The mass protests, demonstrations and actions that have shaken and still are shaking the pro-capitalist governments of Turkey, Brazil and Egypt show that the key emerging capitalist economies are not immune from the slump that has engulfed the advanced capitalist economies. The advanced economies still contribute some 55-60% of world GDP (depending on how you measure it). They remain the dominant influence over the world capitalist economy.

The Great Recession and the subsequent weak recovery have led to a significant fall in trade and investment flows to the emerging economies, particularly to the largest so-called BRICS (Brazil, Russia, China, India and South Africa). Their growth rates have also begun to fall away. In addition, the largest by far of the BRICS, China, is experiencing a 2-3% pt fall in its super-fast growth rate and that has been enough to cause sharp drop in the demand for commodities (agricultural and raw materials), the main exports of other emerging economies. So the crisis is a world-wide one.

Take Brazil. The nationwide street demonstrations of the past few weeks have sent shockwaves through Brazil’s political elite. There is widespread discontent with a ruling class that is seen as self-serving and corrupt. More than a million Brazilians have poured on to the streets in recent weeks to protest against a litany of grievances, from corruption and poor public services to outrage at billions of pounds in taxpayers’ money being spent to host the 2014 World Cup. It seems that the carnival for Brazilian capitalism of recent years is now over.

How has Brazil’s carnival of capital played out? We can look at the Brazilian economy from a Marxist viewpoint by analysing the movement in the rate of profit for the whole economy. Using the Extended Penn World Tables as my source data and my own calculations, I reckon the rate of profit in Brazil moved like this.

So between 1963 and 2008 (the latest year, I have), the rate of profit declined secularly by about 19%. But this secular fall was really the product of the very large decline in the rate of profit from 1963 to the early 1980s and 1990s. Over these 20 years or so, the rate of profit fell over 30% while the organic composition rose 23% and the rate of exploitation fell 17% – a classic example of Marx’s law of profitability at work.

But from the mid-1990s, Brazil’s’ ruling elite adopted neo-liberal policies designed to restore the rate of profit. Between 1993 and 2004, the rate of profit rose 35%. The organic composition of capital rose 20% as foreign investment flooded into new industries (autos, chemicals and petroleum), but the rate of exploitation rose even more, up 55%, as more Brazilians entered the industrial and agro processing labour force with intensive capitalist production methods, while wages were held down.

Over the last three decades Brazil became a major

agricultural producer and exporter to the world market. Leading exports

include soybeans and products, beef, poultry meat, sugar, ethanol,

coffee, orange juice, and tobacco. Brazil’s agrifood sector now accounts

for about 28% of the country’s GDP. Brazil’s is now the world’s

third-largest agricultural exporter (in value terms), after the US and

the EU. Rapid export growth was accompanied by changes in the

composition of agricultural exports away from tropical products to

processed products – up the value-added scale. Processed products now

account for about three-fifths of agricultural exports.

And Brazil, like some other emerging economies, benefited from some other favourable external factors that supported the neo-liberal policies at home. Food commodity prices rose. In a way, it was like the discovery of North Sea oil that helped Britain’s Thatcher government in the 1980s. The income windfall to Latin America from persistently high commodity prices over the past decade has been unprecedented. It averaged 15% of domestic income on an annual basis and close to 90% on a cumulative basis.

And Brazil, like some other emerging economies, benefited from some other favourable external factors that supported the neo-liberal policies at home. Food commodity prices rose. In a way, it was like the discovery of North Sea oil that helped Britain’s Thatcher government in the 1980s. The income windfall to Latin America from persistently high commodity prices over the past decade has been unprecedented. It averaged 15% of domestic income on an annual basis and close to 90% on a cumulative basis.

he

income windfall from persistently high commodity prices over the past

decade has been unprecedented. The windfall averaged 15 percent of

domestic income on an annual basis, and close to 90 percent on a

cumulative basis (see Chart 2). – See more at: http://www.economonitor.com/blog/2013/05/after-a-golden-decade-can-latin-america-keep-its-luster/#sthash.bfZQvDxX.dpuf

So a combination of rising commodity prices driven by Chinese demand,

productivity gains as the rate of exploitation rose and the expansion

of employment from the rural areas boosted profitability and growth for a

decade. After the 2002 crisis, GDP growth averaged above 4% per year

until 2010. This led to significant improvements in living standards

and life in general. But the iniquities of capitalist development remained embedded in the

system. Inequality of income and wealth in Brazil remains at extreme

levels, exceeded only by post-apartheid South Africa – and when measured

by a gini coefficient per capita, Mexico. Note Turkey is next.

