When it rains, it pours. Hurricane Maria hit the island of Puerto Rico off the US mainland leaving the country devastated with no power, no food and water.

Puerto Ricans are US citizens, as the island is officially a ‘US territory’ – in effect, a colony like the French overseas territories. But the US mainland authorities did little to help and when they did, it was inadequate. Power remains lost; homelessness continues and President Trump visited the most well-off part of the island to hand out paper towels – to mop up no doubt!

But even before the hurricane, Puerto Rico’s 3.5m people were in a parlous state. It had become a graphic example of what capitalism and colonial rule can do in exploiting the resources and people, through distortions of the local economy and corruption of local and foreign institutions. Puerto Rico was faced with bankruptcy even before the hurricane. By bankruptcy, I mean that the public sector debt of the island had reached astronomical levels, making it impossible for the island government to service the debt and thus facing default on its bonds owned by local and foreign institutions (mainly hedge funds).

How did this come to pass? Throughout the modern economic history of Puerto Rico, one of the central drivers of its economic growth has been the US tax code. For over 80 years, the US federal government granted various tax incentives to US corporations operating in Puerto Rico. Most recently, beginning in 1976, section 936 of the tax code granted corporations a tax exemption from income originating from ‘US territories’. US corporations benefited greatly from locating subsidiaries in Puerto Rico – a ‘rich port’ indeed. Income generated by these subsidiaries could be paid to U.S. parents as dividends, which were not subject to corporate income tax.

Puerto Rico thus became a large tax scam for multi-nationals. The main ‘exporters’ to Puerto Rico were pharma and chemical companies in Ireland, Singapore and Switzerland. Thus Puerto Rico imported pharmaceutical ingredients from low-tax jurisdictions like Ireland and then exported finished pharmaceuticals to high-tax jurisdictions in Europe and the US.

As top economist Paul Krugman recently noted: “Specifically, PR runs, on paper, a huge trade surplus in pharmaceuticals – $30 billion a year, almost half the island’s GNP. But the pharma surplus is basically a phantom, driven by transfer pricing: pharma subsidiaries in Ireland charge themselves low prices on inputs they buy from their overseas subsidiaries, package them, then charge themselves high prices on the medicine they sell to, yes, their overseas subsidiaries. The result is that measured profits pop up in Puerto Rico – profits that are then paid out in investment income to non-PR residents. So this trade surplus does nothing for PR jobs or income.”

This booming economy raised little tax revenue. So Puerto Rican governments borrowed to provide public services rather than tax mulit-nationals. Due to these extensive tax credits and exemptions, Puerto Rico lost out on $250-$500 million a year in revenue. It did this for four decades, encouraged by financial consultants. Soon it entered the realm of Ponzi-financing, namely, issuing debt to repay older debt, as well as refinancing older debt possessing low interest rates with debt possessing higher interest rates.

Then disaster happened. In the US, section 936 became increasingly unpopular throughout the early 1990s, as many correctly saw it as a way for large corporations to avoid taxes. Ultimately, in 1996, President Clinton signed legislation that phased out section 936 over a ten year period, leaving it to be fully repealed at the beginning of 2006.

Without section 936, Puerto Rican subsidiaries of U.S. businesses were subject to the same worldwide corporate income tax as other foreign subsidiary. They fled the island. Between 1996 and 2006, the US Congress eliminated the tax credits, contributing to the loss of 80,000 jobs on the island and causing its population to shrink and its economy to contract in all but one year since the Great Recession.

At first, the Puerto Rican government tried to make up for the shortfall by issuing bonds. The government was able to issue an unusually large number of bonds, due to dubious underwriting from financial institutions such as Spain’s Santander Bank, UBS, and Citigroup. According to a report from Hedge Clippers, Santander issued almost $61 billion in bonds from the Puerto Rican government through subsidiaries that serve as municipal debt underwriters, obtaining $1.1 billion in fees in the process. Santander officials were also officials of the Puerto Rico’s Government Development Bank.

Thus Santander officials decided whether to issue debt for Puerto Rico and then arranged that Santander should pocket the fees for organising the bond issues! They also decided that sales tax revenue that should have gone to the government should be siphoned off to COFINA (PR Sales Tax Financing Corporation) bonds, more debt to be issued underwritten by Santander and other banks. They even assigned government employees’ pension contributions to pay for bond issues.

