Koreans have decided to impeach their President Park Geun-hye over corruption charges. Last Friday the country’s top court upheld an earlier impeachment vote, officially ousting Park Geun-hye, South Korea’s first female leader, from office. This follows months of protests by South Koreans alarmed at claims of bribery, influence-peddling and even shamanistic cult rituals in the presidential Blue House. The demonstrations were more than 1m strong. An impeachment motion easily passed the legislature.

Park is the most unpopular South Korean leader since the country became a democracy in the late 1980s. The scandal ensnared senior government officials and business figures, including Lee Jae-yong, the acting head of Samsung, who denied bribery, corruption and other charges at the first hearing in his trial last week. Samsung apparently donated 43bn won ($40m) – more than any other firm – to the foundations run by the president’s confidant, Choi Soon-sil.

Choi is the Rasputin to Korea’s Park. She is the daughter of a South Korean Shamanistic–Evangelical cult leader, Choi Tae-min. Her ex-husband is Park’s former chief of staff Chung Yoon-hoi and dressage athlete Chung Yoo-ra is their daughter. Samsung allegedly gave millions of euros to fund Choi’s daughter’s equestrian training in Germany. Choi is in detention, accused of using her close ties with Park to force local firms to “donate” nearly $70m (£60m) to her non-profit foundations, which Choi allegedly used for personal gain.

It looks likely Moon Jae-in, a former human rights lawyer and political veteran from the opposition Democratic party, will win snap presidential polls in May. Mr Moon has won admirers among the country’s younger generation for his “progressive values” and pledges to tackle youth unemployment, which stands at a record high since the Asian crisis of 1997-8. Despite what his opponents say, he is no communist.

Korea’s political turmoil is yet another example of how incumbent governments around the world have suffered the price of failure and exposure since the Long Depression began in 2009 after the global financial crash of 2007 and the Great Recession of 2008-9.

The mainstream view is that Korea is a capitalist success story. Unlike other so-called ‘emerging economies’ in the post 1950 period, which have struggle to close the gap in output and living standards with the leading imperialist countries like the US, the UK or Japan, Korea has made substantial progress. Between 1960s and the 1980s, Korea’s economy expanded by an average of 8% a year in real national output. Per capital GDP rose from $104 in 1962 to $5,438 in 1989, and reached the $20,000 level just before the global financial crash. So per capita income rose from 5% of the US in 1960 to around 55%.

This progress was made possible because Korea embarked on, and adhered to, a state-directed industrialisation and export strategy for nearly 50 years. The manufacturing sector grew from 14.3% of GDP in 1962 to 30.3% in 1987. Within two generations, Korea vaulted into the OECD, its goods and services became known around the globe, and its national corporate champions entered the ranks of the world’s most recognized companies. In 2012, Korea became the seventh global member of the ’20-50′ club (population surpassing 50m with per capita income of $20,000), the supposed definition of a major capitalist economy.

