by Michael Roberts

Now that the dust has settled (for a while) in Greece,

mainstream economics has been reconsidering what went wrong with Greece

and what the best solution would have been. And it now it seems that

both main wings of the mainstream: neoclassical, neoliberal Austerians

on one side; and Keynesian on the other side, agree. Grexit would have

been and still is the best solution.

Leading American Keynesian Brad de Long has joined Paul Krugman and Joseph Stiglitz to argue that Grexit is the cheaper option for the Greeks (http://www.bradford-delong.com/2015/07/highlighted-failing-to-manage-the-eurozone-economies-how-we-are-not-making-our-own-new-mistakes.html).

De Long is just amazed and shocked that the Euro leaders continue to demand austerity and commitment to Euro rules when it was clearly not working. It was irrational. “Because the North Atlantic had lived through the 1930s, I would say, this time we will not make the same mistakes policymakers made in the 1930s. This time we will make our own, different–and hopefully lesser–mistakes. I was wrong. The eurozone is making the mistakes of the 1930s once again. And it is on the point of making them in a more brutal, more exaggerated, and more persistent form than they were made back in the 1930s. But I did not see that coming. And so, when the Greek debt crisis emerged in 2010, it seemed to me that because the lessons of history were so obvious, the path to the Greek crisis’s resolution would be straightforward.”

What idiots the Euro leaders were and are. Surely they should have seen that they would need to “offer Greece enough aid, support, additional money, debt write downs, and debt reschedulings to make Greece better off by staying in the eurozone than it would have been if it had exited, depreciated, defaulted, and restructured back in 2010”?

This is what ex-finance minister Varoufakis and PM Tsipras leading the Greek government were hoping or expecting when they negotiated with the Troika. As Varoufakis explained his strategy: “a Marxist analysis of both European capitalism and of the Left’s current condition compels us to work towards a broad coalition, even with right-wingers, the purpose of which ought to be the resolution of the Eurozone crisis and the stabilisation of the European Union… Ironically, those of us who loathe the Eurozone have a moral obligation to save it!”

(http://yanisvaroufakis.eu/2013/12/10/confessions-of-an-erratic-marxist-in-the-midst-of-a-repugnant-european-crisis/#_edn2)

But, as De Long says, “that did not happen”. So now, says De Long, Grexit is the only way out. And he cites the apparent success of Iceland, a very small country that is not even in the EU, let alone the Eurozone, and thus was able to devalue and default to solve its debt crisis and is now racing towards prosperity. “Just look at the relative degree of recovery–essentially complete, and none–in Iceland and Greece, respectively.”

Really? Iceland is continually served up by the Keynesians as the model for resolving the debt crisis and the depression that Greece is suffering. But it is a Nordic myth, as I have explained in several posts. https://thenextrecession.wordpress.com/2013/03/27/profitability-the-euro-crisis-and-icelandic-myths/.

This story of default and devaluation is just not true. Iceland did not renege on the huge debts that its corrupt banks ran up with foreign institutions (mainly the UK and the Netherlands). It eventually renegotiated them and is now paying them back, like Greece. And devaluation did not mean that Icelanders escaped from a huge loss in living standards. They have done better than the Greeks on that score – but Icelanders started from a much higher standard of living than the Greeks. Even so, in euro terms, Icelandic employee real incomes fell 50% and are still 25% below pre-crisis levels.

Yes, Iceland did nationalise its banks but then privatised them again in record time. Two out of the three collapsed major banks in Iceland are now owned by their creditors, not the state. The third bank, Landsbanki, is still nationalised but that’s solely because of ongoing court cases involving Icesave. Most of the creditors actually sold their stakes onto foreign hedge funds. Some of the bankrupt banks only remained in government control for a few weeks. SPRON, for example, was merged into Arion Bank which in turn was given to its creditors a few weeks later, essentially a free gift to Kaupthing’s foreign creditors.

