It is not possible to reach conclusions Robert's reaches if one doesn't understand this basic fact and the contradictions and consequences of such social organization like the tendency of the rate of profit to fall due to what Marx called the rise in the organic composition of capital. Working people can grasp the fundamentals of this economic world view as it really does objectively merge with our life experience. Understanding the general processes at work in any science, including social science, can ground us in reality and assist us down the revolutionary path to change objective conditions, alter the world around us. Building a living breathing social force (organization) that can assure a correct idea becomes accepted by millions in society is the task facing us and all workers must play a role in that. Like all phenomena, there are the general processes at work and more complex aspects of it that must be studied if we are to fully understand it. Understanding the former is enough up to a point, for the moment, the latter I will leave to Michael Roberts and his colleagues. RM

by Michael Roberts

I’ve just returned from Cluj, Romania’s second largest city, where I discussed the Euro crisis and the future of Europe with Mark Blyth of Brown University. Mark Blyth has published a number of books, including Austerity: a dangerous idea, which covers the history of the austerity doctrine as he sees it and its impact on the global financial crisis and on Europe’s economies.

The intellectual think-tank, Tranzit, organised the event brilliantly and it was very well attended. The discussion was billed as a debate between a Keynesian and Marxist analysis of Europe’s economic crisis. But, of course, there were many areas of agreement between Mark and myself on the events leading up to the global financial crash and subsequent slumps particularly in the periphery of the Eurozone and on the impact of the policies adopted by the European leaders and the Troika with the distressed states of Ireland, Portugal, Spain and Greece.

In my presentation, I argued that the great European project that started after the second world war had two aims: first, it was to ensure that there were never any more wars between European nations; and second, to make Europe as an economic and political entity to rival America and Japan in global capital. This would be led by Franco-German capital.

The move to a common market, customs union and eventually the political and economic structures of the European Union was a relative success. The EU-12-15 from the 1980s to 1999 managed to achieve a degree of harmonisation and convergence: the weaker capitalist economies growing faster than the stronger.

But the move towards further integration with a single currency and the enlargement of the EU to now 28 (soon 27) countries was not so successful. Now it was divergence, not convergence that was the result: the weaker capitalist economies (in southern Europe) within the euro area lost ground to the stronger (in the north).

Franco-German capital expanded into the south and east to take advantage of cheap labour there, while exporting outside the euro area with a relatively competitive currency. But the weaker states built up trade deficits with the northern states and were flooded with northern credit and capital that created property and financial booms out of line with growth in the productive sectors of the south.

This divergence was exposed in the global financial crash and the ensuing Great Recession. The banking system of the southern states was driven to bankruptcy as property prices collapsed and companies and households were unable to meet their debt servicing costs. This also put French and German banks at risk. The weaker governments could not bail out their own banks without help and that meant agreeing to drastic austerity measures from the EU’s stability funds and the IMF.

At debate in Cluj, in my view, were two things: why did the period of success for the EU project turn into failure with the global financial crash? And was the imposition of austerity programmes the main cause of the depression after the collapse in Portugal, Greece etc; or at least, would a reversal of those Troika-style measures have got Greece etc out of trouble?

My view was that the cause of the change from fast growth and convergence from the 1970s to slow growth and divergence from the 1990s can be found in the sharp decline in the profitability of capital in the major EU states (as elsewhere) after the end of the Golden Age of post-war expansion.

This led to fall in investment growth, productivity and trade divergence. European capital, following the model of the Anglo-Saxon economies, adopted neo-liberal policies: anti trade union laws, deregulation of labour and product markets, free movement of capital and privatisations. The aim was to boost profitability. This succeeded at least for the more advanced EU states of the north but less so for the south.

The introduction of the euro added another limitation on growth in the south and convergence with the north. The euro was not an ‘optimal currency union’ (to use the mainstream economics term) because of this. A strong euro was bad for exports in the south and gave investment power to the north. The debts being built up by the south with the north were exposed in the crash and sparked the ‘euro crisis’, but only after the global financial crash.

The EU leaders had set criteria for joining the euro, but these criteria were all monetary (interest rates and inflation) and fiscal (budget deficits and debt). They were not convergence criteria for productivity levels, GDP growth, investment or employment. Why? Because those were areas for the free movement of capital (and labour) and capitalist production for the market; and not the province of interference or direction by the state. After all, the EU project is a capitalist one. Thus some countries clearly unable to converge were still incorporated into the euro area (Greece, Italy).

