Back in 2012, I presented a paper to the Association of Heterodox Economists entitled, A world rate of profit (a world rate of profit). Marx’s model of capitalism and its laws of motion are based on ‘an economy’, in other words, a world economy. Of course, there are still many barriers to the establishment of a world economy and a world rate of profit from labour, trade and capital restrictions designed to preserve and protect national and regional markets from the flow of global capital.

But in 2014, capitalism is much closer to be being a global economy than it was in 1914. So I tentatively suggested in that paper that, maybe, we could start to talk about a world rate of profit and start to measure it as an indicator of the underlying health and activity of capitalism globally.

In the paper I set out to try and measure a world rate of profit. I was not the first to do this. Minqi Li et al did some ground breaking work in their paper, Long waves, institutional changes and historical trends: a study of the long-term movement of the profit rate in the capitalist world economy, Long-Term Movement of the Profit Rate in the Capitalist World-Economy.

They developed a world rate of profit for a long period going back to 1870. For the 19th century, their study integrated just the UK, US and Japanese rates of profit. For the period after 1963, the authors brought in Germany, France and Italy, to make the G6. Among other things, Minqi Li et al found that their world rate of profit tended to fall between the late 19th century and the early 20th century and again tended to fall between the mid-20th century and the late 20th century. And they confirmed a rise from the mid-1980s to a peak in 1997.

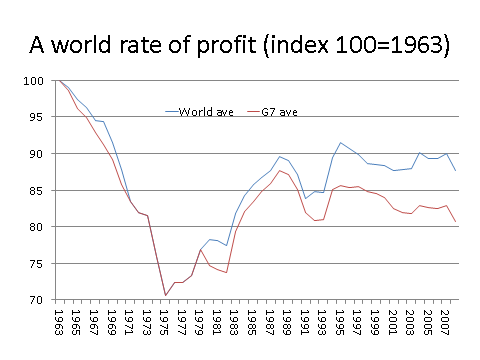

In my own study, I developed a world rate of profit that includes all the G7 economies plus the four economies of the BRIC acronym. So this includes 11 top economies which constitute a significant major share of global GDP. I use the extended World Penn Tables that David Zachariah used in his individual country study (see his paper, Dave Zachariah, Determinants of the average profit rate and the trajectory of capitalist economies, 4 February 2010, zacha10) I weighted the national rates for the size of GDP, although the crude mean average rate does not seem to diverge significantly from the weighted average. A proper measure of the world rate of profit would have to add up all the constant and variable capital in the world and estimated the total surplus value appropriated by global capital. This is really an impossible task. So weighted national profit rates are the only feasible way of getting a figure.

I found that there was a fall in the world rate of profit from the starting point of the data in 1963 and the world rate has never recovered to the 1963 level in the last 50 years. The world rate of profit reached a low in 1975 and then rose to a peak in the mid-1990s. Since then, the world rate of profit has been static or slightly falling and has not returned to its peak of the 1990s. And there was a divergence between the G7 rate of profit and the world rate of profit after the early 1990s. This indicates that non-G7 economies played increasing role in sustaining the world rate of profit. The G7 capitalist economies have been suffering a profitability crisis since the late 1980s and certainly since the mid-1990s.

