by Michael Roberts

Labour’s share

The leading Keynesian bloggers have been discussing the causes of inequality again. In particular, they have highlighted the apparent decline in labour’s share of national income in most advanced capitalist economies since the early 1980s.According to an ILO report, in 16 developed economies, labour took a 75% share of national income in the mid-1970s, but this dropped to 65% in the years just before the economic crisis. It rose in 2008 and 2009 – but only because national income itself shrank in those years – before resuming its downward course. Even in China, where wages have tripled over the past decade, workers’ share of the national income has gone down.

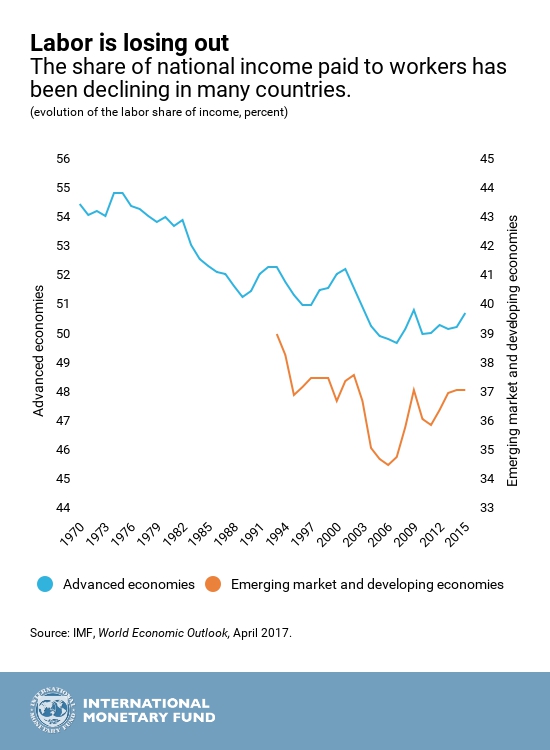

And the very latest IMF World Economic Report finds that “After being largely stable in many countries for decades, the share of national income paid to workers has been falling since the 1980s.”

The IMF goes on “Labor’s share of income declines when wages grow more slowly than productivity, or the amount of output per hour of work. The result is that a growing fraction of productivity gains has been going to capital. And since capital tends to be concentrated in the upper ends of the income distribution, falling labor income shares are likely to raise income inequality.”

As Keynesian blogger Noah Smith put in an article, “For decades, macroeconomic models assumed that labor and capital took home roughly constant portions of output — labor got just a bit less than two-thirds of the pie, capital slightly more than one-third. Nowadays it’s more like 60-40.” What has happened? Smith reckons that there are four possible explanations: 1) China, 2) robots, 3) monopolies and 4) landlords.

By China, he means that globalisation and the shift of manufacturing by multi-nationals to so-called emerging economies has led to labour in advanced economies losing jobs and seeing their wages stagnate while productivity has risen. Yet, as Smith points out, labour’s share has fallen in China too and (until recently) inequality of income rose sharply.

Then there is the accelerating substitution of machines for workers, particularly with robots and artificial intelligence. What appears to be happening is that more efficient, hi-tech firms are growing fast, leaving behind inefficient firms that use more labour. These less efficient firms lose market share and so start to employ less workers as well.

Well, that is pretty much a trend in capitalist accumulation from a Marxist perspective – so it should be no surprise. Indeed, the IMF report backs up this view. “In advanced economies, about half of the decline in labor shares can be traced to the impact of technology. The decline was driven by a combination of rapid progress in information and telecommunication technology, and a high share of occupations that could be easily be automated.”

It used to be argued in mainstream economics that inequalities were the result of different skills in the workforce and the share going to labour was dependent on the race between workers improving their skills and education and introduction of machines to replace past skills.

Indeed, another leading Keynesian Brad Delong still supports this answer. In a recent post, he suggests that Smith and Krugman have it wrong. “let me suggest that there is no mystery to explain.” If we look at labour’s share of net GDP, i.e. after deducting depreciation (the amount of output needed to replace worn-out plant and equipment), then labour’s ratio has not really fallen, except during the Great Recession.

So Delong concludes that any redistribution of income was indeed within labour’s share from low earners to high earners (CEOs, top executives, doctors and dentists etc) and not between labour and capital.

Delong’s argument is not convincing. First, depreciation may not be defined as profit but it is clearly a deduction from gross profits. Second, even the graph above does show a trend decline in labour share after its sharp rise in the late 1960s, which led to an intensification in the fall in profitability in most advanced capitalist economies from the mid-1960s and in an accompanying class struggle. The decline was also significant from 2000 during the credit-boom in the US (unlike Europe, where labour’s share was steady and even rose in the Great Recession – the opposite of the US experience).

And third, the gains in income for CEOs and small business doctors, dentists, lawyers and other ‘professionals’ are really profits not wages. See Simon Mohun’s excellent work in this regard.