The imposition of austerity measures by the Franco-German EU leadership on the distressed countries during the crisis was the result of this ‘halfway house’ of euro criteria. There was no full fiscal union (automatic transfer of revenues to those national economies with deficits) and there was no automatic injection of credit to cover capital flight and trade deficits – as there is in full federal unions like the United States or the United Kingdom. Everything had to be agreed by tortuous negotiation among the Euro states.

Why? Because Franco-German capital was not prepared to pay for the ‘excesses’, or the problems of the weaker capitalist states. Thus the bailout programmes were combined with ‘austerity’ to make the people of the distressed states pay with cuts in welfare, pensions and real wages, to repay (virtually in full) their creditors, the banks of France and Germany and the UK. Eventually, this debt was transferred to the EU state institutions and the IMF – in the case of Greece, probably in perpetuity.

But would a reversal of austerity on its own have turned these economies around without the pain of huge cuts in living standards? In the debate, I argued that it would not. The evidence shows that there is little correlation between faster growth and more government spending or bigger budget deficits. Indeed, during the Great Recession and subsequently, many countries with faster economic growth also had low government spending and budget deficits (see the graph below – if austerity causes poor growth, the line should be sharply from bottom left to top right, but it is nearly flat). It seemed that faster economic growth was more dependent on other factors – in particular, more investment and in turn higher profitability.

The evidence shows that those EU states that got quicker recovery in profitability of capital were able to withstand and recover from the euro crisis (Germany, Netherlands etc), while those that did not improve profitability stayed deep in depression (Greece).

Reversing austerity or leaving the euro and devaluing would not do the trick. I used the example of tiny Iceland that did renegotiate its debts and devalued its currency, but it made little difference to the hit that the Icelandic people took in living standards, because, in this case, inflation rocketed to eat into real wages. In contrast, Estonia and Ireland adopted austerity measures. But what enabled these economies to turn round and raise profitability was mass emigration of their workforces, which drove down the costs of capital (internal devaluation).

But so weak and corrupt was Greek capital that even drastic austerity and mass emigration have not raised up the economy on a capitalist basis.

Thus my argument was that we can look for the main cause of the crisis in the euro in the falling profitability of capital in Europe prior to the crisis, which was then triggered by the global financial crash and Great Recession.

Now Mark had a different analysis. First, he pointed out that profits as a share of GDP in the US are near record highs, so how could the crisis be caused by low profitability or profits? The American multi-nationals are rolling in money and cash; and tax havens are bulging with hidden profits.

Sure, we could agree that the undeniable drop in profitability in the 1970s played a role in the growing difficulties for the EU project and the introduction of neo-liberal policies. But, in his view, as I understand it, it was these neo-liberal policies attacking real wages that caused the crisis of 2008-9, not falling profitability. Real wages were held down and so the rising gap between production and consumption had to be filled by a huge expansion of credit (financialisation). This eventually came tumbling down and kicked off the financial crash.

This analysis is basically the ‘post-Keynesian’ one in economic parlance and Mark mentioned several times the leading post-Keynesian Michal Kalecki in this context. In this theory, crises are the product of the change in the distribution of product between profits and wages. The crisis and stagflation of the 1970s was ‘profit-led’, when strong and confident labour forces forced up wages and squeezed profits and full employment led to inflation (Phillips curve style). But the crisis of 2008 was ‘wage-led’, as wage share in the economy had plummeted and excess (household) credit designed to sustain consumption led to financial instability and collapse (Minsky-style). Marx’s law of profitability of capital based on a rising organic composition of capital (not the distribution between profits and wages) was irrelevant to this narrative.

The 1970s was an era of profits squeeze and inflation. According to Mark, this period of ‘stagflation’ (low growth and inflation) was ‘abnormal’; it did not fit into the post-Keynesian analysis that argues that only a full employment economy would generate inflation – as measured by the so-called Phillips curve that shows a trade-off between full employment and inflation. But by the end of the 1990s, inflation had returned to ‘normal’ levels and now the problem was the post-Keynesian one of ‘wage squeeze’ and ‘underconsumption’. In this period of ‘secular stagnation’ huge injections of credit did not drive up inflation as the monetarist economists expected but merely fuelled financial speculation and instability.

Now, in my view, this post-Keynesian analysis fails theoretically and empirically. Was the 1970s collapse in profitability caused by wages rising too high and squeezing profits? The empirical evidence shows that profitability was falling by the mid-1960s, well before any perceived rise in ‘wage share’ in the major economies. And this coincided with a rise in the organic composition of capital, as in Marx’s law of profitability. Profits squeeze only came later in the early 1970s. As Marx said in Capital Volume 3 (p239): “The tendency of the rate of profit to fall is bound up with a tendency of the rate of surplus-value to rise, hence with a tendency for the rate of labour exploitation to rise. Nothing is more absurd, for this reason, than to explain the fall in the rate of profit by a rise in the rate of wages, although this may be the case by way of an exception.”

