President Trump has now moved on from steel tariffs (with exemptions for some allies) to the real battle: stopping China from gaining market share in America’s key industries: technology, pharma and other knowledge-based sectors. Can China make further inroads globally or will Trump’s policies stop them?

The first thing to note is where things are right now. Economists at Goldman Sachs, the US investment bank, have looked at the data. They find that “the US position as a global technological leader remains strong. The US’s economy-wide productivity remains high compared to other advanced economies, and its shares of global R&D, patents and IP royalties remain impressive.” China has been catching up though, but in medium value-added goods sectors and hardly at all in knowledge-based tech. So, while overall, the US share of global high-tech goods exports has declined as China’s share has grown, the US trade sector deficits have been concentrated in medium-high-tech goods rather than in the most advanced categories. Indeed, the US share of global knowledge-intensive service exports has held up, contributing to a rising trade surplus and higher employment in those sectors.

Take overall productivity, as measured by output per hour worked. On this broad measure of the productivity of labour, the US remains ahead, even compared to other advanced economies in Europe and Japan. China’s labour productivity level is just 20% of the US, although that is a quadrupling since 2000.

The US continues to invest a relatively large share of its GDP in

research and development. While the US share of global R&D has

declined, in part due to a rapid increase in China’s share, the US

remains the global R&D leader, accounting for nearly 30% of the

world total, about 1.5-2 times the US share of world GDP.

Total patents granted for new inventions show that the US share has

held roughly steady at around 20%. China’s share of total patents

granted has risen very rapidly over the last decade to over 20%, but

most patents granted to Chinese innovators have come from its own

domestic patent office, with far fewer granted abroad. The US share of

the world total of royalties on intellectual property has declined

somewhat as the EU’s has grown, but it remains very large. China’s share

remains negligible. That means US capital is still taking the lion’s

share of global profits in technology.

The modern 21st century US economy relies increasingly on

advanced knowledge and technology sectors for its growth. The share of

US GDP for these sectors is now 38%, the highest of any major economy.

But China is not far behind with 35% of its GDP in these sectors,

amazingly high for a ‘developing’ economy.

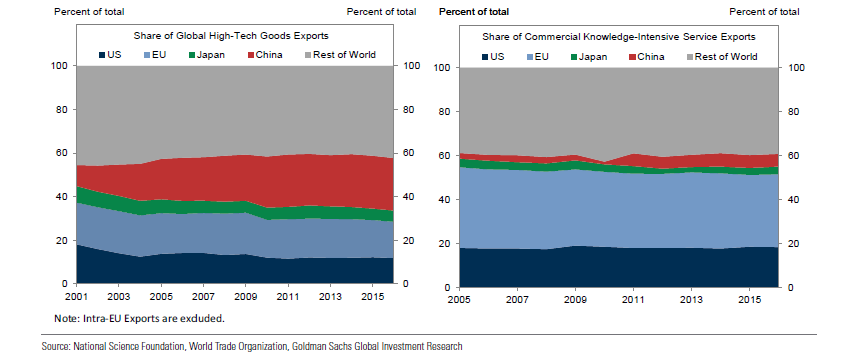

Where Trump is now concentrating his ire on China is on the share of

hi-tech goods sales in world markets. While the US is the largest

producer of high-tech goods, its share of world exports has shrunk

considerably while China’s share has grown. This rising Chinese

competition has caused US manufacturing firms to reduce their patent

production, which has been accompanied by reduced global sales, profits,

and employment.

But on the services side, the US is the largest global producer of

commercial knowledge-intensive services and second only to the EU in

exports. China’s share remains quite small. If China gains market share

in this area, it will really hurt US capital.

That’s because, although the US runs a deficit on trade in tech and

knowledge industries, that deficit has shrunk from the early 2000s. The

US is more than holding its own in this area even since China joined

the World Trade Organisation. Indeed, it runs a surplus in

knowledge-intensive services, which has grown over the last decade. It

is this that Trump seeks to protect.

While jobs have been lost to technology replacing labour (capital-bias)

and the shift of US industry to China in manufacturing, the employment

share of hi-tech and knowledge sectors has risen to about one-third of

all US jobs. Trump claims to be restoring the ‘smoke-stack’ sectors

where he won some votes, but in reality that battle for jobs is already

lost, thanks to US industry shifting out. The real battle is now over

profits and jobs in the knowledge-based sectors where the US still

rules.

But these sectors are highly concentrated in just a few firms, the

technology leaders. There are wide swathes of American industry,

including tech, which benefits little from this US superiority. Just

five firms have over 60% of sales in biotechnology, pharma, software,

internet and comms equipment. The top five in each sector are taking

the lion’s share of profits too.

What this shows is that, contrary to the mainstream economic idea

that international ‘free trade’ will benefit all, the gains from trade

are concentrated in just the leading firms which take advantage of

network, scale, and experience and gain larger market share. The rising

industry concentration has in turn boosted their corporate profit

margins. As Goldman Sachs puts it: “global trade is particularly

concentrated, with “export superstars” accounting for a very large share

of exports in many industries and countries.”

Contrary to the Ricardian theory of comparative advantage,

international trade is transacted by companies not countries and, as

such, value (profit) gets transferred to those with technological

advantage and they gain at the expense of others. Trade represents a

form of combined development, but capitalism delivers this unevenly.

As I argued in a previous post,

over the last 30 years or so, the world capitalist economies had moved

closer to ‘free trade’ with sharp reductions in tariffs, quotas and

other restrictions – and many international trade deals. But since the

Great Recession and in the current Long Depression, globalisation has

paused or even stopped. World trade ‘openness’ (the share of world

trade in global GDP) has been declining since the end of the Great

Recession.

It is this decline in globalisation as world economic growth stays low and the profitability of capital remains squeezed that lies behind this new trade war. Trump’s blundering blows on trade have an objective reason: to preserve US profits and capital in the key growing tech sectors of the world economy from the rising force of Chinese industry. So far, the US is still holding a strong lead in hi-tech and intellectual property sectors, while China’s growth has been mainly in taking market share at home from American companies, not yet globally. But China is gaining.

No comments:

Post a Comment