Iceland’s lauded recovery model involving devaluation of its currency was coupled with capital controls. And these remain a serious drag on investment for the capitalist sector. Iceland is growing at 2% a year, faster than much of Europe. But the IMF had originally forecast annual growth of around 4.5% from 2011-2013.

Many Icelanders say they do not ‘feel’ this modest growth. Outside booming fishing and tourism, businesses complain of stagnation. Some 80% of households are swamped in housing loan debts indexed to inflation. Investment is under 15% of GDP, a record low. Real incomes have dropped sharply for Icelandic households as their mortgage debt is index-linked to inflation.

And it is not true that through default and devaluation, Icelanders avoided the impact of austerity. Look at this chart of the degree of change in the budget balance before interest costs as a % of national GDPs made by governments globally between 2009 and 2014. Greece leads the way in the degree of austerity. But look which country is second: Iceland.

Brad de Long now reckons that the cost to the Greek economy of Grexit would be much lower than “the long-run costs of remaining in the eurozone given the required austerity now on offer from Brussels and Frankfurt.” That may be right, but the example of Iceland does not confirm it.

And neither does the traditional explanation of the Greek depression that comes from Keynesians: too much austerity. De Long says that “the key reason for the failure of forecasts is, of course, Brussels’s and Frankfurt’s–and Washington’s, both at the IMF and in the Obama administration–underestimate of the simple Keynesian multiplier at the zero lower bound on interest rates.”

Well, the ‘simple Keynesian multiplier’ measures the increase in real GDP growth that comes from a unit increase in government spending. But the evidence that this is decisive is not clear – see my post, https://thenextrecession.wordpress.com/2012/10/14/the-smugness-multiplier/ .

Moreover, I have shown in previous posts that the impact of austerity on growth in Greece and elsewhere is way less than the impact of the collapse in capitalist investment due to low profitability and high corporate and public sector debt. As Frances Coppola recently put it, “the story of the Greek crisis is not really one of fiscal profligacy resulting in a “sudden stop”. It is one of PRIVATE sector profligacy fuelled by rising external debt, itself resulting from (or caused by) falling competitiveness.”

https://thenextrecession.wordpress.com/2015/03/14/greece-keynes-or-marx/

The Marxist multiplier measures the amount of economic growth engendered by investment in the capitalist sector and thus by each unit of extra profitability (see my post,

https://thenextrecession.wordpress.com/2013/01/13/multiplying-multipliers/.

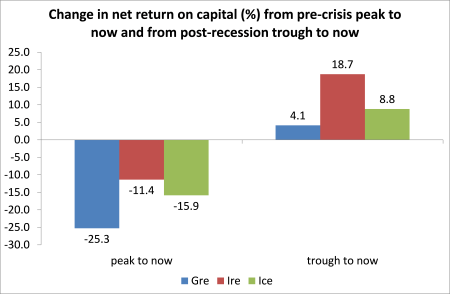

Greek capitalism took the biggest hit to profitability from the Great Recession and its profitability has recovered the least. In contrast, Ireland suffered the least of three economies below, and recovered profitability the most (although it is still down on its peak). And this is reflected in economic growth. This explains Greece’s worse position, not austerity as such or the failure to devalue.

Nevertheless, De Long continues to be amazed at the stupidity of the Euro leaders and the Austerians: “So why have we not learned from our history? I still rub my eyes in amazement: I would have thought that the Great Depression was a salient enough event in European history that we would not be making the same mistakes, exactly, again–and right now it looks like in what will turn out to be a more extreme way.”

Well, now it seems that the Austerians are not so stupid because they agree that the Greek government should opt for Grexit too. German finance minister, Wolfgang Schauble, during the tortuous negotiations on the ‘bailout package’ with Greece, apparently offered a deal to Varoufakis to stump up €50bn in ‘aid’ if the Greeks opted to exit the Eurozone.