If profits are the result of the exploitation of labour power and not merely the result of the distribution of production between wages and profits, then it is profits that matters for capital, not wages. Keeping wages down and profits up is good for capital accumulation. The contradiction does not lie in the wage-profit nexus but in the limitation in the increase in the productivity of labour as a counteracting factor to the tendency of the rate of profit on overall capital to fall.

Profit share in GDP may be at highs (at least in the US) – although its has been falling back recently. But this only measures profit per output or profit margins, not profits against the stock of capital accumulated and invested in an economy. Rising profit margins show capital is making bigger profits; but that can still mean overall profitability is falling. Yes, many large multinationals are ‘awash with cash’, but there are also many more companies making only enough profit to service their debts (zombie companies) and corporate debt to GDP in most economies is at record high levels too.

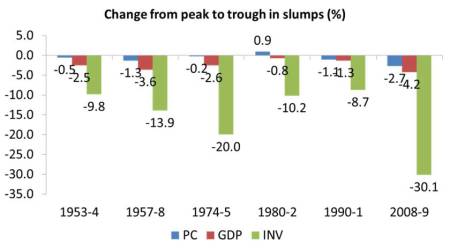

Yes, corporations squeezed the share of value added going to wages from the 1980s to boost the rate of surplus value and reverse falling profitability. But it only had limited success. By the early 2000s as the euro area started, profitability was falling across the major economies. Indeed, far from wages and consumption collapsing prior to the Great Recession, as the post-Keynesian thesis would suggest, it was profits and investment that did so, as the Marxist thesis would argue (graph shows inv in green and cons in blue).

