US GDP figures were revised down last Friday to -1% annualised growth from -0.1% on the first estimate. This was mainly due to inventories. Inventory depletion contributed -1.62% points to growth, compared with the advance estimate of -.57% pts. In other words, American businesses reduced production and ran down their stocks of unsold goods in early 2014 instead to meet demand. The consensus view is that businesses will have to restock this quarter and so the US growth rate will pick up now that the terrible winter is over. We shall see.

Even more interesting was the data released on profits. US corporations have enjoyed an explosion in profits since the Great Recession ended. Corporate profits as a share of GDP reached all-time highs (both before and after tax) in 2013. But in the first quarter of 2014, that changed.

Before tax corporate profits in Q1 fell absolutely on a year on year basis for the first time since the Great Recession. After tax, there was still some rise in profits but at one quarter of the pace of 2012.

I have argued before that there is a good correlation between the movement in the mass of profit and business investment (see http://thenextrecession.wordpress.com/2010/12/29/profits-and-investment-in-the-economic-recovery/). Indeed, US corporate profits growth began to slow before US business investment way back in 2003 and fell absolutely towards the end of 2005, while business investment did not drop until the Great Recession began in 2008. Also profits started to recover one year before investment did. Since the end of the Great Recession profit growth has dropped from its heady heights at the end of 2009 and has steadily slowed towards zero now. Business investment growth has followed a year later. So profits lead investment – they call the tune under capitalism. If that’s case, business investment could also start falling absolutely by this time next year.

Now it may be that the drop in profit recorded for Q1 2014 is just a blip caused by the bad weather that hit the US during the early part of 2014. This is what mainstream economists say. The consensus is that growth will recover sharply in the current quarter that we are now in and the second half of this year will see 3%-plus annualised growth. Again we shall see.

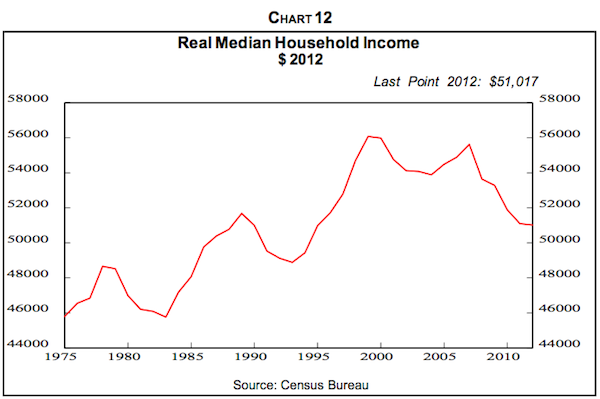

Since the Great Recession, American corporations have sucked up all the new value created by the labour force while average American households continue to take a hit on real income levels. The purchasing power of the majority of Americans has not only stagnated since the recovery began five years ago – it has actually declined. At $53,000, the median US household is more than $4,000 – or 7.6% – poorer in real terms than it was at the start of the recession in 2008, according to Sentier Research.

The great debate about inequality of income and wealth provoked by the book from Thomas Piketty

(see http://thenextrecession.wordpress.com/2014/05/24/piketty-data-and-the-scientific-method/)

has recently centred on whether inequality of wealth and income really has risen in the last 3o years in the US. It seems that Mark Carney, the governor of the Bank of England, reckons it has: “Within societies, virtually without exception, inequality of outcomes both within and across generations has demonstrably increased.” Whatever the evidence, it is clear that US inequality of income has sharply risen since the Great Recession ended, with the profit share rocketing and average real incomes falling.

The US now has a lopsided economy similar to that in the UK. During the first four months of this year, the sales of the top 1% most expensive US homes – those worth $1.67m or more – have increased by 21%, according to Redfin, the real estate group. It followed a gain of 35% in 2013 – led by the gilded San Francisco Bay area, where the priciest homes start at $5.35m. But sales of the bottom 99% of homes have fallen by 7.6% so far this year. The fall in average household incomes is reflected in falling sales at shops for the majority. At Walmart, the supermarket chain, revenues dropped by 5% in Q1 2014. At Sears Holdings, sales are down 6.8%, while the discount stores are getting higher sales as Americans search for bargains: the leading retail discounter’s sales rose 7.2%.

The US stock market hit yet another all-time high last week as cheap money from the Fed and expectations of further increases in profits encouraged rich investors and institutions to plough more cash into stocks and bonds. That will change if America’s profit explosion has really ended.

No comments:

Post a Comment