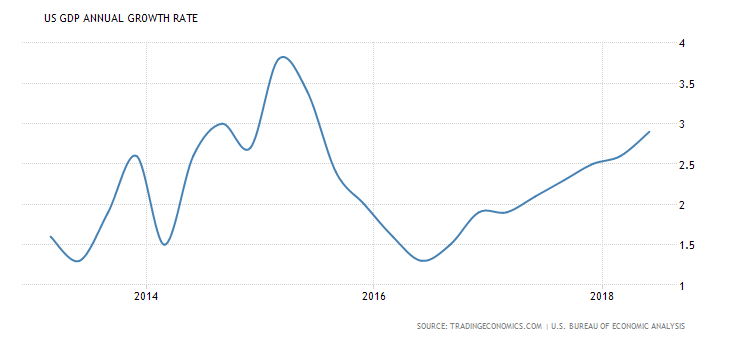

US real GDP growth for the second quarter of 2018 was confirmed at an annual rate of 4.2%. And that means US real GDP is 2.9% higher than one year ago. The ‘annualised’ rate was the highest since the third quarter of 2014. Similarly the year on year rate is the highest since 2014. But not the highest rate in history – as President Trump claims!

But it does show a relative recovery from the near recession rates of 2016.

But as I have mentioned before in previous posts, the underlying story is not so sanguine. First, the 4% ‘annualised’ growth rate is really dependent on some one-off factors that will soon turn into their opposites. US net exports was a big factor in the 4% rate and this was mainly due to the rush by China to buy up American soybeans before tariffs on US exports took effect in retaliation to Trump’s trade war with China.

Second, growth has been jacked up by Trump’s huge tax cuts for corporations on their profits. While pre-tax profits for the major corporations have risen a little, it is post-tax profits where there has been a bonanza. According to a recent report by Zion Research, for the top 500 US companies, 49% of their 2018 profits were due to the Trump tax cuts. For some sectors, like the telephone companies, it was 152% of 2018 profits ie from loss to profit.

Nevertheless, mainstream economics seems generally convinced that the US is out of its Long Depression of the last ten years and is now motoring ‘normally’. The official unemployment rate is at all-time lows, wages are beginning to rise a little and inflation has ticked up marginally.

So the US Federal Reserve decided to push up its policy interest rate for the eighth time since 2015 to reach 2.25%. The rate is used to set credit card, mortgage and loan rates and will trigger rises across the board for consumers and businesses. In a statement the Fed signalled more rate hikes were imminent. “The committee expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2% objective over the medium term. Risks to the economic outlook appear roughly balanced,” So the Fed seeks to ‘normalise’ rates in line with the ‘normal’ growth of the US economy and reckons its economic forecasts are about right.

But as I pointed out in a previous post, if the Fed is wrong and the productive sectors of the US economy do not resume ‘normal growth’ (the average real GDP growth rate since 1945 has been 3.3% – so growth is not back there yet), the rising costs of servicing corporate and consumer debt could lead to a new downturn.

The key factor for growth is investment by the capitalist sector. And what decides the level of that investment in the last analysis is not the level or cost of debt but the profitability of any investment. Business investment has made a modest recovery in the last few quarters, driven by the 16% rise in corporate profits after tax. But the bulk of this profits bonanza for US corporates in 2018 has been used to pay higher dividends to shareholders and buying back company shares to boost the share price, not in productive investment. And within productive investment, most has gone into the oil industry and into ‘intellectual property’ (software etc). Investment in equipment and new structures in other businesses has been very modest.

Moreover, non-financial corporate profits are still below levels of 2014, even after Trump’s boost.

And in the productive sectors of the economy, like manufacturing, they are falling quite sharply – as measured per employee.

At the other end of the economy, average incomes for American families are making little progress. In an excellent post, Jack Rasmus of the American Green Party showed that for non-supervisory workers (non-managers) who are the bulk of the American workforce (133m out of 162m), real incomes are falling not rising, while the burden of consumer debt is rising. When Trump announced his corporate tax cuts, he claimed that this would allow companies to increase wages from their increased profits. This, of course, has turned out to be nonsense. There has been very little increase in private sector wage compensation since the end of 2017.

And it is only in the US that we can talk about ‘recovery’ or ‘normal’ growth. Everywhere else hopes of a return to pre-crisis growth rates seem dashed. In the Eurozone, growth has slipped back to around 2% a year, still one-third below pre-crisis rates.