And leading German Austerian economist and spokesman for the German Eurosceptic party, the AfD, Dr Werner Sinn agrees. “There are not many issues on which I agree with my colleagues Paul Krugman and Joseph E. Stiglitz and the former Greek finance minister Yanis Varoufakis. But one of them is the view that an exit from the eurozone would be advisable for Greece.”

Echoing the likes of Krugman and De Long, Sinn reckons that Greece needs to devalue and this cannot be done successfully by ‘internal devaluation’ ie cutting wages and prices as the current Troika measures are trying to do. “The public credit has delayed a Greek bankruptcy, but it has failed to revitalize the Greek economy. To compete, Greece needs a strong devaluation — a relative decline of its price level. Trying to lower prices and wages in absolute terms (for example, by slashing wages) would be very difficult, as it would bankrupt many debtors and tenants.”

For Sinn, the Keynesian solution won’t work, not because the Keynesians advocate devaluation of the Greek currency to make Greek capitalism competitive, but because they also want to increase public spending. “What about the solution favored by leftists: more money for Greece? No doubt, enormous government spending would bring about a Keynesian stimulus and generate some modest internal growth. However, apart from the fact that this money would have to come from other countries’ taxpayers, this would be counterproductive, as it would prevent the necessary devaluation of an overpriced economy and keep wages and prices above the competitive level.”

That’s why, for Sinn, Grexit would only work if it makes the Greek capitalist sector profitable and more competitive (at the expense of labour). Here Sinn spells out the perfectly rational logic of austerity that De Long and the Keynesians fail to understand. Austerity is not just some stupid ideological prejudice on the part of the likes of Schauble and Sinn (although it may be that too), it is a solution aiming to restore the profitability of Greek capital, just as it offered for other capitalist economies in this depression. See my post https://thenextrecession.wordpress.com/2015/04/24/austerity-has-it-worked/.

Sinn offers not the example of Iceland, as the Keynesians do, but the example of Ireland: “The Irish tightened their belts and underwent a drastic internal devaluation by cutting wages, which in turn led to lower prices for Irish goods both in absolute and relative terms. This made the Irish economy competitive again.” And they sure did ‘tighten their belts’. In my graph above of changes in government budgets since 2009, Ireland comes next after Greece and Iceland. Indeed, see Michael Taft’s excellent article on the Irish model for Greece: http://www.theguardian.com/world/economics-blog/2015/jul/10/ireland-no-model-greece-troika-austerity

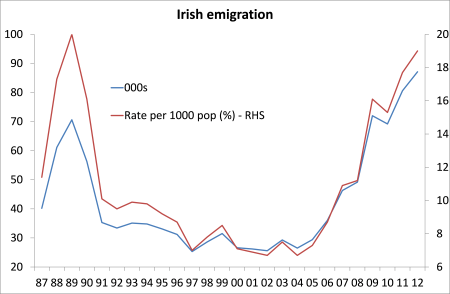

Sinn also neglects to mention that the main reason that Ireland has become competitive has been the mass emigration of the labour force and the special tax conditions provided by Irish governments for American multi-nationals to operate there. Irish emigration is now back at levels not seen since the dark days of late 1980s.

It is the same story with Estonia, another example of successful ‘austerity’ and now, of course, in Greece, Spain and Portugal. The Austerians rest their claims for recovery for these weak capitalist economies on huge reductions in wages and conditions for labour, massive cutbacks in public spending and mass emigration. All this is to restore the profitability of the capitalist sector.

But, it seems that Sinn and others now reckon that the policies of austerity alone will not be enough to get Greek capitalism back on its feet, however, tottering. Better now that Greece leaves, devalues its drachma and then carries through austerity measures. “Greece would have the option to return to the eurozone, at a new exchange rate, after carrying out institutional reforms — such as public recording of land purchases, functioning tax collection, accurate statistical reporting — and meeting the normal conditions for eurozone membership. It could take five or 10 years.”