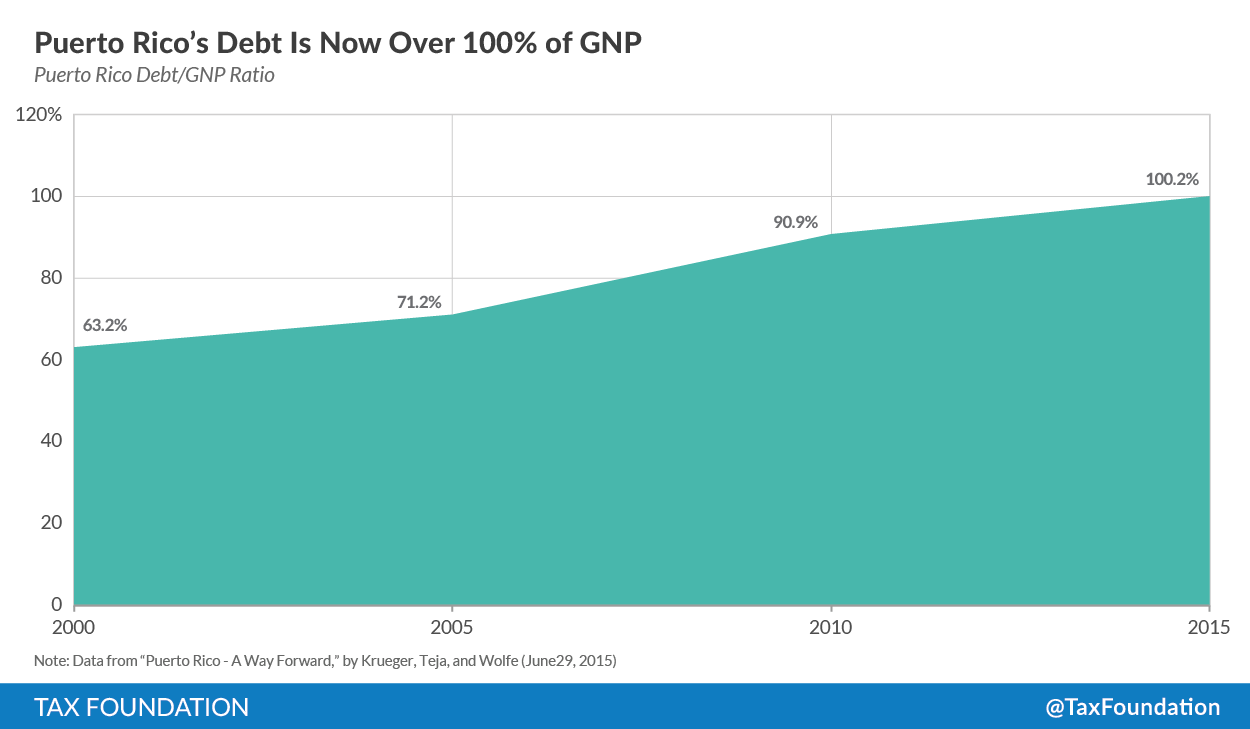

Not coincidentally, 2006 also marked the beginning of a deep recession for Puerto Rico, which has lasted until today. Between 2000 and 2015, Puerto Rico’s debt rose from 63.2% of GNP to 100.2% of GNP. Eventually the debt burden became so great that the island was unable to pay interest on the bonds it had issued.

The tax regime remains paralysed. The Department of Treasury of Puerto Rico is incapable of collecting 44% of the Puerto Rico Sales and Use Tax (or about $900 million). Public spending is also distorted. A public teacher’s base salary starts at $24,000 while a legislative advisor starts at $74,000. The government has also been unable to set up a system based on meritocracy, with many employees, particularly executives and administrators, earning large salaries while health workers struggle.

The Puerto Rico Electric Power Authority (PREPA) provides free electricity to local governments. The utility had improperly given away $420 million of electricity and that the island’s governments were $300 million delinquent in payments. As a result, PREPA had no funds to invest in new technology and built up a debt of $9 billion. In 2012, the Puerto Rico Ports Authority was forced to sell the Luis Muñoz Marín International Airport to private buyers after PREPA threatened to cut off power over unpaid bills. Last July, PREPA filed for bankruptcy.

The island’s unemployment rate is now 14.8% with a poverty rate of 45%. But the Puerto Rican authorities have been under pressure from the US government to apply vicious austerity measures. More than 60% of Puerto Rico’s population receives Medicare or Medicaid services but the US has a cap on Medicaid funding for US territories. This has led to a situation where Puerto Rico might typically receive $373 million in federal funding a year, while, for instance, Mississippi receives $3.6 billion.

The austerity programmes imposed on the Puerto Rican governments have meant taxes and fees went up on nearly everything and everyone. Personal income taxes, corporate taxes, sales taxes, sin taxes, and taxes on insurance premiums were hiked or newly imposed. The retirement age for teachers was raised.

