by Michael Roberts

Friday’s US jobs figures were a shock to the optimists about an accelerating recovery in the US economy. Yes, the unemployment rate fell to 6.7%, but for the wrong reason.

The percent of employed workers is rising because there are fewer and fewer workers in the labour force. Labour force dropouts are boosting the employed share percentage of a smaller labor force. The stats work like this: if 1000 are in the labour force with 70 counted as unemployed with 300 having given up looking for work, the unemployment rate is 7%. If the labour force stays at 1000, but 60 are now counted as unemployed because the number that has given up looking for work has risen to 310, the unemployment rate drops to 6%, yet the labour market gets worse. The participation rate, the labour force as a percent of the whole population, dropped to 62.8% in December, matching the October level that was the lowest since 1978 when large numbers of women were entering the work force for the first time. Against total population, the participation rate is stuck below 59%.

The very weak December jobs number, up only 74,000, meant that the 12-month average increase in jobs is 182,000, the same as it was in 2012. The year-over-year employment growth rate, a proxy for the trend, has dropped to 1.62%, down from a previous steady trend of over 1.7%. The broader unemployment rate includes everyone in the official rate plus “marginally attached workers” — those who are neither working nor looking for work, but say they want a job and have looked for work recently; and people who are employed part-time for economic reasons, meaning they want full-time work but went part-time because that’s all they could find. The ranks of part-time workers for economic reasons rose slightly to 7.77 million, but a bigger increase came in the marginally attached workers. The broader unemployment rate did not budge from 13.1%. And therre are currently more than 18.7 million people out of work for more than six months, or about 37% (after peaking at 40%).

The total number of jobs hit a peak of about 138 million in January 2008, one month after the start of the Great Recession. In the ensuing downturn, nearly nine million jobs disappeared. To date in the recovery, almost 8 million jobs have returned, leaving a gap just shy of 1 million. But that doesn’t account for changes in the population. If job growth had kept up with labour-force growth, the shortfall would be a lot bigger. If the population keeps growing at that same rate, and the US continues to add jobs near 2013’s pace, then the total number of jobs won’t get back to where they should be until 2019. If the pace picks up to 250,000 a month, the gap will narrow sooner, but the US economy hasn’t added an average 250,000 jobs or more a month since 1999.

And the US employed workforce has increasingly become part-time. Back 1968, only 13.5% of US employees were part-timers. That number peaked at 20.1% in January 2010. The latest data point, going almost four years later, is only modestly lower at 18.9%. The annual increase in part-time employment since the early 2000s has been steady but there has been a precipitous decline in full-time jobs from 2002, accelerating in the recession. Since 2002, the number of part-time jobs has risen 3m, while full-time jobs has decreased by a similar amount. Between full and part-time work, there was a conspicuous crossover during Great Recession.

In addition, most new jobs are in low-paid sectors like leisure and hospitality, retailing and fast food. Around 60% of the jobs lost during the last recession were mid-wage jobs, but 58% of the jobs created since then have been low wage jobs. Approximately one-fourth of all American workers make $10 an hour or less. According to the Working Poor Families Project, “about one-fourth of adults in low-income working families were employed in just eight occupations, as cashiers, cooks, health aids, janitors, maids, retail sales persons, waiters and waitresses, or drivers.” The US actually has a higher percentage of workers doing low wage work than any other G7 economy.

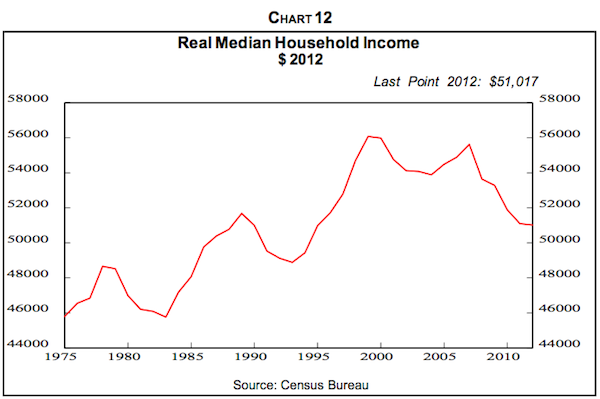

Real median household income, that of the household in the middle of the spectrum, is down 8.3% from the pre-recession 2007 level and off 9.1% from the 1999 all-time top. According to one survey, 77% of all Americans are now living paycheck to paycheck at least part of the time. The official estimate is that 15% of Americans live in poverty. But the highest wage in the bottom half of US earners is about $34,000. The number of Americans who earn between one-half and two times the poverty threshold is 146 million. Put simply, median income has slumped because a very large share of Americans can no longer find proper jobs.

The new generation of workers now have trouble finding full-time work and developing the skills needed for the transition to more stable, higher-paying employment. The longer the situation persists, the more difficult making up lost ground and lost time becomes. A recent study by the Brooking Institution (http://www.brookings.edu/~/media/Projects/BPEA/Fall%202013/2013b%20coibion%20unemployment%20persistence.pdf) found that both short-term and long-term unemployment increased sharply in 2008-9 during the Great Recession. But while short-term unemployment returned to normal levels by 2012, long-term unemployment has remained at historically high levels in the aftermath of the Great Recession. The longer one has been unemployed, the less likely one is to get a callback from an employer and job search effort also is likely to decline.