For as Sinn puts it, “Until Europe is turned into a federal state — as it should become, at some point — it will not have a currency like the dollar. Until then, what is needed is a “breathing” currency union, with orderly entry and exit options, coupled with an insolvency rule for member states.”

So there we have it. The Keynesians say the way forward is through Grexit and so now do many Austerians. Both see Grexit as a solution to save Greek capitalism. The Keynesians reckon it will ‘free’ Greek capitalism from austerity. The Austerians reckon it will ‘free’ the Euro leaders from the wasted funding of a failing capitalist economy. But neither side is right if the profitability of capital does not recover in Greece and in Europe.

Leading American Keynesian Brad de Long has joined Paul Krugman and Joseph Stiglitz to argue that Grexit is the cheaper option for the Greeks (http://www.bradford-delong.com/2015/07/highlighted-failing-to-manage-the-eurozone-economies-how-we-are-not-making-our-own-new-mistakes.html).

De Long is just amazed and shocked that the Euro leaders continue to demand austerity and commitment to Euro rules when it was clearly not working. It was irrational. “Because the North Atlantic had lived through the 1930s, I would say, this time we will not make the same mistakes policymakers made in the 1930s. This time we will make our own, different–and hopefully lesser–mistakes. I was wrong. The eurozone is making the mistakes of the 1930s once again. And it is on the point of making them in a more brutal, more exaggerated, and more persistent form than they were made back in the 1930s. But I did not see that coming. And so, when the Greek debt crisis emerged in 2010, it seemed to me that because the lessons of history were so obvious, the path to the Greek crisis’s resolution would be straightforward.”

What idiots the Euro leaders were and are. Surely they should have seen that they would need to “offer Greece enough aid, support, additional money, debt write downs, and debt reschedulings to make Greece better off by staying in the eurozone than it would have been if it had exited, depreciated, defaulted, and restructured back in 2010”?

This is what ex-finance minister Varoufakis and PM Tsipras leading the Greek government were hoping or expecting when they negotiated with the Troika. As Varoufakis explained his strategy: “a Marxist analysis of both European capitalism and of the Left’s current condition compels us to work towards a broad coalition, even with right-wingers, the purpose of which ought to be the resolution of the Eurozone crisis and the stabilisation of the European Union… Ironically, those of us who loathe the Eurozone have a moral obligation to save it!”

(http://yanisvaroufakis.eu/2013/12/10/confessions-of-an-erratic-marxist-in-the-midst-of-a-repugnant-european-crisis/#_edn2)

But, as De Long says, “that did not happen”. So now, says De Long, Grexit is the only way out. And he cites the apparent success of Iceland, a very small country that is not even in the EU, let alone the Eurozone, and thus was able to devalue and default to solve its debt crisis and is now racing towards prosperity. “Just look at the relative degree of recovery–essentially complete, and none–in Iceland and Greece, respectively.”

Really? Iceland is continually served up by the Keynesians as the model for resolving the debt crisis and the depression that Greece is suffering. But it is a Nordic myth, as I have explained in several posts. https://thenextrecession.wordpress.com/2013/03/27/profitability-the-euro-crisis-and-icelandic-myths/.

This story of default and devaluation is just not true. Iceland did not renege on the huge debts that its corrupt banks ran up with foreign institutions (mainly the UK and the Netherlands). It eventually renegotiated them and is now paying them back, like Greece. And devaluation did not mean that Icelanders escaped from a huge loss in living standards. They have done better than the Greeks on that score – but Icelanders started from a much higher standard of living than the Greeks. Even so, in euro terms, Icelandic employee real incomes fell 50% and are still 25% below pre-crisis levels.