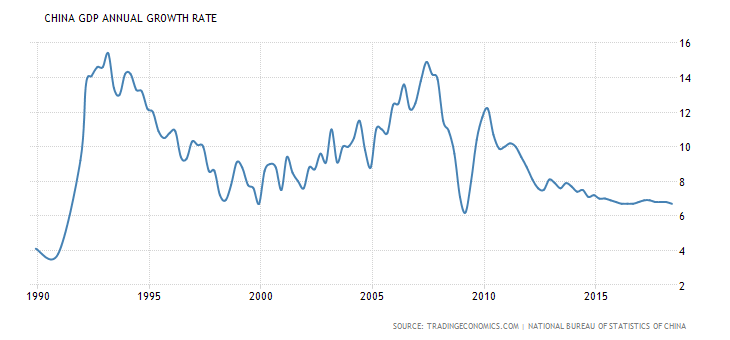

In Japan, it’s back at 1%. China too is ‘struggling’ to stay above 6% a year.

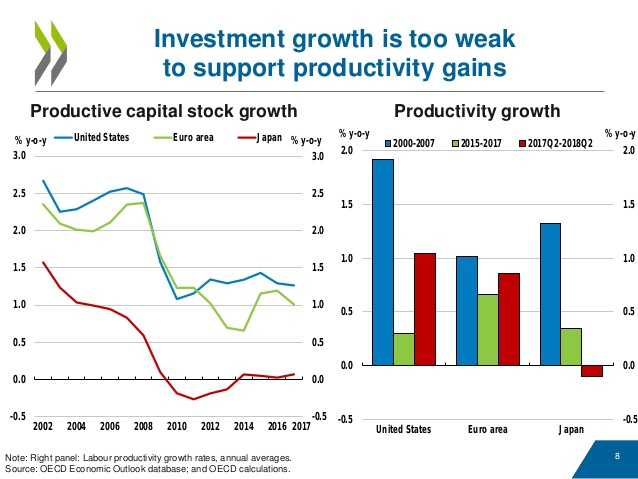

As the OECD put it in its latest interim report on the global economy: “Global growth is peaking; the trade war is beginning to bite; investment growth is still too weak to boost productivity; real wages are still below pre-crisis levels; and the losses in income from the Great Recession will never be recovered.”

“Trade tensions are starting to bite, and are already having adverse effects on confidence and investment plans. Trade growth has stalled, restrictions are having marked sectoral effects and the level of uncertainty on trade stances remains high.”

So “It is urgent for countries to end the slide towards further protectionism, reinforce the global rules‑based international trade system and boost international dialogue, which will provide business with the confidence to invest,”.

And as for the so-called emerging markets, the situation continues to deteriorate. According to the IIF, growth tracker, emerging market growth is now at a two-year low.

And as interest rates globally rise (driven by the Fed) and trade wars begin to squeeze global trade, emerging markets with high corporate debt are especially vulnerable.

The right-wing government of Argentina has now had to swallow a record-breaking IMF bailout of $57bn. IMF chief Lagarde said that, as part of the deal, Argentina’s central bank can only intervene to stabilize its currency if the peso depreciates below 44 pesos to the dollar. It is currently at 39 pesos to the dollar after losing 50% of its value since the start of the year. The president of Argentina’s central bank, Nicolás Caputo, resigned because of this condition.

The size of the bailout shows how desperate the IMF is to support the right-wing government in Argentina, but also to remove any independent action by the Argentine monetary and fiscal authorities. Argentina’s economic policy is now being run by the IMF. Argentina is now under the grip of IMF dictates, something the right-wing Macri government said would never happen again. A massive slump and austerity will now follow for the Argentine people – repeating the hell of the last major slump of 2001.

At the same time, the Turkish economy is in meltdown. There the Erdogan government refuses to take IMF money in return for austerity and control over its currency and interest rate policy – unlike Argentina. But it will make no difference: both countries cannot avoid a serious slump as interest rates spiral and inflation rockets.

There is one economic lesson to be learned here. When Greece was locked in the straitjacket of the so-called Troika (the IMF, the ECB and the Euro group), many Keynesians and radicals said that the reason Greece was in this mess was that it was inside the Eurozone and so it could not devalue its currency or control its interest rates. If it broke away, it could control its own destiny.

Well, Argentina and Turkey now show that it was not the Eurozone as such that was the problem, but the forces of global capitalism. Both Argentina and Turkey control their currency and interest rate policy. The former has opted for IMF control and the latter refuses it. But it will make no difference – the working people in both countries will pay the price for the crisis in their economies.

No comments:

Post a Comment