by Michael Roberts

Larry Summers is one of the world’s leading Keynesian economists, a former Treasury Secretary under President Clinton, a candidate previously for the Chair of the US Fed, and a regular speaker at the massive ASSA annual conference of the American Economics Association, where he promotes the old neo-Keynesian view that the global economy tends to a form of ‘secular stagnation’.

Summers has in the past attacked (correctly in my view) the decline of Keynesian economics into just doing sterile Dynamic Stochastic General Equilibrium models (DSGE), where it is assumed that the economy is stable and growing, but then is subject to some ‘shock’ like a change in consumer or investor behaviour. The model then supposedly tells us any changes in outcomes. Summers particularly objects to the demand by neoclassical and other Keynesian economists that any DSGE model must start from ‘microeconomic foundations’ ie the initial assumptions must be logical, according to marginalist neoclassical supply and demand theory, and the individual agents must act ‘rationally’ according to those ‘foundations’.

As Summers puts it: “the principle of building macroeconomics on microeconomic foundations, as applied by economists, contributed next to nothing to predicting, explaining or resolving the Great Recession.” Instead, says Summers, we should think in terms of “broad aggregates”, ie empirical evidence of what is happening in the economy, not what the logic of neoclassical economic theory might claim ought to happen.

Not all Keynesians agree with Summers on this. Simon Wren-Lewis, the leading British Keynesian economist claims that the best DSGE models did try to incorporate money and imperfections in an economy: “respected macroeconomists (would) argue that because of these problematic microfoundations, it is best to ignore something like sticky prices (wages) (a key Keynesian argument for an economy stuck in a recession – MR) when doing policy work: an argument that would be laughed out of court in any other science. In no other discipline could you have a debate about whether it was better to model what you can microfound rather than model what you can see. Other economists understand this, but many macroeconomists still think this is all quite normal.” In other words, you cannot just do empirical work without some theory or model to analyse it; or in Marxist terms, you need the connection between the concrete and the abstract.

There is confusion here in mainstream economics – one side want to condemn ‘models’ for being unrealistic and not recognising the power of the aggregate. The other side condemns statistics without a theory of behaviour or laws of motion.

Summers reckons that the reason mainstream economics failed to predict the Great Recession is that it does not want to recognise ‘irrationality’ on the part of consumers and investors. You see, crises are probably the result of ‘irrational’ or bad decisions arising from herd-like behaviour. Markets are first gripped by ‘greed’ and then suddenly ‘animal spirits’ disappear and markets are engulfed by ‘fear’. This is a psychological explanation of crises.

Summers recommends a new book by behavioural economists Andrei Shleifer’s and Nicola Gennaioli, “A Crisis of Beliefs: Investor Psychology and Financial Fragility.” Summers proclaims that “the book puts expectations at the center of thinking about economic fluctuations and financial crises — but these expectations are not rational. In fact, as all the evidence suggests, they are subject to systematic errors of extrapolation. The book suggests that these errors in expectations are best understood as arising out of cognitive biases to which humans are prone.” Using the latest research in psychology and behavioural economics, they present a new theory of belief formation. So it’s all down to irrational behaviour, not even a sudden ‘lack of demand’ (the usual Keynesian reason) or banking excesses. The ‘shocks’ to the general equilibrium models are to be found in wrong decisions, greed and fear by investors.

Behavioural economics always seems to me ‘desperate macroeconomics’. We don’t know why slumps occur in production, investment and employment at regular and recurring intervals. We don’t have a convincing theoretical model that can be tested with empirical evidence; just saying slumps occur because there is a ‘lack of demand’ sounds inadequate. So let’s turn to psychology to save economics.

Actually, the great behavourial economists that Summers refers to also have no idea what causes crises. Robert Thaler reckons that stock market prices are so volatile that there is no rational explanation of their movements. Thaler argues that there are ‘bubbles’, which he considers are ‘irrational’ movements in prices not related to fundamentals like profits or interest rates. Top neoclassical economist Eugene Fama criticised Thaler. Fama argued that a ‘bubble’ in stock market prices may merely express a change in view of investors about prospective investment returns; it’s not ‘irrational’. On this point, Fama is right and Thaler is wrong.

The other behaviourist cited by Summers is Daniel Kahneman. He has developed what he called ‘prospect theory’. Kahneman’s research has shown that people do not behave as mainstream marginal utility theory suggests. Instead Kahneman argues that there is “pervasive optimistic bias” in individuals. They have irrational or unwarranted optimism. This leads people to take on risky projects without considering the ultimate costs – against rational choice assumed by mainstream theory.

Kahneman’s work certainly exposes the unrealistic assumptions of marginal utility theory, the bedrock of mainstream economics. But it offers as an alternative, a theory of chaos, that we can know nothing and predict nothing. You see, the inherent flaw in a modern economy is uncertainty and psychology. It’s not the drive for profit versus social need, but the psychological perceptions of individuals. Thus the US home price collapse and the global financial crash came about because consumers have irrational swings from greed to fear. This leaves mainstream (including Keynesian) economics in a psychological purgatory, with no scientific analysis and predictive power.