Yes, Iceland did nationalise its banks but then privatised them again in record time. Two out of the three collapsed major banks in Iceland are now owned by their creditors, not the state. The third bank, Landsbanki, is still nationalised but that’s solely because of ongoing court cases involving Icesave. Most of the creditors actually sold their stakes onto foreign hedge funds. Some of the bankrupt banks only remained in government control for a few weeks. SPRON, for example, was merged into Arion Bank which in turn was given to its creditors a few weeks later, essentially a free gift to Kaupthing’s foreign creditors.

Iceland’s lauded recovery model involving devaluation of its currency was coupled with capital controls. And these remain a serious drag on investment for the capitalist sector. Iceland is growing at 2% a year, faster than much of Europe. But the IMF had originally forecast annual growth of around 4.5% from 2011-2013.

Many Icelanders say they do not ‘feel’ this modest growth. Outside booming fishing and tourism, businesses complain of stagnation. Some 80% of households are swamped in housing loan debts indexed to inflation. Investment is under 15% of GDP, a record low. Real incomes have dropped sharply for Icelandic households as their mortgage debt is index-linked to inflation.

And it is not true that through default and devaluation, Icelanders avoided the impact of austerity. Look at this chart of the degree of change in the budget balance before interest costs as a % of national GDPs made by governments globally between 2009 and 2014. Greece leads the way in the degree of austerity. But look which country is second: Iceland.

Brad de Long now reckons that the cost to the Greek economy of Grexit would be much lower than “the long-run costs of remaining in the eurozone given the required austerity now on offer from Brussels and Frankfurt.” That may be right, but the example of Iceland does not confirm it.

And neither does the traditional explanation of the Greek depression that comes from Keynesians: too much austerity. De Long says that “the key reason for the failure of forecasts is, of course, Brussels’s and Frankfurt’s–and Washington’s, both at the IMF and in the Obama administration–underestimate of the simple Keynesian multiplier at the zero lower bound on interest rates.”

Well, the ‘simple Keynesian multiplier’ measures the increase in real GDP growth that comes from a unit increase in government spending. But the evidence that this is decisive is not clear – see my post, https://thenextrecession.wordpress.com/2012/10/14/the-smugness-multiplier/ .

Moreover, I have shown in previous posts that the impact of austerity on growth in Greece and elsewhere is way less than the impact of the collapse in capitalist investment due to low profitability and high corporate and public sector debt. As Frances Coppola recently put it, “the story of the Greek crisis is not really one of fiscal profligacy resulting in a “sudden stop”. It is one of PRIVATE sector profligacy fuelled by rising external debt, itself resulting from (or caused by) falling competitiveness.”

https://thenextrecession.wordpress.com/2015/03/14/greece-keynes-or-marx/

The Marxist multiplier measures the amount of economic growth engendered by investment in the capitalist sector and thus by each unit of extra profitability (see my post,

https://thenextrecession.wordpress.com/2013/01/13/multiplying-multipliers/.

Greek capitalism took the biggest hit to profitability from the Great Recession and its profitability has recovered the least. In contrast, Ireland suffered the least of three economies below, and recovered profitability the most (although it is still down on its peak). And this is reflected in economic growth. This explains Greece’s worse position, not austerity as such or the failure to devalue.

Nevertheless, De Long continues to be amazed at the stupidity of the Euro leaders and the Austerians: “So why have we not learned from our history? I still rub my eyes in amazement: I would have thought that the Great Depression was a salient enough event in European history that we would not be making the same mistakes, exactly, again–and right now it looks like in what will turn out to be a more extreme way.”

Well, now it seems that the Austerians are not so stupid because they agree that the Greek government should opt for Grexit too. German finance minister, Wolfgang Schauble, during the tortuous negotiations on the ‘bailout package’ with Greece, apparently offered a deal to Varoufakis to stump up €50bn in ‘aid’ if the Greeks opted to exit the Eurozone.

And leading German Austerian economist and spokesman for the German Eurosceptic party, the AfD, Dr Werner Sinn agrees. “There are not many issues on which I agree with my colleagues Paul Krugman and Joseph E. Stiglitz and the former Greek finance minister Yanis Varoufakis. But one of them is the view that an exit from the eurozone would be advisable for Greece.”