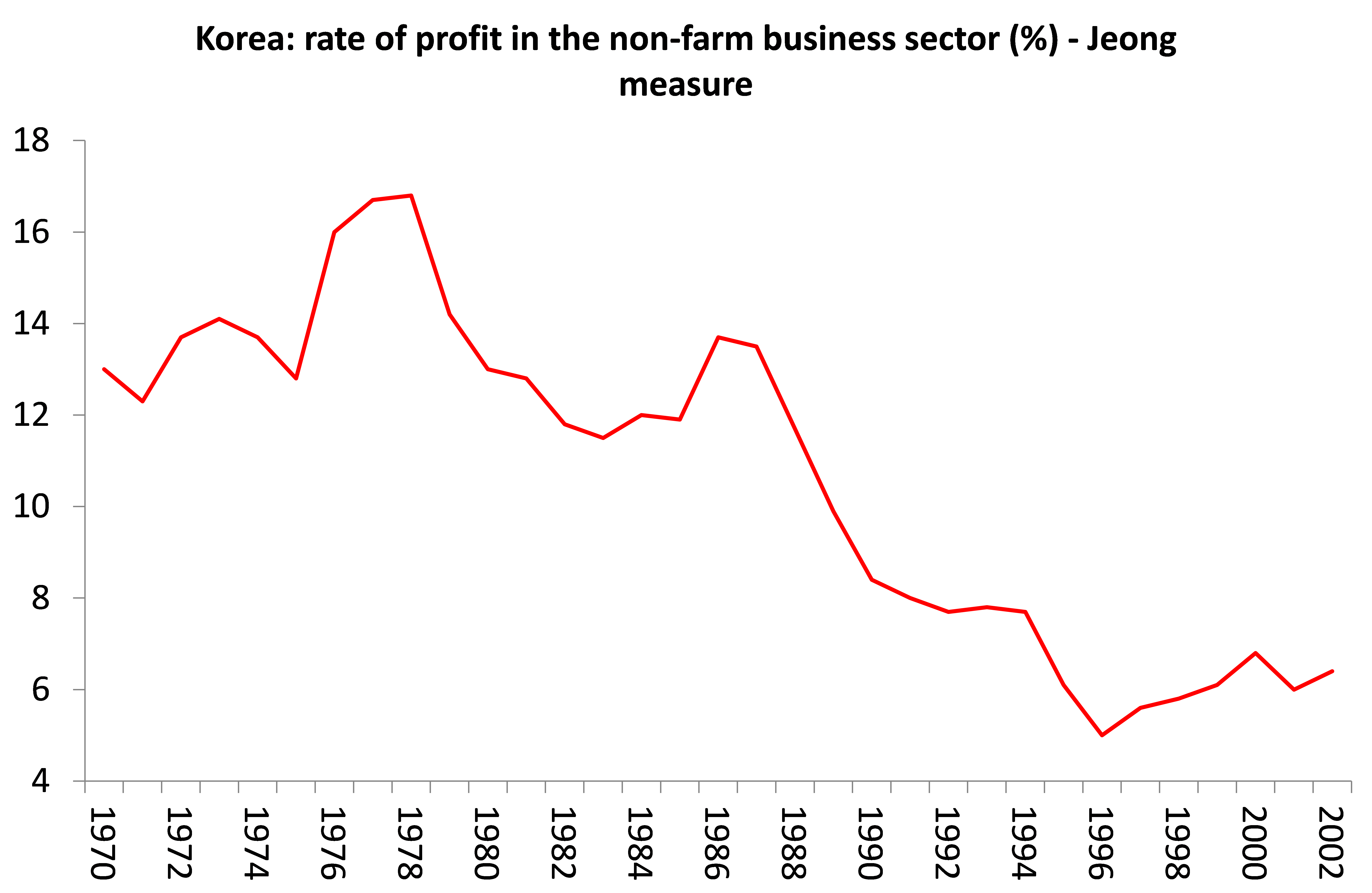

Marx’s law of profitability can provide an underlying explanation of the success of Korean capitalism in the period from the 1960s after the Korean war to the end of the 1970s. While the major capitalist economies experienced a fall in profitability from about the mid-1960s to the early 1980s, Korean capital had high and rising rates of profit. The Korean rate of profit has been measured by several different authors including myself, but probably the best and most thorough measurements have been by Esteban Maito and Seongjin Jeong, the editor of Marxism21.

Maito finds that the Korean rate of profit rose from the 1960s to the late 1970s. (Maito, Esteban – The historical transience of capital. The downward tren in the rate of profit since XIX century ). And that was the peak.

Jeong presents the most comprehensive analysis of trends in the rate of profit on Korean capital. Jeong finds that the rate of profit fell from a peak in 1978 to a low in 2002. And the decline in the rate over the 1980s and 1990s was the underlying cause of the crisis and slump of 1997, part of the so-called Asian crisis. “The 1997 crisis was intimately related to a broader problem of declining capitalist profitability. While the rate of profit has recovered since that crisis”, Jeong says, “its 2002 level still remains at only one-third of the level of 1978. This suggests that the Korean economy remains in the middle of its long downturn.”