As the debt mounted, the US government removed the power of managing and monitoring that debt out of the hands of the Puerto Ricans and put into a new monitoring body, PROMESA (The Financial Oversight and Management Board for Puerto Rico) – a bit like how the EU governments took control of Greek finances and provided with ‘conditionalities’ through the EFSF and ESM. There is only one Puerto Rican on the PROMESA board. PROMESA’a main aim to service the debt not restore the economy. Puerto Rico’s $123 billion liabilities from debt ($74 billion) and unfunded pension obligations ($49 billion) are much larger than the $18 billion Detroit bankruptcy,

What is to be done? Since it was installed, PROMESA has begun outlining and implementing deep government spending cuts. There is talk that the government should pay back its bonds before providing essential services to its citizens. Though repayment is still on hold, different classes of bondholders are now locked in a legal dispute about which of them is entitled to the revenue from the island’s sales tax, currently set at 11.5%.

PROMESA wants the Puerto Rican government to maintain a balanced budget for four consecutive years and carry out significant privatisations of state assets. For Puerto Ricans, that could mean austerity measures for the foreseeable future imposed by an unelected body based outside Puerto Rico. As economist Joseph Stiglitz recently put it: “The PROMESA Board was supposed to chart a path to recovery; its plan makes a recovery a virtual impossibility. If the Board’s plan is adopted, Puerto Rico’s people will experience untold suffering. And to what end? The crisis will not be resolved. On the contrary, the debt position will become even more unsustainable.”

And yet the foreign bond holders do not think this is enough and condemn PROMESA for being too weak. A group of 34 hedge funds that specialize in distressed debt —sometimes referred to as vulture funds—hired economists with an IMF background. Their report called for increased tax collection and a reduction of public spending and wanted public private partnerships and the ‘monetization’ (privatisation) of government-owned buildings and ports. Another group goes even further.

They called on the US Congress to “consider a tax credit for U.S. multinationals” and the “militarization of the island to provide short to medium [term] security.” They want PROMESA closed down and to be replaced by an “administrator who has broad authority to execute contracts, coordinate with federal agencies and oversee reconstruction.” The bondholders want more police and the US army to enforce austerity. “The U.S. military needs to supplement the 15,000 Puerto Rican police officers to maintain law and order”, while at the same introducing tax allowances at 100% of capital expenditures “required to rebuild after Maria or build new factories within a 2-3 year window.”

Another idea is for all the outstanding debt to be incorporated into a ‘super bond’ that would get interest directly from the tax revenues of the Puerto Rican government This plan would have a designated third party administer an account holding some of the island’s tax collections and those funds would be used to pay holders of the superbond. The existing Puerto Rican bondholders would take a haircut on the value of their current bond holdings. This is almost an exact replica of the private sector involvement (PSI) deal that was imposed on the Greek government in 2012 that led to a bailout off private bondholders and the shifting of the bulk of debt onto the government books.

Is there any way out for the Puerto Rican people or do they face permanent austerity and misery? One solution coming from the left is for the US Federal Reserve Bank to buy up all the Puerto Rican bonds at current market value and then not impose any interest payment burden on the island. This is both useless and utopian at the same time. Even if it were applied, the debt would remain on the books and its servicing subject to the whim of the Federal Reserve Board (and who knows who the Fed Chair would be next year?). Moreover, if the Fed offers to pick up the bill, the price of the bonds would rocket, enabling the ‘vulture funds’ to make a killing at the US taxpayers expense. And it still does nothing to solve the economic problem for the island that created this debt in the first place. And, second, it is utopian because it ain’t going to happen: the Fed will do nothing.

Clearly, the most effective immediate answer is to cancel the debt. But that poses its own problems. First, 40% of the debt is locally held, often by local banks and pension funds that could be bankrupted – so they would have to be brought under the public umbrella. Second, cancellation would mean immediate confrontation with the US authorities and the hedge funds – which could lead to the closure of PROMESA and the imposition of a US administrator to take over the government. In other words, cancellation would mean a major political struggle on the island.

And what sort of Puerto Rican economy is needed anyway? The model of a tax haven that encourages multi-nationals to engage in transfer pricing scams has failed to deliver incomes and jobs for those Puerto Ricans who have not left the island.

Puerto Rico was an important hub, in particular, for big pharmaceutical firms like Pfizer, which have kept many of their investments on the island even after ‘936’ was gradually ended. But Puerto Rico is no longer competitive in areas where 75-80% of expenses come from payroll costs. Puerto Rico needs to move up into higher-value manufacturing and services. It has a large number of educated bilingual workers. There is potential to turn the economy into a modern hi-tech service sector. But that would require government investment and state-run firms democratically controlled by Puerto Ricans. It’s the Chinese model, if you like.

Puerto Rico is a small island that was exploited by the US and foreign multi-nationals with citizens’ tax bills siphoned off to pay interest on ever increasing debt, while reducing social welfare – all at the encouragement of foreign investment banks making huge fees for doing so. Now Puerto Ricans are being asked to keep on paying for the foreseeable future after a decade of recession and cuts in living standards to meet obligations to vulture funds and US institutions. And the troops will be sent into ensure that! When it rains, it pours.

No comments:

Post a Comment