Paul Krugman has returned to the theme of falling labour share in a recent post on his blog, where he argues that it is monopoly power among such capital-intensive companies like Google, Microsoft, etc and the energy companies that drives up profits the overall economy. This is an argument he has raised before. As he said back in 2012, “Are we really back to talking about capital versus labor? Isn’t that an old-fashioned, almost Marxist sort of discussion, out of date in our modern information economy?”

Krugman recognises that inequalities of income and wealth across US society and the declining share of income going to labour in the capitalist sector are not due to the level of education and skill in the US workforce, but to deeper factors. In 2012, he cited two possible explanations: “One is that technology has taken a turn that places labor at a disadvantage; the other is that we’re looking at the effects of a sharp increase in monopoly power. Think of these two stories as emphasizing robots on one side, robber barons on the other.”

The first argument is that modern technology is ‘capital-biased’, namely it aims to replace labour by machines over time. As Krugman put it: “The effect of technological progress on wages depends on the bias of the progress; if it’s capital-biased, workers won’t share fully in productivity gains, and if it’s strongly enough capital-biased, they can actually be made worse off.”

This is not new in Marxist economic theory. Marx put it differently to the mainstream. Investment under capitalism takes place for profit only, not to raise output or productivity as such. If profit cannot be sufficiently raised through more labour hours (ie.e more workers and longer hours) or by intensifying efforts (speed and efficiency – time and motion), then the productivity of labour can only be increased by better technology. So, in Marxist terms, the organic composition of capital (the amount of machinery and plant relative to the number of workers) will rise secularly. Workers can fight to keep as much of the new value that they have created as part of their ‘compensation’ but capitalism will only invest for growth if that share does not rise so much that it causes profitability to decline. So capitalist accumulation implies a falling share to labour over time or what Marx would call a rising rate of exploitation (or surplus value).

And yes, it does all depend on the class struggle between labour and capital over the appropriation of the value created by the productivity of labour. And clearly labour has been losing that battle, particularly in recent decades, under the pressure of anti-trade union laws, ending of employment protection and tenure, the reduction of benefits, a growing reserve army of unemployed and underemployed and through the globalisation of manufacturing.

Apart from capital-bias technology, Krugman considers that the fall in labour’s share may be caused by ‘monopoly power’, or the rule of ‘robber barons’. Krugman puts it this way. Maybe labour’s share of income is falling because “we don’t actually have perfect competition” under capitalism, “increasing business concentration could be an important factor in stagnating demand for labor, as corporations use their growing monopoly power to raise prices without passing the gains on to their employees.”

What Krugman seems to be suggesting is that it is an imperfection in the market economy that creates this inequality and if we root out this imperfection (monopoly) all will correct itself. So Krugman presents the issue in the terms of neoclassical economics.

But it is not monopoly rule as such, but the rule of capital. Sure, capital accumulates through increased centralisation and concentration of the means of production in the hands of a few. This ensures that the value created by labour is appropriated by capital and that the share going to the 99% is minimised. This is not monopoly as an imperfection of perfect competition, as Krugman explains it; it is the monopoly of ownership of the means of production by a few. This is the straight forward functioning of capitalism, warts and all.

The falling share going to labour in national income began at just the point when US corporate profitability was at an all-time low in the deep recession of the early 1980s. Capitalism had to restore profitability. It did so partly by raising the rate of surplus value through sacking workers, stopping wage increases and phasing out benefits and pensions. Indeed, it is significant that the collapse in labour’s share intensified after 1997 when US profitability again peaked and began to slide again. The IMF graph above shows that this applied to most economies.

Labour’s share in the capitalist sector in the US and other major capitalist economies is down because of increased technology and ‘capital bias’, from globalisation and cheap labour abroad; from the destruction of trade unions; from the creation of a larger reserve army of labour (unemployed and underemployed); and from ending of work benefits and secured tenure contracts etc. Indeed, this seems to be the conclusion reached by the IMF in its latest report, Chapter 3 of the April 2017 World Economic Outlook finds that this trend is driven by rapid progress in technology and global integration.

“Global integration—as captured by trends in final goods trade, participation in global value chains, and foreign direct investment—also played a role. Its contribution is estimated at about half that of technology. Because participation in global value chains typically implies offshoring of labor-intensive tasks, the effect of integration is to lower labor shares in tradable sectors. Admittedly, it is difficult to cleanly separate the impact of technology from global integration, or from policies and reforms. Yet the results for advanced economies are compelling. Taken together, technology and global integration explain close to 75 percent of the decline in labor shares in Germany and Italy, and close to 50 percent in the United States.”

Maybe ‘capital bias’ and ‘globalisation’ had less of an effect on labour share in the US because of the greater growth in financial profits and rents there than in the rest of the advanced economies.

Indeed, as Noah Smith puts it, “monopoly power, robots and globalization might all be part of one unified phenomenon — new technologies that disproportionately help big, capital-intensive multinational companies.” I call that modern capital, which, quoting Smith again, “provides a possible way to unify at least some of the competing explanations for this disturbing economic trend.”

No comments:

Post a Comment