Jeong also shows that Marx’s law of profitability, based on a rising organic composition of capital, provides the underlying cause for this fall in profitability. The era of Park Jung Hee, which saw a limited stabilisation of profitability, was only possible because of intensified exploitation of the Korean working class in the so-called neoliberal period of the 1980s, delivering a rise in the rate of surplus value or exploitation, the main counteracting factor to the tendency of the rate of profit to fall. But even that factor could not overcome the eventual fall in profitability in the 1990s that finally culminated in the slump of 1997, ironically just as profitability in the major economies peaked. In the 1997 Asian financial crisis, the South Korean economy suffered a liquidity crunch and had to rely on a bailout by the IMF.

The Asian crisis that hit Korea so hard led to a sharp devaluation of capital values (through the writing off of bankrupt companies and rising unemployment), followed by more neoliberal measures that boosted profitability. But as Maito and my own measures of profitability show, after the 2001 mild global recession, Korean profitability resumed its decline, leading up to the global financial collapse of 2008. Economic growth was stopped in its tracks in 2009.

Since then, Korean capitalism has become part of the Long Depression. Underlying trend growth has weakened from 7% a year in the 1990s to just 3% now.

Moreover, Korean capitalism now faces serious structural challenges, many of which imply a further decline in potential growth. Korea has one of the lowest birth rates in the world and one of the world’s most rapidly aging societies. The working age population is projected to peak this year and decline rapidly thereafter, depressing potential employment and growth. The overall population is expected to start declining after 2025.

Korea’s economic success came on the back of exports, but that heavy reliance may now be a liability in a world of slowing trade and with the prospect of the end of globalisation and the rise of protectionism after the election of President Donald Trump in the US. With exports exceeding 50% of GDP—one of the highest shares among advanced economies—Korea is heavily exposed to any shocks or change in China and the US, particularly from China, its largest trading partner. Some of the heavy industrial sectors that underpinned Korea’s past growth—for instance, shipbuilding, shipping, steel, and petrochemicals—are now facing bleak prospects globally given the trade slowdown and competition from China. Korean capital is under severe pressure.

Moreover, South Korea’s economy is still dominated by oligopolistic chaebol that are now being squeezed at the low end by expanding Chinese manufacturers and at the high end by Japanese players who have benefited from a deliberately-weakened yen. Exporters are creating fewer jobs in South Korea as the chaebol move production offshore to look for cheaper labour. That has left the domestic economy hurting: small and medium-sized businesses are still failing and the high-value services sector is lagging well behind other countries. “This has raised concerns about Korea’s traditional catch-up strategy led by exports produced by large chaebol companies”, the OECD said in a report last year.

In the 1990s, Korean capitalists adopted neoliberal employment policies by keeping much of its workers on casual temporary contracts. The share of temporary workers was nearly 22% in 2014, double the OECD average. But this led to slowing productivity and under-investment in skills. Labor productivity rose at an average annual rate of 5.5% in 1990-2011, but it has stagnated since then and remains only 40% of the three most productive OECD countries. Labor productivity is particularly low in the service sector—much lower than in peer economies and only half that of manufacturing and much lower in smaller companies.

Korean capital prospered on the backs of overworked staff, working long hours and by avoiding any social security. The Basic Livelihood Security Program (BLSP), introduced in 2000, provides cash and in-kind benefits to the most vulnerable, but is substantially less generous than the OECD average. The National Pension System (NPS) currently covers about one-third of the elderly and the OECD reports that pension benefits were only around one-quarter of the average wage in 2015.

This has led to increasing household debt: many retirees borrow to open (risky) small businesses, in an attempt to supplement their incomes. Total social spending amounts to just 10% of GDP, less than half the OECD average, while household debt rose steadily from 40% of GDP in the early 1990s to nearly 90% today. At the same time, corporate debt has been consistently high at about 100% over the last decade. This high and rising debt indicates that Korean capital is no capable of getting a healthy and rising rate of profit and is forced to borrow to grow – increasing the impact of any future slump.