The last 30 years in the so-called neoliberal era has destroyed millions of reasonably paid, full-time secure jobs, especially in lower skilled manufacturing sectors. This has enable the capitalist sector to raise the rate of exploitation to counteract the fall in profitability experienced by most leading capitalist economies between 1965 and the early 1980s. Average income from employment has stagnated, even if average ‘compensation’ (health insurance, pensions etc) has risen somewhat. Over the same period, top layers of the employed workforce (chief executives etc), as agents of neo-liberal policies in the workplace, have seen spectacular rises in income and wealth.

The stagnation and recent collapse in average real incomes alongside the continued rise in the real incomes of the top 1% since the start of the Great Recession brings me to discuss the invaluable work of French economist, Thomas Piketty. Along with Emmanuel Saez and Anthony Atkinson (see my post, http://thenextrecession.wordpress.com/2013/07/14/the-story-of-inequality/), Piketty has provided seminal statistics on the inequality of income and wealth in the major economies. Piketty now has new book out (Capital in the 21st century) that analyses the changes in the inequality of income and wealth since the capitalist mode of production became dominant from the end of the 18th century. His 900 page book is partly summarised in this article http://www.voxeu.org/article/capital-back. and here is one chapter, piketc6. There are also some interesting reviews here: Piketty2013Cologne and here Milanovic on Piketty MPRA_paper_52384

According to Piketty, inequality is now approaching prewar levels. This rise in inequality is not due to better education for the top earners or even super star status like footballers. It is mainly due to a rise in income from the ownership of capital assets: “Economists used to believe that the ratio of aggregate wealth to income is constant over time, but it is not.” The wealth-to-income ratios of rich countries have been increasing since the 1970s. In the top eight developed economies, according to official national balance sheets, aggregate private wealth has risen from about two to three times national income in 1970 to a range of four to seven times today.

Figure 1. Private wealth / national income ratios, 1970-2010

Source: Authors’ computations using country national accounts. Private wealth = non-financial assets + financial assets – financial liabilities (household & non-profit sectors).

Piketty shows that the postwar decades – marked by relatively low capital wealth – appear to be a historical anomaly. High wealth-to-income ratios were the norm in Europe throughout the 18th and 19th centuries. Then the world wars, low saving rates, and a number of anti-capital policies provoked a large drop in private wealth, from six to seven times national income to about two times in the aftermath of World War II. The wealth-to-income ratios have been rising ever since, to the extent that they appear to be returning to their 19th-century levels. In the US, the wealth-to-income ratio has also followed a U-shape evolution, but less marked (Figure 2).

Figure 2. Private wealth / national income ratios, 1870-2010: Europe vs. USA

Source: Authors’ computations using country national accounts. Data are decennial averages (1910-1913 averages for Europe). Europe is the average of UK, France and Germany.

In his book, Piketty considers the reasons for this. In particular, he compared his model in his book, called Capital in the 21st century, with Marx’s model in his 19th century book, the first to be called Capital. Piketty says: “capitalists are concerned to accumulate each year more capital, by will power and perpetuation, or just because their life is already sufficiently high, … and then the ”return the capital must necessarily be reduced more and more and become infinitely close to zero, otherwise the share of income going to capital would “eventually devour the all of the national income”… So there is a “dynamic contradiction pointed to by Marx”. Capitalists must accumulate more to boost productivity “in a desperate attempt to fight against the downward trend in the rate of return”.

This is a bastardised version of Marx’s accumulation theory. Piketty really adopts a neoclassical version of diminishing returns as capital grows. The fall in the rate of return is not due to the inability of capitalists to exploit labour power enough but due to an ‘excess’ of capital. Piketty reckons that productivity growth is infinite and thus can compensate indefinitely for the decline in the rate of profit. That apparently is why Marx’s law of profitability proved wrong as capitalism grew over the last 150 years. But he also recognises that, as capital accumulates and the share of capital in national income rises, it threatens intensified class struggle.

So Marx was on the right lines, in a way. If only he had looked at the statistics, as Piketty has done. Marx had “a fairly anecdotal, unsystematic available statistics approach. In particular, it does not seek to know if the high capital intensity that he believes detected in the accounts of some manufacturing sectors is representative of the British economy in as a whole…this is most amazing in a book (Capital) dedicated for a large part to the question of the accumulation of capital. Marx makes no attempt to estimate the national capital stock despite the earlier work of Colquhoun in the years 1800-1810 or the later work of Giffen from 1870-1880…which is all the more regrettable as this would have allowed him to confirm to some extent his intuitions on the huge accumulation of private capital that characterizes the time, and especially to clarify his own model.”

Piketty is no Marxist or even an anti-capitalist economist. But he recognises the threat to the system that growing inequality is creating and he has glimmerings of an understanding of why inequality is endemic under capitalism. It is not the result of better skilled workers being paid more, but is caused by the division between income from the ownership of the means of production and income from selling your labour power. Inequality cannot disappear or even be reduced significantly without ending that division in the organisation of society. So the lost generation will stay lost.

No comments:

Post a Comment