Also, it leads to a utopian view of how to fix crises. The answer is to change people’s behaviour; in particular, big multinational companies and banks need to have ‘social purpose’ and not be greedy!

Turning to psychology is not necessary for economics.

At the level of aggregate, the macro, we can draw out the patterns of motion in capitalism that can be tested and could deliver predictive power. For example, Marx made the key observation that what drives stock market prices is the difference between interest rates and the overall rate of profit. What has kept stock market prices rising now has been the very low level of long-term interest rates, deliberately engendered by central banks like the Federal Reserve around the world.

Of course, every day, investors make ‘irrational’ decisions but, over time and, in the aggregate, investor decisions to buy or to sell stocks or bonds will be based on the return they have received (in interest or dividends) and the prices of bonds and stocks will move accordingly. And those returns ultimately depend on the difference between the profitability of capital invested in the economy and the costs of providing finance. The change in objective conditions will alter the behaviour of ‘economic agents’.

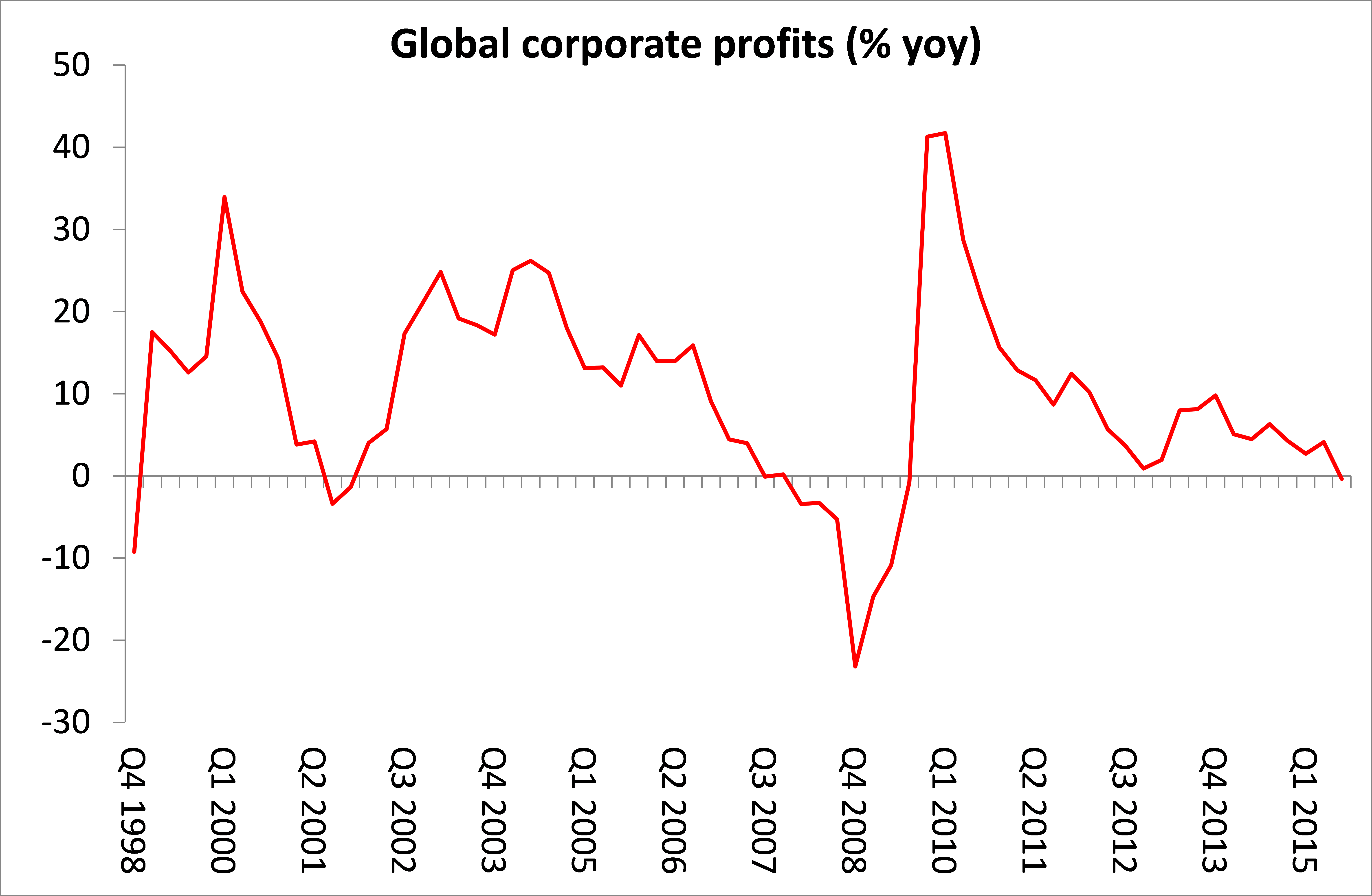

Right now, interest rates are rising globally while profits are stagnating.

The scissor is closing between the return on capital and the cost of borrowing. When it closes, greed will turn into fear.

No comments:

Post a Comment