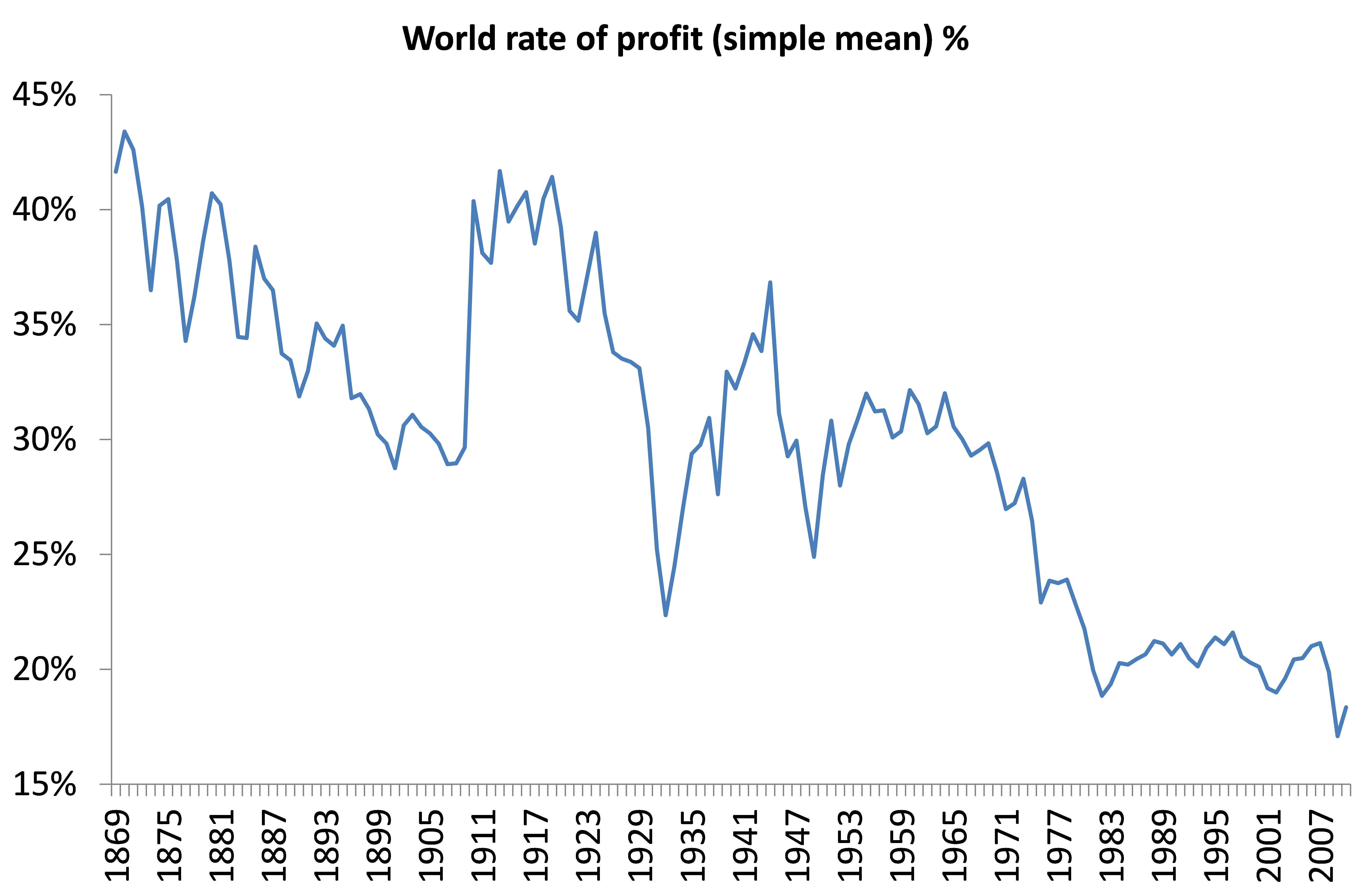

Now I have gone over all this again because there has been a brand new estimate of the world rate of profit in a new paper by Esteban Maito of Argentina (Maito, Esteban – The historical transience of capital. The downward tren in the rate of profit since XIX century). His paper presents estimates of the rate of profit on 14 countries in the long run going back to 1870. And Maito uses national historical data for each country not the Extended Penn Tables that I used. His results show a clear downward trend in the world rate of profit, although there are periods of partial recovery in both core and peripheral countries. So the behaviour of the profit rate confirms the predictions made by Marx about the historical trend of the mode of production. There is a secular tendency for the rate of profit to fall under capitalism and Marx’s law operates. Here is Maito’s world rate of profit back to 1869 (simple mean version).

Maito also finds, as Minqi Li and I do, that there was a stabilisation and even a rise in the world rate of profit from the early or mid-1980s up to the end of the 1990s, the so-called neoliberal period of the destruction of trade unions, a reduction in the welfare state and corporate taxes, privatisation, globalisation, hi-tech innovation and the fall of the Soviet Union. Again this seems to have peaked about 1997 (if China is excluded).

This is where Thomas Piketty comes into the story. In his book, Capital in the 21st century, now acclaimed by all the great and good in mainstream economics (see my posts, http://thenextrecession.wordpress.com/2014/04/15/thomas-piketty-and-the-search-for-r/ and http://thenextrecession.wordpress.com/2014/04/16/piketty-fest-continues-some-directions-for-the-reader/), and by many on the heterodox left, Piketty alludes to his book title as a follow-on from Marx’s Capital.

But he takes time out to insist that Marx’s law of profitability has proved to be fallacious. According to Piketty, “the rate of return on capital is a central concept in many economic theories. In particular, Marxist analysis emphasises the falling rate of profit – a historical prediction that has turned out to be quite wrong”. I won’t go into Piketty’s reasons for claiming why Marx was wrong here (I am saving that for my upcoming review of Piketty’s book in Historical Materialism). But the evidence from Maito, Minqi Li and myself makes a nonsense of Piketty’s conclusion about Marx’s law.

Piketty reckons that the net rate of return on capital (Piketty’s r) has been pretty static over the last 200 years at about 4-5%. This is crucial to his explanation of how capitalism can get into deep trouble. For him, it will be due to a rising share of profit going to capital and causing such extreme inequality that it threatens social instability. In contrast, Piketty does not see any crisis coming from falling profitability in the capitalist mode of production.

Piketty’s calculation that the net rate of return on capital has been steady is dubious even on his own definition of capital. But the real problem is that he defines capital as the same as wealth and thus includes residential property, even though houses are not means of production and do not ‘earn’ an income (unless they are owned by real estate companies and rented out). By including residential property in his calculations and concocting the ‘income’ from people’s homes as ‘rental equivalents’, Piketty ends up with completely distorted results for his r.

Moreover, here is some irony. Maito uses Piketty’s historical data for Germany to get a rate of profit for that economy. But Maito leaves out residential property and correctly categorises capital as the value of the means of production owned and accumulated in the capitalist sector. The result is not some steady r, but a falling rate of profit a la Marx. There a long-term decline, but with a rise from the 1980s to 2007 (which confirms my own estimates for Germany -

see http://thenextrecession.wordpress.com/2013/09/22/german-capitalism-a-success-story/).

Actually, Piketty’s r for Germany also falls from 1950 and then stabilises from the 1980s too. This is because, by 1950, landed property (also used in Piketty’s measure of ‘capital’) has disappeared in value and Germans generally have a much lower ownership of residential property compared to capitalist means of production as capital.

So Marx’s law of the tendency of the rate of profit to fall is again confirmed by this latest evidence on a world rate of profit. In my view, it remains the most important law of motion of capitalism, not Piketty’s r.

No comments:

Post a Comment