I’ve just returned from visiting Slovenia where I was invited to deliver a lecture on Socialising banking for the Institute of Labour Studies in Ljubljana and also to participate in a seminar with others, including economists from Die Linke, the German left party and Syriza from Greece on the role of banking and debt in the current capitalist crisis and Mick Brooks, the joint author with me of the UK’s Fire Brigade Union pamphlet on the banks (see s-time-to-take-over-the-BanksLR.pdf).

My paper for the lecture is here (Presentation on banking in Slovenia 140314) It has a simple message: that banking in a modern monetary economy should be a public service for the people, whether they work for an employer or run a small business. This aim can only be achieved through nothing less than full public ownership of the major banks, which must be democratically accountable and controlled by the people and which must act within a national (or even international) plan to meet the social needs of the people, not the profit of a few.

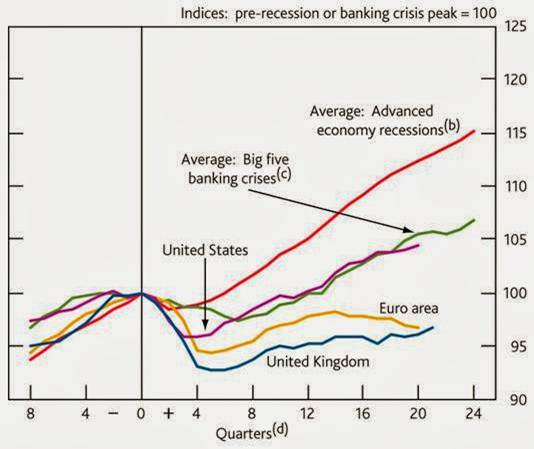

As I try to to show in this paper and in previous posts on this blog (see http://thenextrecession.wordpress.com/2010/09/15/banking-as-a-public-service/ and http://thenextrecession.wordpress.com/2012/11/19/marx-banking-firewalls-and-firefighters/), banking crashes can trigger crises in capitalism and generally they make the depth and loss of resources during those crises larger and any economic recovery weaker than average – as this graph from the Bank of England shows: in ‘average’ capitalist recession, recovery to the previous peak takes about one year. So there is only one year’s waste of resources. When a banking crash is also involved, it takes three years on average. But so humungous was this banking crash, global and extensive, that only the US economy is matching that average. Europe is still unable to return to the previous peak of economic activity after five years.

One feature of the global banking collapse in 2008 onwards was that governments bailed out these banks with huge dollops of taxpayers’ money and extra borrowing. According to the IMF, straight cash injections were equivalent to 7% of national GDP, or which less than half has been recovered from the banks since then.

And since the banking crash and the ensuing Great Recession, public debt has rocketed and now millions of households are being asked to pay for this disaster in programmes of ‘austerity’ (a word used in times of war hardship or depressions). But it’s ‘business as usual’ for the banks: they continue to engage in scams, risky investments and outright fraud, while top bankers pile up their grotesque bonuses yet again. Yet nobody apart from outright ‘Wolf of Wall Street’ fraudster, Bernie Madoff, has been charged and convicted on any crime.

My paper goes into examples of ‘business as usual’ but I bring to your attention another recent article by Ben Strubel, a former investment banker, who exposes in yet more detail the sheer scandal of the banking business in the hands of just a few huge global banks, but also copied by the smaller banks (see http://neweconomicperspectives.org/2014/03/financial-sector-greatest-parasite-human-history.html). And in a recent Rolling Stone article by Matt Taibi, he shows just how appalling the Libor interest-rate rigging was – pervasive and damaging to the tune of over £100bn (http://www.rollingstone.com/politics/news/the-vampire-squid-strikes-again-the-mega-banks-most-devious-scam-yet-20140212).

The financial sector has grown hugely as part of the modern capitalist system in the last 30 years – the theme of ‘financialisation’ in the ‘neo-liberal era’ since the 1980s.

But it makes no contribution to creating new value. It merely redistributes value already created, supposedly to enable investment to take place more efficiently. Even that role has been usurped by what is basically hedge-fund activity i.e. just betting on where the prices of financial assets like stocks, bonds, currencies, commodities and the derivatives of these will go – up or down? This activity is not only value-less (as I show in my paper) but also positively damaging to the productive sectors when these ‘financial instruments of mass destruction’ (to use the famous phrase of billionaire investor, Warren Buffett) blow up.

Indeed, Warren Buffett has commented just this week on hedge fund investing, pointing out that it does not even deliver decent returns for his fellow investors compared to just investing directly. At the 49th annual meeting of his holding company, Berkshire Hathaway, the ‘Sage of Omaha’ said the instructions laid out in his will advised his wife to invest 90 per cent of the money she inherits in a low-cost S&P 500 index tracker, and the other 10 per cent in short-term government bonds. In other words, avoid all investment funds run by highly paid investment banks and hedge funds. Study after study has shown that very few active fund managers outperform their benchmark over any meaningful period of time, and those that do are invariably difficult to predict in advance.

This was also the conclusion reached by Strubel in his article. His calculations show that investing directly and not through managers would have produced five times as much return.

So, not only is banking and financial investment worthless in creating value, it is mostly a huge selling scam designed to rip off rich investors. Of course, from the point of view of labour, we have no interest in or sympathy with the rich being ripped off. However, the failures and losses suffered by the banks and investors from this will also have repercussions for millions through job losses, wage cuts, higher interests and premiums, as we have seen.

In my paper, I argue that the proposed reforms of the banking system, more regulation, higher capital adequacy ratios, breaking up the banks into smaller bits, separating the risky investment arm from the ‘safe’ retail and commercial arms and a financial transactions tax – all these will not be enough to make banking a public service. We need public ownership of the main banks globally and in each country. If we stop short of that, as nearly every set of reform proposals does, like for example, the recent one proposed by the Keynesian-style think tank, Class, promoted the British trade unions

(2014_Banking_in_the_public_interest_-_Prem_Sikka), then it will fail to do the job.

But how to make state-owned banks democratic and accountable to the people and not just huge bureaucratic inefficient monoliths? At the ILS seminar in Slovenia, some excellent answers were provided by Philipp Hershel from Die Linke in his important banking paper Socialisation of German banking and also by Dimitris Liakos from Syriza in his LIAKOS SPEECH-1. In my paper, I argued that publicly owned banking must be democratically accountable and controlled by its own workers, consumers and the government. That means directly elected boards, salary caps for top managers, and also local participation. I constructed a provisional schema for this.

Most important, as the chart shows, banking must be integrated into a national plan for investment and growth to plan the economy for social need and not profit. Of course, that would not be possible without public ownership of the ‘commanding heights’ of the productive corporate sectors too. One goes with the other.

The people behind the Institute of Labour Studies have now formed a political party, the Initiative for Democratic Socialism, which has joined a coalition with two other radical and socialist parties to run in the upcoming Euro elections as the United Left. The United Left has adopted a programme that includes a publicly-owned and democratically controlled banking service. The UL will be part of the pan-European Left Bloc led by Syriza’s Alexis Tsipras in the Euro elections. See http://euobserver.com/news/123367.

No comments:

Post a Comment