The world’s stock markets continue to make new all-time high index levels as central banks continue to pronounce that they will not push up interest rates for investing any time soon. The ECB has cut interest rates and is planning further credit easing measures. So is the Bank of Japan. And last week, the US Federal Reserve policy committee unanimously voted to hold off raising interest rates until late 2015 at the earliest. Only the Bank of England has hinted at raising its rate some time in 2015.

But while the world’s stock and bond markets are booming, the ‘real’ economy of output and incomes shows little sign of getting a proper head of steam. Last week, the International Monetary Fund (IMF) slashed its US growth forecast for 2014 from 2.8% it predicted at the beginning of this year to just 2% after a “harsh winter” led to a weak first quarter. It continued to forecast 3% real GDP growth in 2015, but given that it has now lowered its annual forecast for six times in row, that 3% may not survive. And also last week, the US Fed reduced its forecasts for real GDP growth this year from 2.8-3.0% to 2.1-2.3%. Again, like the IMF, it kept its forecast for 2015 intact at about 3.1-3.2%.

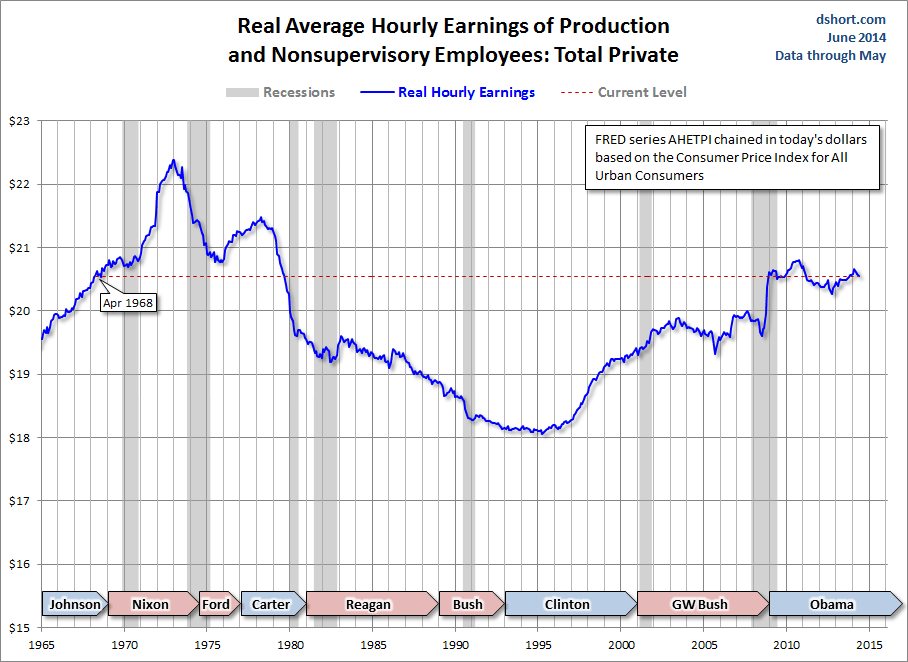

World stock investors may be doing well, but the majority of people are not. The IMF agreed that the US recovery from the Great Recession had been better than in many other developed economies. But it noted that the productivity growth was poor and reckoned that the labour market was weaker than suggested by the headline numbers for people out of work. Long-term unemployment was still high and many people are not even seeking work, which means they don’t register in the official jobless numbers. Real wages are stagnant (see graph below) and poverty is stuck at more than 15%. It even called for a hike in the US minimum wage to help boost spending!

In the UK, real wages are still falling. And a new report from the High Pay Centre found that the UK’s lowest average disposable income is amongst the worst in the whole EU even though Britain’s richest people enjoy some of the highest salaries. The top 20% of UK households have an average disposable income of £31,670 (€39,662, $53,785) a year, which puts them behind only Germany and France. However, the lowest 20% in this country have an average disposable income of just £5,506 – the poorest in western Europe!

“Simply, for the millions of people comprising the poorest fifth of our population, life is much worse here than it is for the poorest fifth in virtually every other north-west European country – countries we would like to think of as our equals,” stated the study. And this Piketty-style level of inequality is not going to be reduced. The UK’s Institute for Fiscal Studies predicts that, as the economy recovers, inequality will be ‘about the same’ as pre-recession levels by 2015-16.

Also, the Poverty and Social Exclusion project has found that the number of British households falling below minimum living standards has more than doubled in the past 30 years, despite the size of the economy increasing two-fold. Now 33% of households endure below-par living standards – defined as going without three or more “basic necessities of life”, such as being able to adequately feed and clothe themselves and their children, and to heat and insure their homes. In the early 1980s, the comparable figure was 14%.

Almost 18 million Britons live in inadequate housing conditions and that 12 million are too poor to take part in all the basic social activities – such as entertaining friends or attending all the family occasions they would wish to. It suggests that one in three people cannot afford to heat their homes properly, while 4 million adults and children are not able to eat healthily. 5.5 million adults go without essential clothing; 2.5 million children live in damp homes; that 1.5 million children live in households that cannot afford to heat them; that one in four adults have incomes below what they themselves consider is needed to avoid poverty and that more than one in five adults have to borrow to pay for day-to-day needs. 21% of households are behind with household bills against 14% in the late 1990s. More than one in four adults (28%) have skimped on their own food so that others in the household might eat.

Behind the failure to restore reasonable levels of economic growth since the Great Recession is a failure to invest by the capitalist sector, while public sector investment has been slashed in austerity measures (see my post, http://thenextrecession.wordpress.com/2013/09/17/nobodys-investing/). Capitalists are investing in the stock market but not in building homes for people. In the UK, housing starts have failed to keep up with population growth for the most part of two decades and is currently falling further behind.

