by Michael Roberts

The latest Trade and Development report

by the United Nations Conference on Trade and Development (UNCTAD), the

economic research agency to help ‘developing countries’, is a must

read. Not only is it packed with data and statistics about trends and

developments in global production, trade and investment, but this 2020

issue takes a very radical position on how to get the world economy out

of what the IMF calls the ‘lockdown’ slump. As UNCTAD eloquently says: “The

world economy is experiencing a deep recession amid a still-unchecked

pandemic. Now is the time to hammer out a plan for global recovery, one

that can credibly return even the most vulnerable countries to a

stronger position than they were before. The status quo ante,

is a goal not worth the name. And the task is urgent, for right now,

history is repeating itself, this time with a disturbing mix of both

tragedy and farce.”

First, UNCTAD’s economists spell out the depth and extent of the pandemic recession. UNCTAD reckons the global economy’s real GDP will contract by about 4.3 per cent this year, leaving global output by year’s end over $6 trillion short (in current US dollars) of what economists had expected it to be before the Covid-19 pathogen began to spread. “In short, the world is grappling with the equivalent of a complete wipe out of the Brazilian, Indian and Mexican economies. And as domestic activity contracts, so goes the international economy; trade will shrink by around one fifth this year, foreign direct investment flows by up to 40 per cent and remittances will drop by over $100 billion.”

The Great Lockdown has tipped the global economy into recession in 2020 on a scale not witnessed since the 1930s. As a result, over 500 million jobs worldwide are under threat and at least 100 million jobs will have gone entirely by year-end. Furthermore, between 90 million and 120 million people will be pushed into extreme poverty in the developing world, with hunger and malnutrition certain to follow, while income gaps will widen everywhere. These developments point toward a massive uptick in sickness and death.

The urgent need for increased health spending along with declining tax revenues, combined with a collapse in export earnings and pending debt payments has exposed a $2-3 trillion financing gap in the developing world which the ‘international community’ has, so far, failed to address. “There is a very serious danger that the shortfall will drag developing countries into another lost decade ending any hope of realizing the ambition of the 2030 Agenda for Sustainable Development.”

UNCTAD economists note something I argued last March, that the world economy was already heading for a slump before the pandemic hit. In the advanced capitalist economies, the average growth rate between 2010–2019 fluctuated around an annual average of 2 per cent, compared with 2.4 per cent from 2001–2007. Growth also declined for developing countries from 7.9 per cent in 2010 to 3.5 per cent in 2019, with an annual average of just 5.0 per cent compared with 6.9 per cent from 2001–2007 (or 3.4 and 4.9 respectively, excluding China). The global economy had entered dangerous waters by late 2019. Growth was slowing across all regions with a number of economies contracting in the final quarter.

Moreover, UNCTAD reckons that a V-shaped recovery from the 2020 slump is not likely. Even a full V-shaped recovery with annual growth next year above 5 per cent and the world economy returning to its 2019 level by end of 2021 would still leave a $12 trillion income shortfall in its wake and an engorged debt burden, particularly in the public sector. But even that is not going to happen, says UNCTAD: “Our own assessment also sees the bounce continuing into next year albeit with stronger headwinds weakening the pace of global recovery which will, under the best scenario, struggle to climb above 4 per cent.”

What economic policies should be adopted to end this ‘lockdown slump’ and avoid or reduce the hit to the livelihoods of billions? That depends on the analysis of the causes of the slump itself.

And here I take issue with UNCTAD’s economists. They reckon the cause of the global slowdown before the pandemic and the lost decade since the Great Recession ended in 2009 is primarily due a ‘lack of global demand’. This lack of demand is caused by wages being too low because of neoliberal policies; and by capitalist investment being too low because of a switch into financial speculation rather than into productive investment; and by fiscal austerity reducing government spending.

UNCTAD economists openly follow the Keynesian ‘explanation’ for the lost decade (or what I have called the Long Depression) since 2009. And their solution is a re-adoption of Keynesian policies to manage capitalism better. For UNCTAD, slumps start with a collapse in demand ie in investment spending and above all in household consumption. That leads to a fall in sales, trade and then production and investment. “Since its founding in the aftermath of the Great Depression, the key principle of macroeconomics has been that effective demand – expected sales of final goods and services – determines income and employment.” That may be the key principle of macroeconomics, but as I have argued before in many posts, this sequence is not correct and is actually back to front. In a capitalist, profit-making, economy, it is profits and profitability that drive investment and when profitability drops, investment in the means of production and in labour will contract, leading to unemployment and loss of consumer incomes and demand.

Indeed, on occasion even Keynes recognised that profitability (which he called the ‘marginal efficiency of capital’) was an important factor in causing slumps. As he said: “Unemployment, I must repeat, exists because employers have been deprived of profit. The loss of profit may be due to all sorts of causes. But, short of going over to Communism, there is no possible means of curing unemployment except by restoring to employers a proper margin of profit.” If the marginal efficiency of capital fell below the interest cost of borrowing capital, then capitalists would have a loss of ‘animal spirits’ and stop investing and instead hoard money. But this aspect of Keynesian theory is ignored by modern Keynesians (as it was by Keynes himself). There is no mention of profit or profitability in the whole of the long UNCTAD report. Instead we are asked to accept that slumps are caused by low wages and consumption and by low investment caused by a switch to financial speculation leading to ‘instability’.