Echoing the likes of Krugman and De Long, Sinn reckons that Greece needs to devalue and this cannot be done successfully by ‘internal devaluation’ ie cutting wages and prices as the current Troika measures are trying to do. “The public credit has delayed a Greek bankruptcy, but it has failed to revitalize the Greek economy. To compete, Greece needs a strong devaluation — a relative decline of its price level. Trying to lower prices and wages in absolute terms (for example, by slashing wages) would be very difficult, as it would bankrupt many debtors and tenants.”

For Sinn, the Keynesian solution won’t work, not because the Keynesians advocate devaluation of the Greek currency to make Greek capitalism competitive, but because they also want to increase public spending. “What about the solution favored by leftists: more money for Greece? No doubt, enormous government spending would bring about a Keynesian stimulus and generate some modest internal growth. However, apart from the fact that this money would have to come from other countries’ taxpayers, this would be counterproductive, as it would prevent the necessary devaluation of an overpriced economy and keep wages and prices above the competitive level.”

That’s why, for Sinn, Grexit would only work if it makes the Greek capitalist sector profitable and more competitive (at the expense of labour). Here Sinn spells out the perfectly rational logic of austerity that De Long and the Keynesians fail to understand. Austerity is not just some stupid ideological prejudice on the part of the likes of Schauble and Sinn (although it may be that too), it is a solution aiming to restore the profitability of Greek capital, just as it offered for other capitalist economies in this depression. See my post https://thenextrecession.wordpress.com/2015/04/24/austerity-has-it-worked/.

Sinn offers not the example of Iceland, as the Keynesians do, but the example of Ireland: “The Irish tightened their belts and underwent a drastic internal devaluation by cutting wages, which in turn led to lower prices for Irish goods both in absolute and relative terms. This made the Irish economy competitive again.” And they sure did ‘tighten their belts’. In my graph above of changes in government budgets since 2009, Ireland comes next after Greece and Iceland. Indeed, see Michael Taft’s excellent article on the Irish model for Greece: http://www.theguardian.com/world/economics-blog/2015/jul/10/ireland-no-model-greece-troika-austerity

Sinn also neglects to mention that the main reason that Ireland has become competitive has been the mass emigration of the labour force and the special tax conditions provided by Irish governments for American multi-nationals to operate there. Irish emigration is now back at levels not seen since the dark days of late 1980s.

It is the same story with Estonia, another example of successful ‘austerity’ and now, of course, in Greece, Spain and Portugal. The Austerians rest their claims for recovery for these weak capitalist economies on huge reductions in wages and conditions for labour, massive cutbacks in public spending and mass emigration. All this is to restore the profitability of the capitalist sector.

But, it seems that Sinn and others now reckon that the policies of austerity alone will not be enough to get Greek capitalism back on its feet, however, tottering. Better now that Greece leaves, devalues its drachma and then carries through austerity measures. “Greece would have the option to return to the eurozone, at a new exchange rate, after carrying out institutional reforms — such as public recording of land purchases, functioning tax collection, accurate statistical reporting — and meeting the normal conditions for eurozone membership. It could take five or 10 years.”

For as Sinn puts it, “Until Europe is turned into a federal state — as it should become, at some point — it will not have a currency like the dollar. Until then, what is needed is a “breathing” currency union, with orderly entry and exit options, coupled with an insolvency rule for member states.”

So there we have it. The Keynesians say the way forward is through Grexit and so now do many Austerians. Both see Grexit as a solution to save Greek capitalism. The Keynesians reckon it will ‘free’ Greek capitalism from austerity. The Austerians reckon it will ‘free’ the Euro leaders from the wasted funding of a failing capitalist economy. But neither side is right if the profitability of capital does not recover in Greece and in Europe.

No comments:

Post a Comment