I have just returned from Brazil where I spoke at the annual Society for Political Economy (SEP) conference at the University Federal Fluminense (UFF) in Rio de Janeiro and at the economics faculties of the Federal University of Rio de Janeiro and the State University of Sao Paolo.

I did so as the currencies of the major so-called emerging market countries dived against the dollar. The moves by President Trump to ‘up the ante’ on tariffs on trade against everybody and the resultant retaliation planned by the EU and China will hit the exports of these economies hard. At the same time, the US Federal Reserve has raised its policy interest rate yet further. That will eventually increase the cost of servicing dollar debt owed by these emerging economies. So the emerging market debt crisis is getting closer. Argentina has already had to go to the IMF for a $50bn loan and its stock market dropped nearly 10% in one day this week. The South African rand is also heading back towards its all-time low against the dollar that it achieved two years ago.

Brazil is part of this new trade and currency crisis. The Brazilian real has taken a hit too, halving in value against the US dollar since 2014 and heading back to a record low since the Great Recession of R$4 to the US$.

Unemployment remains near highs.

And this is at a time when the country is bracing itself for a presidential election in October. The leading candidate in the polls is former president Lula of the Workers Party (PT). But he is languishing in jail convicted on a supposed corruption charge. He is unlikely to be able to stand in October. So the election result is wide open. And with 50% of Brazilians saying that they are not going to vote (even though it is compulsory!), that is an indication of the disillusionment that most Brazilians have with their mainly corrupt politicians and with the prospects of Brazil getting out of its slump that the economy has been since the end of the commodity price boom in 2010.

The Great Recession of 2008-9 hit the economy as everywhere else, but when the prices for Brazil’s key exports (food and energy) also plummeted, the economy entered a deep depression that troughed in 2015-6. The mild recovery from that is now stalling.

The incumbent administration of President Temer came into office through a constitutional coup engineered by right-wing parties in Congress that led to the impeachment of the Workers Party president Dilma Rousseff. From the start, Temer aimed to impose the classic ‘neoliberal’ policies of ‘austerity’ in the form of drastic cuts in public services, reductions in public sector jobs and government investment. Above all, Temer aimed to massacre state pensions. The slump and the high level of public debt were to be paid for by Brazilian households. No wonder Temer’s popularity ratings have slumped to a record low of just 4%. But public sector deficits (now around 8% of GDP) and debt must be brought under control to re-establish business and foreign investor ‘confidence’, so the argument goes.

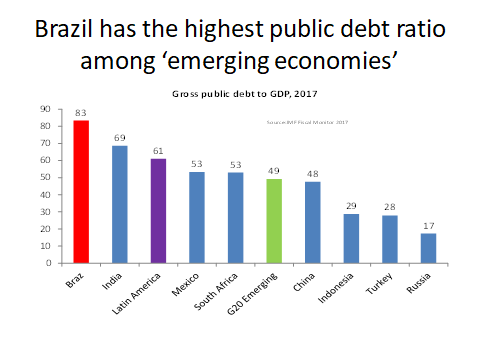

As I showed in a previous post, Brazil has the highest public debt ratio among emerging economies (IMF data).

But as I also showed in that post, the cause of the high budget deficit and debt was not ‘excessive’ government spending on pensions etc. Instead it was continual recurring crises in the capitalist sector and the low level of tax revenue – because the rich do not pay high taxes and continually avoid them anyway, while the majority pay sales taxes that are highly regressive ie. the poorer pay more as a percentage of income than the richer.

The slump has been caused by the collapse of the capitalist sector in Brazil and the cost is being shifted onto the public sector and average Brazilians through austerity measures. The results of the slump and austerity were evident to me on my latest visit to Brazil: in the rundown streets of the cities of Rio and SP; and from the comments of people and the attendees at my meetings on the continual freeze in education and health spending etc – and in the high levels of crime.