Back in 2012, the now disgraced Park Geun-hye pledged to rebuild the ‘middle class’ and increase its size to 70% of society. This has turned out to be a sham. Instead, there has been increasing economic polarisation in the Long Depression. Economic inequality increased noticeably during and after the 1997 crisis and the Great Recession of 2008-9. South Korea’s average gini coefficient — a measure of inequality — for 1990–1995 was 0.258, but with rising inequality its coefficient increased to 0.298 in 1999. It continued to increase, reaching 0.315 in 2010. The same trend can be seen in income distribution: the share held by the top 10% of income holders divided by that of the bottom 10% has increased from 3.30 in 1990 to 4.90 in 2010. The income share of the top 1% was 16.6% of national income in 2012, not far short of the extremes in the US and much worse than in Japan. The most recent statistics released by a government source indicate that as much as 73% of Seoul residents identified themselves as belonging to the ‘lower class’.

The Great Recession has increased the precarious position of Korean workers and produced an even sharper cleavage between regularly employed workers on standard contracts and irregularly employed workers (those who are limited-term, part-time, temporary or dispatched), increasing the latter from 27% of the working population in 2002 to 34% in 2011. This means that approximately one-third of South Korean workers suffer from insecure job conditions, receiving only around 60% of regular workers’ wages with no medical insurance, severance pay or company welfare subsidies.

Since the late 1990s, a general trend among South Korean firms has been to discard the old seniority-based salary system and adopt the American style ability-based salary system. With this change, the wage gap between professional and managerial workers and the rest of the workforce has widened greatly. As the South Korean economy has moved towards being knowledge-based, the value of scarce skills and knowledge has increased and globalised business sectors have begun to offer extremely high salaries to attract talent.

So significant income disparities that have long existed between South Korea’s conglomerate firms and medium to small-sized firms have become even greater in recent years. South Korea’s top 1% of income earners are most likely to be employed in the leading conglomerates, like Samsung, Hyundai and LG, which have grown into truly world-class companies and become very profitable.

Finally, in South Korea, as in most societies, wealth inequality is much larger than earned income inequality. In 2012, the top 10% of the population possessed 46% of the country’s total wealth. The bottom 50% possessed only 9.5%. This wealth inequality emerged primarily from the booming real estate market. But in recent years, the stock market and other financial investments have replaced the real estate market as the major means of wealth accumulation.

According to Statistics Korea, the average monthly household income of the top 10% was 10,627,099 won. This is 5.1 times higher than that in 1990, which was 2,097,826 won. For the bottom of 10%, the figure increased only 3.6 times from 248,027 won to 896,393 won. So the gap between these two groups increased from 8.5 times to 11.9 times. The data is based on 8,700 households, not including the extremely poor or the top chaebol families, so the actual gap appears to be much larger.

One out of six people live with less than 10 million won per year and one out of four households are more often in the red than in the black. The poverty rate of people over 65 years old is 48.5%, which is 3.4 times higher than that of the OECD average. Moreover, the suicide rate is among the highest in the world. Korean capitalism may appear to have been a relative success by world standards over the last 50 years, but it has been at the expense of its people.

The future of Korean capitalism is tied up with the future of global capital. No national economy can escape that. But there are specific challenges for Korean capital too. The biggest and possibly the most immediate is what happens with North Korea. If and when the Stalinist-type regime falls there, Korean capital is no position to integrate the people of the north into the capitalist system of the south. The cost that West German capital and economy suffered when the Berlin Wall fell and Germany was united again was significant and held back one of the most successful capitalist economies for a decade. The disruption to Korean capital would be very much greater, especially if this should happen in this period of economic stagnation and political turmoil.

Then there is Korean capital’s longer term future. The slowing of world trade everywhere is damaging to Korean capitalism, but this slowdown appears to morphing into the end of the period of so-called globalisation that world capitalism has benefited from since the early 1980s. Regional trade agreements like TPP and TTIP are in the rubbish bin, thanks to Donald Trump, while he talks of tariffs on imports into the US and forcing American capital back to the US. The next global recession could be an even bigger hit to Korean capital than the last.

No comments:

Post a Comment