Many smaller companies are not making a profit or are heavily in debt. The Bank of England has found that the percentage of companies that don’t make a profit reached 35% in 2011, the last year for which figures were available. This figure of loss-making firms has been steadily rising since 1998 when it was 23%. These are ‘zombie’ companies, just making enough to service their debts but having nothing to pay workers more or invest in new technology. No wonder UK productivity levels continue to slip (see my post, http://thenextrecession.wordpress.com/2013/12/04/cash-hoarding-profitability-and-debt/).

And in a great new paper to be delivered to the upcoming Rethink Economics conference in London next weekend

(http://www.rethinkingeconomicslondon.org/),

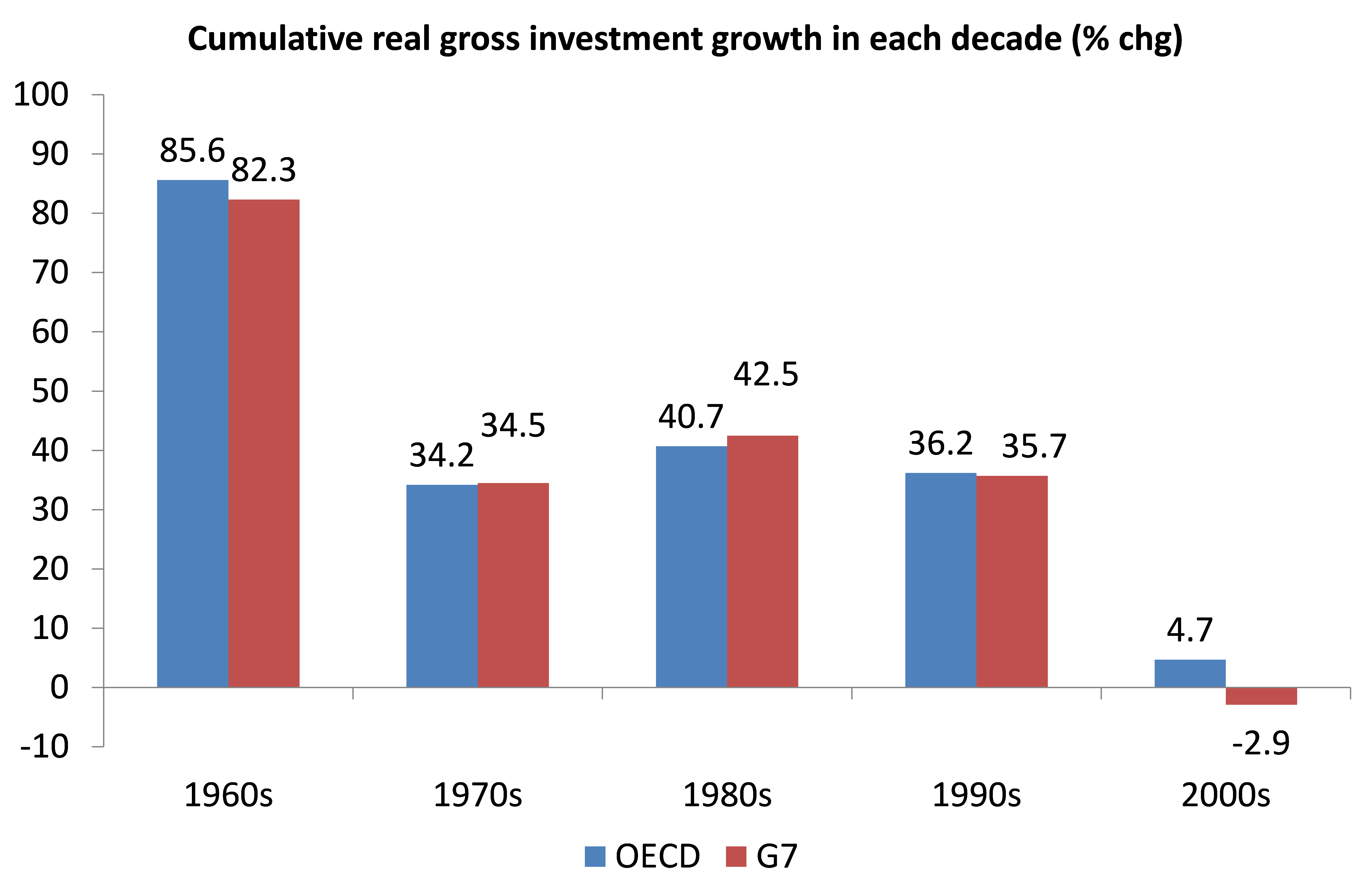

Michael Burke shows that this failure to invest is endemic to the major capitalist economies (The Great Stagnation as the Crisis of Investment). Burke shows that gross investment (both business and government and before depreciation) experienced the sharpest decline of all main components of GDP during the Great Recession. Such gross investment is down 5.2% in the OECD since 2008 and as a proportion of GDP it is down from 22% to 20%, reaching a new low since 1960.

Burke finds that real GDP growth in the OECD has been in a secular slowdown over a very prolonged period. Every successive decade has seen slower growth than the preceding one. But the slowdown in investment has been even more pronounced. While OECD GDP growth in the most recent decade to 2010 was little more than a quarter of the rate in the 1960s, gross investment growth is little more than one-twentieth of the 1960s. Indeed, in the top seven capitalist economies (G7), gross investment fell in absolute terms in the final decade to 2010.

Yet since 1960, consumption has risen as a proportion of GDP. So it has not been a Keynesian ‘lack of demand’ from consumers that has caused the slowdown in economic growth for the major economies, but capitalist sector investment. 21st century capitalists are good at speculating in financial assets and the stock market with cheap money, but are failing to accumulate in productive sectors where profitability just ain’t good enough for them.

No comments:

Post a Comment