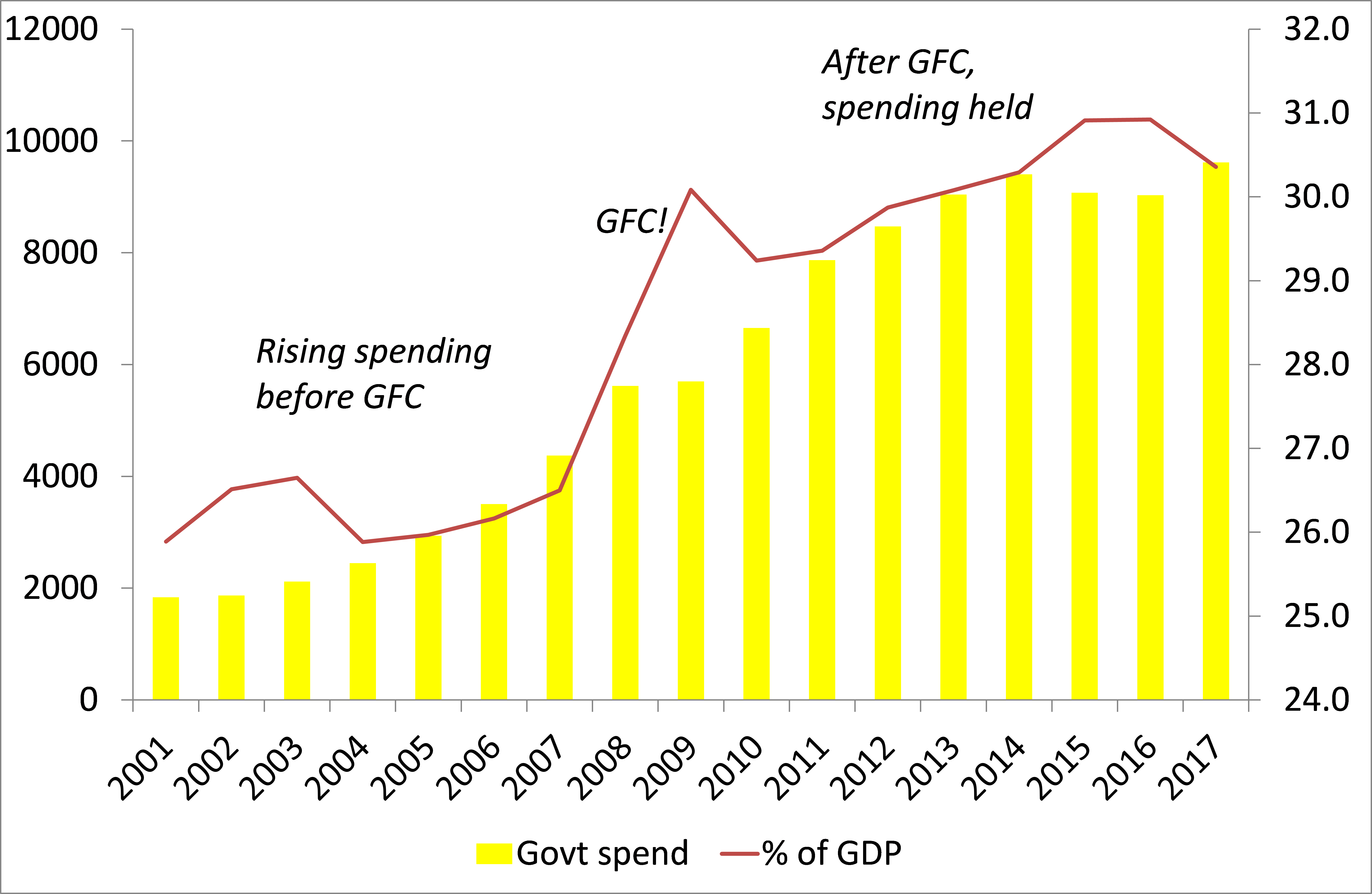

So it was no surprise that SEP asked me to speak on the impact of austerity globally. Austerity, investment and profit. Actually my paper made two points: first, that austerity was not the cause of the slump or Great Recession in global capitalism. On the contrary, government spending was rising in most countries before the crash, as economies globally boomed. See below for state spending in emerging economies (my calcs).

But more important, I wanted to show that, while Brazilians must resist and reverse ‘austerity’ with all their might to protect public services and welfare, just increasing public spending will not solve the underlying problem of capitalist booms and slumps – as the Keynesians claim.

In my paper, I presented both theoretical arguments and empirical evidence to conclude that just boosting government spending will not deliver the sufficient ‘multiplier’ effect on growth, income and jobs wherever the capitalist mode of production dominated. Capitalist production only revives with an increase in profitability and overall profits; and a slump and ‘austerity’ are the ways that capitalism can get out of a crisis – at labour’s expense. I showed that the impact of a rise in profitability on growth under capitalism – what my colleague G Carchedi and I have called the Marxist multiplier – is much greater than boosting government spending (the Keynesian multiplier). So the policy of austerity is not just some ideological pro-market irrationality as Keynesians claim, but has rationality in the context of low profitability for the dominant capitalist sector.

And as I pointed out in my other lectures in Rio and SP universities, the Long Depression continues and now it seems to be entering a new phase (The state of world economy): first, with the growing risk of a major trade war between Trump’s America and everybody else; and second, with the rising cost of debt biting into corporate stability, particularly in ‘emerging economies’ like Brazil. The repayment schedule for debt owed to foreigners will reach a peak next year, as the costs of servicing and ‘rolling over’ that debt will have risen.

And as I have shown before, Brazil has the highest interest costs on debt of all major emerging economies (see BR in the graph below).

The global economy has been experiencing a mild upswing (within the Long Depression) from a near recession in 2016. But in 2018 it looks like growth globally will peak and the underlying low levels of profitability and investment will reappear, along with a new debt crisis in non-financial corporate sector itself, to pose new risks. We shall see.

No comments:

Post a Comment