The scandal of the Rogoff and Reinhart ‘affair’ (see my post, Revising the two RRs, http://thenextrecession.wordpress.com/2013/04/17/revising-the-two-rrs/) rumbles on among mainstream economists. The issue of their ‘mistakes’ and biases has moved onto whether any economic research is being done at all on a proper scientific basis. As Noah Smith (http://noahpinionblog.blogspot.co.uk/2013/04/the-reason-macroeconomics-doesnt-work.html) pointed out: “While this particular error is squarely in the lap of Rogoff and Reinhart, I think it is symptomatic of a broad failure to ensure that empirical results are replicable, which is the “gold standard by which the reliability of scientific claims are judged” (National Research Council, 2001). The lack of replicability of empirical models in economics should be an embarrassment to a field that has been trying (mistakenly, in my view) to catch up with the big boys in the natural sciences”. Apparently, even those journals that have policies requiring submission of data do not seem to have particularly compelling incentives for authors to actually cooperate. In this 2007 paper, Daniel Hamermesh pointed out that the editor of JMCB sought data sets and documentation from authors with accepted papers in that journal, but only got about one-third of them.

Smith does not think the two RRs did their research in order to prove austerity was right; no, it was down to useless data. “I don’t think it’s politics (mostly). I don’t think it’s the culture of consensus and hierarchy. I don’t think it’s too much math or too little math. I don’t think it’s the misplaced assumptions of representative agents, flexible prices, efficient financial markets, rational expectations, etc. Fundamentally, I think the problem is: uninformative data.”

Noah Smith concludes that “After the financial crisis, a bunch of people realized how little macroeconomists do know. I think people are now slowly realizing just how little macroeconomists can know. There is a difference.”

Well, it’s true that economic analysis often faces difficulty with its data. There are not many data points to use in judging whether the Kondratiev economic cycle of 50-60 years exists or not, for example – something I have been struggling with in my research. But it is not all as hopeless as Smith reckons. Can we tell if profits lead investment rather than vice versa? – a bit like the question of causality in the RR debts: does high debt lead to low growth or vice versa? Well, luckily for Marxist economic research, we can get somewhere with the question of profits and investment. My own research in my book, The Great Recession, provided some proof that profits led investment in the US in analysing its booms and slumps in the post-war period. But even better work has been done since by Jose Tapa Granados in his brilliant paper: Does investment cal the tune? (does_investment_call_the_tune_may_2012__forthcoming_rpe_), where he uses 252 quarterly data points for the Us economy to show a high correlation between profits and investment and, more important, statistical significance of the causal direction that profits lead investment. G Carchedi also has an upcoming piece of research based on US data with a similar number of data points.

However, Mark Thoma reckoned that what comes out of the R&R debacle is that “The biggest problem in macroeconomics is the inability of econometricians of all flavors (classical, Bayesian) to definitively choose one model over another, i.e. to sort between these imaginative constructions. We like to think or ourselves as scientists, but if data can’t settle our theoretical disputes – and it doesn’t appear that it can – then our claim for scientific validity has little or no merit. Unfortunately, the time period covered by a typical data set in macroeconomics is relatively short (so that very few useful policy experiments are contained in the available data, e.g. there are very few data points telling us how the economy reacts to fiscal policy in deep recessions). The point is that for a variety of reasons – the lack of experimental data, small data sets, and important structural change foremost among them – empirical macroeconomics is not able to definitively say which competing model of the economy best explains the data.

Well, yes, choosing the ‘right model’ or, if you like, the best set of assumptions (or priors) for a model is very important. If you start with the Keynesian model assumptions that consumption drives income and that drives investment, as most DSGE models do (see my post, http://thenextrecession.wordpress.com/2013/04/03/keynesian-economics-in-the-dsge-trap/), then, in my view, you are not going to get very far in explaining capitalist ‘business cycles’ with however much data you have. None of the DSGE models include profits or profitability as a variable, so they cannot really explain much. There is a great piece of Marxist research to do here in ‘modelling’ the ‘business cycle’ with profits as the main causal variable. Unfortunately, no Marxist economist is ensconced in a university with a team of students to develop and crunch the numbers.

