.

Consumer spending also does not seem to be responding to all this optimistic talk. US personal consumption spending seems to have slowed to just a 1.1% annual rate in the first quarter of 2017 compared to 3.5% in the last quarter of 2016, the weakest rate of expansion in four years and the worst first quarter since the end of the Great Recession in 2009.

And, as I have argued in several previous posts, corporate profitability in the major advanced capitalist economies remains weak and there is a sizeable section of ‘zombie’ firms, those unable to make any more profit than necessary to cover the servicing of their debts, let alone invest in new productive technology to raise productivity and expand.

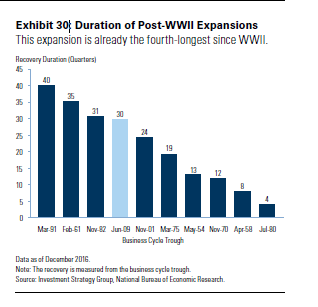

Confidence may be rising among mainstream economists and official agencies, based on improving surveys of opinion, but that must be balanced against the fact that the current recovery period since the end of the Great Recession is pretty long already.

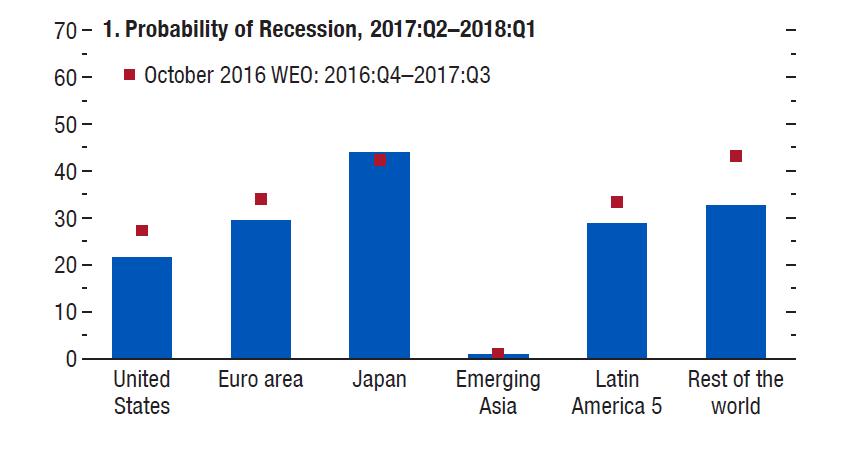

The IMF report signals the risk of a new recession. Its indicator suggests that it is still quite low for most economies at around 20-40% as the world economy moves through 2017. But Lagarde warns that “there are clear downside risks: political uncertainty, including in Europe; the sword of protectionism hanging over global trade; and tighter global financial conditions that could trigger disruptive capital outflows from emerging and developing economies.”

No comments:

Post a Comment