Despite the boom of the last decade, average household net-adjusted disposable income in Brazil is still way lower than the OECD average of $23,047 a year – and that’s the average. Over 16 million people are still living in what is deemed extreme poverty, with monthly incomes of below 70 reais (about $33). Some 80% of men are in paid work, compared with 56% of women and 12% of employees work very long hours, higher than the OECD average of 9%, with 15% of men working very long hours compared with 9% for women. Around 7.9% of people reported falling victim to assault over the previous 12 months, nearly twice the OECD average of 4.0%. Brazil’s homicide rate is 21.0, almost ten times the OECD average of 2.2, one of the highest in the world at 21 per 100,000. Violence is concentrated among young people and over the past decade and a half, violence – including armed violence – has become a major social problem in the country. And Brazil’s regional disparities remain very high: average GDP per capita varies from just 46% of the national average in the Northeast region to 34% above the average in the Southeast.

Under the government of former president Lula and the commodity boom, there were some important gains for the working class: a social protection system, increasing credit at low interest rates for workers and universalising health and education. The Bolsa Familia, or family allowance programme, is the most visible face of these policies. Between 2004 and 2011, the number of families benefiting from income transfers more than doubled, from 6.5 million to 13.3 million, representing nearly one-quarter of the population. In the more isolated regions, payments under this programme have become the principal engine of the local economy. Another pillar of government policy, adopted through negotiations with the unions, was to raise the minimum wage and associated pension. It went up by 211% in nominal terms between 2002 and 2012, for a real inflation-discounted increase of 66%. Unemployment rate plunged from 12.3% to 6.7% and the labour force expanded at a 1.6% yearly rate.

However, during this boom, Marx’s law of profitability was still at work. From 2004 the rate of profit began to fall (down 8% to 2008 and more since), as wages shot up and the rate of exploitation dropped 25%. It was only the continued boom in food commodity prices that kept growth going.

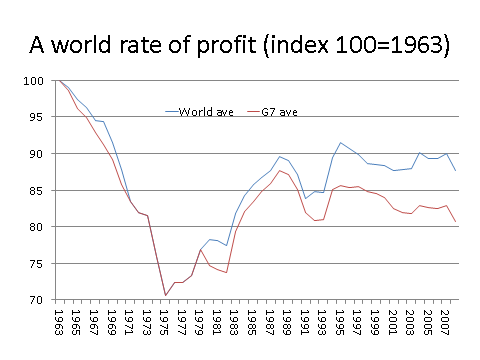

The fall in profitability since 2004 was mirrored in other major emerging capitalist economies (see my post on Turkey for a similar trend, http://thenextrecession.wordpress.com/2013/06/03/turkey-cant-see-the-trees-for-the-woods/). In my paper, A world rate of profit (roberts_michael-a_world_rate_of_profit), I show that the rising rate of profit in the emerging economies was able to push up the overall world rate of profit through the mid-2000s, but not since then.

When the global slump came in 2008-9, the emerging capitalist economies could not avoid the consequences. In the case of Brazil, it seemed that rising commodity prices plus a deliberate policy by the government to increase state-financed investment had enabled Brazil to avoid the worst of the slump compared to others.

But prices for Brazil’s key agricultural exports began to falter from 2011 onwards. In the last year, global commodity prices fell back sharply and profitability began to fall further. Now Brazil’s export profitability is some 20% below its best years before 2004.

Brazil’s GDP growth has consequently slowed since 2011. There has been a sharp fall in manufacturing investment and exports over the past two years. While public investment increased by 0.4% points to 5.4% of GDP, it has not been enough to compensate for the fall in the ratio of private investment to GDP from 14.3% to 12.7% last year. Industry has not even returned to its pre 2008 crisis production level.

The government has tried to get private sector investment going through tax cuts and incentives for the corporate sector but only at the cost of running up a deficit on its budget. Interest costs on the public debt have been mounting, forcing the government to cut subsidies to transport, housing and education on which the majority rely. It was the last straw to spend huge amounts on football and the Olympics (partly to boost capitalist sector profits) at the expense of basic public services. Thus the eruption of protest.

What now? Dilma Rousseff’s approval rating has sunk by 27 percentage points in the last three weeks. The share of people who consider Rousseff’s administration “great” or “good” plummeted to 30% from 57% in early June, according to a Datafolha opinion poll, the sharpest drop for a Brazilian leader since 1990, when Fernando Collor outraged the population by freezing all savings accounts in a desperate attempt to stop hyperinflation. 81% said they support the demonstrations. Asked if the protests had resulted in positive changes, 65% said yes.

The unrest has prompted a flurry of government promises to improve public services and other measures aimed at quelling the protests. In the past week alone, Brazil’s Congress voted on a battery of bills promoting issues popular with the protesters, and the supreme court ordered the arrest of a lower house representative convicted of corruption. Rousseff is now seeking congressional support for a non-binding referendum to ask Brazilians how they would like to see the political system changed.

But while the government appears to be making paper concessions, in reality it has no intention of reversing its neo-liberal policies. Finance minister Guido Mantega made that clear when he said that he will “raise taxes or cut public spending to compensate for any future subsidies it offers to support struggling sectors”. Profitability in the capitalist sector will not recover without further hits to living standards and economic growth will remain low as long as the world economic recovery remains weak and China slows down. The carnival is over.

No comments:

Post a Comment