So we are left where we are. That brings me to what mainstream economists are thinking right now about the state of the world economy. They are in total confusion. This week’s batch of global economic indicators was grim. Business indicators in the key ‘growth’ economies of the US, China and Germany all slowed sharply, while Europe’s indicators remain mired in recession mode.

The economic recovery in the advanced economies since 2009 has been very weak. The IMF published some graphs that show how weak this recovery has been in the advanced capitalist economies (constituting about 55-60% of world GDP) compared to previous recoveries from slumps. In the graphs, the red lines represent the current cycle in the advanced economies, the blue lines represent the average of three earlier recessions (1975, 1982 and 1991), and the index numbers are centred on the year before the recessions started. An abnormally deep recession in 2008/09 has been followed by an abnormally weak recovery, so real GDP per capita is now 10 per cent below the levels indicated by previous cycles (Panel A).

Is the cause of this weak recovery the implementation of the policies of fiscal austerity,as the Keynesians claim? Gavyn Davies in his FT blog (http://blogs.ft.com/gavyndavies/2013/04/21/great-recession-and-not-so-great-recovery/) considered the question by looking at these graphs. He concluded that “fiscal policy has been tightened everywhere to control public debt, which is much higher than “normal”, so real public spending is about 14 per cent below the cyclical norm (B). With fiscal policy tightening, the whole burden of supporting demand has fallen on monetary policy, so nominal interest rates have fallen to zero (C) and the central banks have resorted to sizeable increases in their balance sheets (D).”

So stock markets are booming (see my post, http://thenextrecession.wordpress.com/2013/03/30/its-still-a-bear-market/), rising on a wave of central bank power money being pumped into the banks. But companies that are cash-rich are hoarding their money and don’t invest. The result is that all this ‘wall of money’ goes into buying shares and bonds and even property. So financial and real estate markets are booming again and the old cycle of credit-fuelled unproductive speculation is rearing its very ugly head once again – to the increasing worry of the IMF and the national monetary authorities.

Would the global recovery have been stronger if fiscal policy had tightened less rapidly than has actually occurred?

Paul Krugman certainly thinks so (http://www.nytimes.com/2013/04/22/opinion/krugman-the-jobless-trap.html?_r=1&): “The main reason our economic recovery has been so weak is that, spooked by fear-mongering over debt, we’ve been doing exactly what basic macroeconomics says you shouldn’t do — cutting government spending in the face of a depressed economy. It’s hard to overstate how self-destructive this policy is. “ Radical Keynesian and MMT theorist (see my post, http://thenextrecession.wordpress.com/2012/04/27/effective-demand-liquidity-traps-and-debt-deflation/, Randall Wray is even more adamant: “As I argued in another piece (http://www.levyinstitute.org/pubs/ppb_111.pdf), in a depressed economy, you need fiscal expansion. “

But Gavyn Davies is not quite so sure that fiscal austerity is the cause of the weak recovery. “Since the short term fiscal multiplier is almost certainly not zero, the answer to this question is clearly “yes”, but it is hard to ascribe the whole of the shortfall in GDP growth to this single factor. If real government expenditure had performed as normal in this recovery, this would have resulted in spending being about 5 percentage points of GDP higher than it is now, so the fiscal multiplier would have needed to be about 2 in order to explain the whole of the 10 per cent growth shortfall. This seems implausibly high. Furthermore, monetary policy would have been tighter in such fiscal circumstances, and there would have been a somewhat greater (if still small) risk of fiscal crises in some economies. Therefore the Not-So-Great Recovery is not just a fiscal story.”