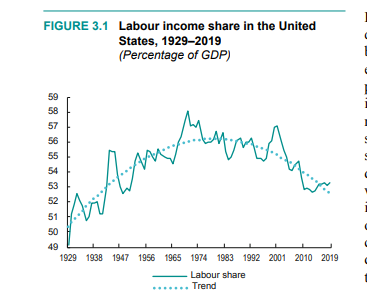

You see, in the last 40 years, the share of profits in the national incomes of the major economies has risen at the expense of wages and so the crisis of capitalist production is ‘wage-led’ not ‘profit-led’. “In the last decade, the profit share has increased in all but three G20 countries. If these pre-Covid-19 forces of wage repression remain in place, the labour share will likely continue its decline in many economies in the next years exacerbating inequalities. In the United States, after a 50-year descent, the labor share is now back to its 1950s level; if current trends continue, in ten years’ time it will be back to the brink-of-the-abyss level of 1930.”

UNCTAD says the problem is that “The world largely abandoned the imperative of demand management with the turn to neoliberal policies in the 1980s and an exclusive focus on measures to boost growth from the supply-side.” But UNCTAD offers no real explanation of why the government policies changed in the 1970s towards what are now called neo-liberal measures like wage suppression. If everything was going swimmingly in the ‘golden age’ of the 1960s for capitalism and with workers’ wages, why change? UNCTAD’s offered explanation is that “a more active role of the government in economic reconstruction fell out of fashion in recent decades under the influence of the neoliberal economic mindset.” So Keynesian policies of managing capitalism “fell out of fashion” because of a change of ideology to a “neoliberal mindset”. This is the explanation also recently made by Thomas Piketty is his new tome, Capital and Ideology, where he argues that it was a change of ideology that changed economic policies.

This idealist explanation ignores the main objective economic condition for capitalism in the 1970s: the well-documented profitability crisis. In the 1970s, rates of profit on capital in the all the major economies plummeted, leading to a severe slump in 1980-2. This forced governments to abandon Keynesian ‘demand management’. It had failed to save capitalism and governments turned to ‘neoliberal’ policies based on crushing trade union power, decimating manufacturing industry in the advanced capitalist economies and taking capital and productive capacity into the cheap labour areas of the global south (and eastern Europe after the fall of the Soviet Union).

Yes, the ‘rules of the game’ were changed from ‘demand management’ to ‘free markets, corporate tax cuts and globalisation’. But this was based on the objective situation, not on some ideological nastiness. UNCTAD may think that returning to Keynesian demand management will solve rising inequality, global warming and low wages and investment. But if the profitability of capital stays low, such policies (even in the unlikely event of being implemented) won’t work.

UNCTAD’s economists note that productivity growth has slowed significantly in the last 20 or more years. In the US, productivity grew 17 percent in the 1999–2009 decade but only 12.5 percent in the last decade; China’s impressive productivity growth of 162 percent in the earlier decade came down to 99 percent in the last decade. But they seem to think this is due to lower slowing aggregate demand. But the evidence is clear: those countries with low levels of productive investment growth had low levels of productivity growth, and low levels of investment growth were driven by low levels of profitability, not ‘demand’.

It’s true that productive investment growth has slowed while investment in financial assets has risen, driven by cheap credit (leading to rising debt). But again the question is why capitalists invested productively with credit back in the 1960s and early 1970s but now prefer to purchase financial assets? Why have “policies drifted towards a different paradigm of finance-led globalization”? Should we not consider the motor force for this is the low profitability in productive investment?

UNCTAD says “as long as growth needs to rely on credit and the State is removed from actions to control finance and ensure full employment, financial instability and crises become features of capitalist economies”. The implication here is that if the state controlled finance it could achieve full employment and end crises. But surely, as UNCTAD goes onto to say “with profit preservation being the linchpin of the model, wage earners or the public sector bear the cost of crises, and downward pressure on wages suppresses aggregate demand in the subsequent cycle.”

Indeed, ‘profit preservation’ is the problem because it is the driving force for capitalist production. So when UNCTAD says it wants to focus “on functional income distribution” ie the wage-profit share distribution, and reduce the profit share, it ignores the reality that it is the capitalist mode of production for profit that generates that unequal distribution. UNCTAD wants us to end “rent-seeking behaviour and market concentration (ie monopolies), and unequal terms of trade (imperialism) and the international division of labour (imperialism)”, but how can that be done without taking control and ownership of the multinational companies and financial institutions that breed these inequalities and imperialist flows of value?

UNCTAD says that “markets, left alone, cannot efficiently provide society with the necessary collective goods and with the conditions for sustainable, equitable growth and development, regardless of the starting point. A mixture of active fiscal policies and more structural policies are then needed to fill the gap, policies that look beyond temporary stabilization and contribute to economic reconstruction.” This implies that things would work efficiently if markets were interfered with and ‘managed’.

UNCTAD’s ‘structural policies’ boil down to more regulation of monopolies and banks, not taking them over. “To curtail market monopolization and corporate rent-seeking, much of the regulatory structure dismantled over the past four decades needs to be restored. In addition, antitrust and anti-monopoly laws have to be updated.” And “we need a re-regulation of finance. This includes tackling the giant private banks through international oversight and regulation; addressing the highly concentrated and critical market for credit rating; and the cosy relationship between rating agencies and shadow banking institutions.” Anybody who has read my analysis of the effectiveness of regulation over monopolies and banks will conclude that this policy of regulation will not work.

Take climate change. UNCTAD presents a whole range of ’green’ measures to curb and control global warming. But there is no call for the public ownership of the fossil fuel industries and their phasing out.

Maybe that’s too much to expect from an international agency like UNCTAD, funded as it is by the great powers in the UN. UNCTAD wants to promote a radical alternative to neoliberalism that it reckons has brought capitalism to its knees in the pandemic, but if it only advocates a return to Keynesian-style demand management of capitalism, it is not offering a “plan for global recovery, one that can credibly return even the most vulnerable countries to a stronger position than they were before”.

No comments:

Post a Comment