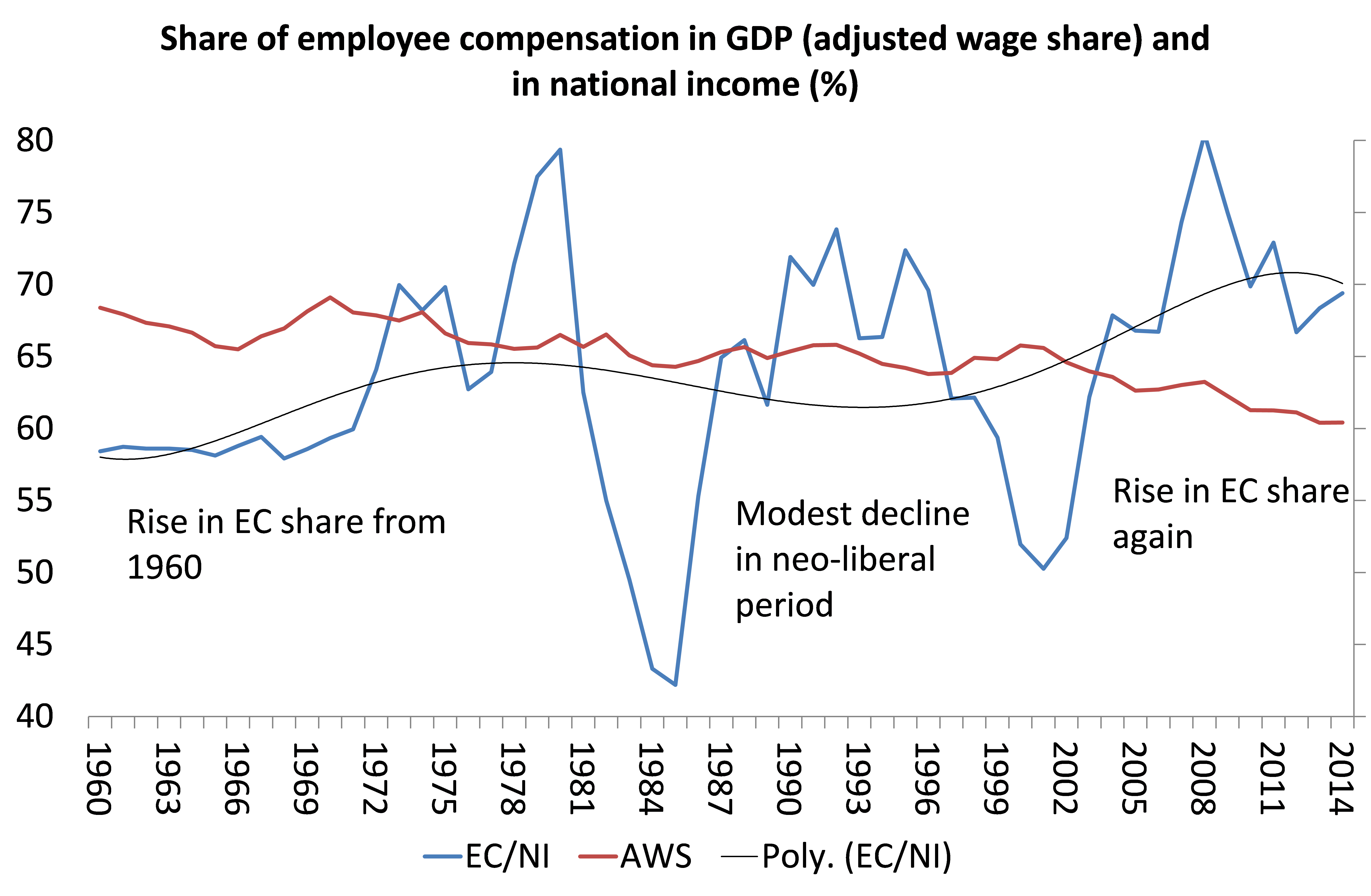

Actually, over the period from the 1980s, wage share in most economies did not decline that much. And when adjusted for social benefits, the share of total value going to labour was pretty stable. In the graph below, the wage share for the US is measured against GDP and against national income. Following the blue line, we can see that the ‘profits squeeze’ only began in the early 1970s (well after profitability fell). Following the average black line, we can see that employee compensation to national income was pretty stable, if not rising in the post war period.

US personal consumption to GDP rose, not so much because of rising household debt filling the gap between output and wages, but because wages from work were supplemented by health and social benefits (so the green line below more than matches the blue line of personal consumption share).

Finally, there are policy implications from these rival theses. If the euro crisis and the Great Recession were the product of wage compression and too much credit, then the solution for the EU project may just be better taxation of profits, more wage increases and public spending. In other words, we need a return to the social democratic consensus of the Golden Age, when apparently the right balance between profits and wages was achieved.

Indeed, this scenario is exactly the view and policy objective of post-Keynesian analysis. Two leading post-Keynesians summed thus up in a recent paper, when they said: “in contrast to other heterodox economists, especially from the Marxian tradition, Post-Keynesians believe that it is possible even within a capitalist economy to counteract effectively these destabilizing tendencies through appropriate macroeconomic policy actions of the state, as long as the political conditions are in place, as it happened to some extent during the early post-World War II “Golden Age”, especially as implemented by certain social democratic regimes, which had held power on the European continent and who were committed to full employment.” I assume this was at least one reason why Mark Blyth, when asked in Cluj, said that “je ne suis pas Marxist”.

However, if the cause of the euro crisis is be found in the main contradiction within capitalist production for profit, namely the law of the tendency of the rate of profit to fall (which brings about recurring and regular slumps in production whatever the ratio of distribution between profits and wages), then a managed solution within capitalism is not possible. Crises would still re-occur. And indeed, austerity then has a certain rationality in the very irrationality of capitalism, as it aims to raise profitability, not production or wages.

It is a vain hope that we could return to the golden age where wages and profits were ‘balanced’ (apparently) to avoid crises. Modern capitalist economies are not generating high levels of profitability, full employment and investment as in the 1950 and 60s – on the contrary, they are depressed. And they are depressed not by the lack of consumption (US personal consumption to GDP is at its height), but by the lack of sufficient profitability, notwithstanding Apple or Amazon’s huge cash piles.

If there was an abnormal period, it was not the ‘stagflation decade’ of the 1970s where the Phillips curve did not operate, as Mark argued. It was the Golden age of the 1950s and 196os, when profitability was high after the war and capital could make concessions to labour (under pressure) for higher wages and a welfare state. Indeed, the Phillips curve is still not operating as Keynesians and post-Keynesians expect. Where is that curve?; it should be from the top left to the bottom right, but it was nearly flat in the 1970s and it is even flatter now.

Japan, the US and the UK now have record low unemployment rates and yet wages stay low and inflation is virtually non-existent (speech984). Instead of stagflation, economies have stagnation. Now capitalism is in a new ‘abnormality’, if you like, a long depression, where it can concede nothing to labour, certainly not a social democratic consensus to balance profits and wages.

No comments:

Post a Comment