Indeed, despite the exposure of the two RRs, many stick to the view that the build-up of excessive public sector debt before the Great Recession that must now be deleveraged is still part of the problem. In his blog, James Hamilton (http://www.econbrowser.com/archives/2013/04/reinhartrogoff.html) said “The main reason that I personally am concerned arises from the fact that, for any level of the interest rate, a higher debt load means that the government will permanently need to spend more money just to pay the interest on the debt. In any case (despite the revised data of the two RRs) you would still conclude that higher debt loads are associated with slower growth in the postwar advanced economy data set, just as they were in the postwar emerging economy data set, just as they were in the centuries-long individual country data sets, and as also was found to be the case in separate analyses of yet other data sets by Cecchetti, Mohanty and Zampolli (2011), Checherita and Rother (2010), and the IMF (2012), among others.”

Right-wing mainstream economist John Taylor also opposed the idea that austerity (public sector spending cuts and tax rises) was the cause of failure to grow whatever the scandal of the two RRs. “The discovery of errors in the Reinhart-Rogoff paper on the growth-debt nexus is already impacting policy….offered as a reason why the U.S. should stop worrying about budget reform and consolidation and start worrying about austerity. But the claims about austerity in the current budget proposals are exaggerated. Consider the recent House budget proposal which balances the budget in 10 years without raising taxes by gradually reducing the growth of spending. It would reduce federal outlays as a share of GDP by 3.1 percentage points over the next decade (from 22.2% in 2013 to 19.1% in 2023). Critics label it austere, but this is less spending restraint than the 4.1 percentage point reduction in outlays as a share of during the 1990s (when spending fell from 22.3% in 1991 to 18.2 % in 2000). With this spending restraint, the 1990s were a very good decade for economic stability and growth, and they left the budget in balance. The same can be said for the next decade. The benefits of properly addressing the debt and deficit problems are enormous and the costs are surprising small.”

So austerity is not causing a problem because there isn’t any, but if you do it, it will help in the long term! Taylor’s argument is weakened when you realise that the reason that spending as a share of GDP fell in the 1990s was because real GDP growth was much stronger than post-2009. If the US economy had been growing at the 1990s average, then the fall in government spending as a share of GDP now would be much greater and quicker – and austerity would look very severe. So is it austerity that enables growth or growth that enables austerity? Here we go again.

Gavyn Davies goes on to blame the banking system and the failure to boost credit as the cause of weakness. I don’t see how this follows. There has been a huge expansion of credit. This has ended up in the banking system, to be used to buy financial assets and start a speculative boom. Money has not got through to the real economy not mainly because the banks are crippled in their ability to lend but mainly because there is no demand to borrow from overleveraged small businesses and cash-rich large businesses – you can’t make a horse drink (see my post, http://thenextrecession.wordpress.com/2013/03/04/you-cant-make-a-horse-drink-2/).

If central bank largesse is merely fuelling another financial bubble and not real GDP growth or even inflation, then another crisis could be on its way. That’s the worry of some mainstream economists. The last credit bubble from 2002-7 apparently was deliberately started or allowed to happen as the only way to get the modern capitalist economy going. According to Transcripts of the Fed’s internal meetings March 16, 2004, Donald Kohn, a longtime Fed staffer who later became the Fed’s vice chairman, said that the credit bubble was “deliberate and a desirable effect of the stance of policy.” According to Kohn, the Fed’s strategy was to: “boost asset prices in order to stimulate demand.”

Indeed, in a recent speech, Nayarana Kocherlakota, the president of the Minneapolis Federal Reserve Bank, reckons that the Fed “will only be able to achieve its congressionally mandated objectives by following policies that result in signs of financial market instability.” So the Fed is incapable of lowering the unemployment rate without creating more bubbles. Kocherlakota said that the Fed needed real interest rates to be “unusually low for a considerable period of time” and that this would lead to “unusual financial market outcomes” including “inflated asset prices, high asset return volatility and heightened merger activity.” John Taylor commented that surely there must be a better way.

Well yes, there is. What caused the Great Recession was a collapse in capitalist investment, not excessive public sector debt, and what is causing the slow recovery is the lack of renewed investment. Look at these graphics from John Ross’ blog (http://ablog.typepad.com/keytrendsinglobalisation/2013/04/investments-failure-to-recover.html).

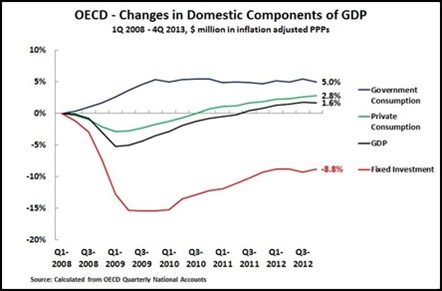

In constant price dollar PPPs, the form in which the OECD publishes the statistics, OECD GDP in the 4th quarter of 2012, the latest available data, was $625bn above its level in the 1st quarter of 2008. Government expenditure was $326bn above its 4th quarter 2008 level, net exports $482bn above, and personal consumption $659bn above. However fixed investment was $700bn below its 4th quarter 2008 level. It is therefore clearly the depression of fixed investment that remains the key weakness in the advanced economies.

The trend can also be seen clearly in the quarterly percentage change in the domestic components of GDP in each quarter between the 1st quarter of 2008 and the 4th quarter of 2012. Personal consumption continues to recover – being 2.8% above its 1st quarter 2008 level. Government consumption is 5.0% above its 1st quarter 2008 level – although this has essentially remained static since 2010, and is now mildly falling, reflecting various austerity policies. The key problem is that fixed investment remains –8.8% down.

This is not to deny that austerity has not played a role in the weak recovery. The great supporter of austerity, the UK government, has just announced that it scraped through in meeting its borrowing target for the fiscal year 2012-013. But it only did so by slashing public sector investment spending at a time when private sector investment is still at lows. As Jonathan Portes explained in his blog: “most of the deficit reduction has come from cutting public sector net investment (spending on schools, roads, hospitals, etc) roughly in half. Pretty much all the rest came from tax increases (note that the investment cuts and tax increases were both, to a significant extent, policies inherited from the previous government). And we can see when it happened – between 2009-10 and 2011-12. But these sources of deficit reduction stopped in 2011-12, because the government belatedly realised that cutting investment was a major mistake and that the economic imperative was actually to do precisely the opposite (not that there was much investment left to cut); and it stopped putting up taxes overall. So we can see also what’s happened since – with the impact of the weak economy on tax receipts reducing revenues, the deficit has been flat and is projected to stay flat.” Austerity was not working and has now been abandoned.

But why did investment collapse in the first place? That would help us look at how it might be revived. I have argued many times on this blog that there are two reasons. The first is that profitability in the main capitalist economies dropped after 2006 , heralding the Great Recession of 2008-9. And the rate of profit in most economies has not recovered to pre-crisis levels (in the US it has – just). So there is no ability or desire to raise investment.

The second reason was the huge build-up of private sector debt before the crisis (see my post http://thenextrecession.wordpress.com/2013/02/25/deleveraging-and-profitability-again/). So we are not talking about the Reinhart and Rogoff story of public sector debt, but at the private sector. This overhang of ‘fictitious capital’ still restricts the ability or willingness of households to spend as they pay down debt or default on their mortgages and for companies (not just banks) to invest when their returns only just cover the servicing of their debts (zombie operations). Only low interest rates have kept many firms in business, even in the US (graph).

Pumping money into the financial sector is not working to restore sufficient investment growth to get unemployment down and households to spend. Although fiscal austerity has played a role in delaying the recovery of investment, the real cause lies in the capitalist sector itself (see my post,http://thenextrecession.wordpress.com/2013/02/10/why-is-there-a-long-depression/). In that sense, the scandal of the two RRs does not provide sufficient ammunition for Keynesians to suggest that more government spending will cure the economy, get growth up and public debt down. If the lack of investment is the problem, what is needed is for a plan of public investment for jobs, the environment and in technology that does not depend on raising the profitability of the corporate sector, indeed, aims on replacing it.

No comments:

Post a Comment