Still more on the state of the world economy as we head into the second month of 2013. In previous posts, (The global crawl, The US – still crawling), I argued that the world economy was not slipping back into recession; but it was not recovering at the same rate as it had done in previous economic slumps like 1974-5 or 1980-2, 0r 1991-2, or 2001. The US economy was doing better relatively than Europe or Japan, but its growth at about 2% a year in real terms was sluggish and not enough to get the unemployment rate down fast, if at all.

I’ve used some higher frequency measures of economic activity in the past and we now have the latest figures for these measures up to January 2013.

First, there are the US purchasing managers indexes (PMIs) for manufacturing and services sectors. These indexes are surveys of activity done by the Institute of Supply Managers (ISM). I have constructed a combined ISM manufacturing and services index. The latest data show that the US corporate sector is still expanding, but still well below what can be called a boom level, as seen last in 2004.

An even more frequent activity measure is that by the Economic Cycle Research Institute (ECRI), which claims it is a leading business cycle authority and has an ‘unmatched ability’ to forecast economic turning points – something disputed by its critics. Anyway, its weekly indicator tells much the same story as the ISM index, although the recent period of data suggests some small acceleration of activity.

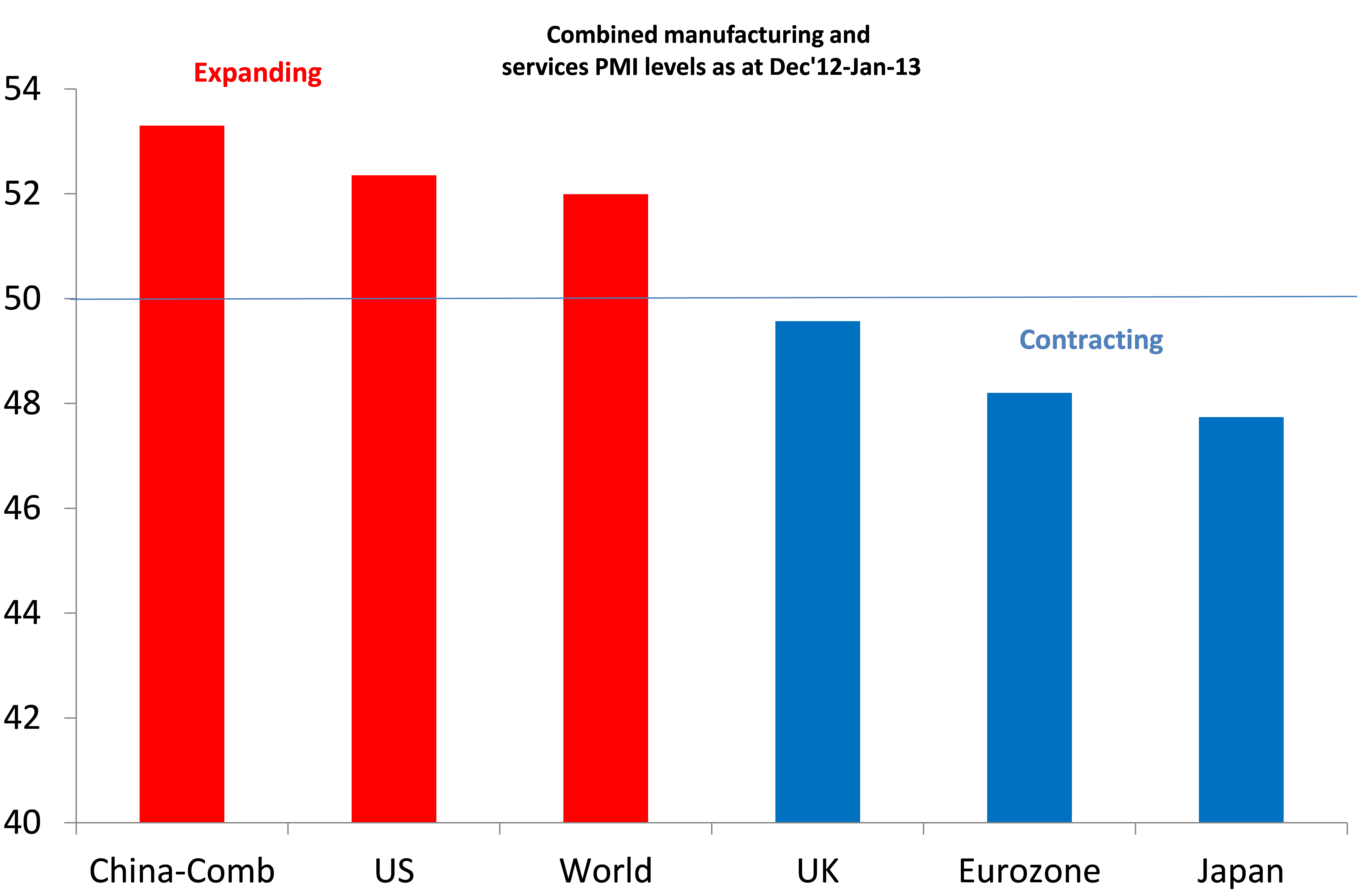

But what about the rest of the world? Well, the PMIs for December and January show that the world as whole is still expanding, with China and the US leading the way, while Europe and Japan are contracting (a score of 50 is the benchmark).

Another measure is that provided by Doug Short (see http://advisorperspectives.com/dshort/updates/Big-Four-Economic-Indicators.php). Short combines four data series for the US: industrial production, real retail sales, personal income and employment, to develop an index to gauge whether economic recession is imminent. The idea comes from the St Louis Federal Reserve. This index shows that the Great Recession was much deeper than the closest contender, the 1973-1975 recession. Recovery ensued after mid-2009 but a close look at the average shows a clear slowing of the trend in 2012. It took five years to get back to the previous peak in this index after the 2001 recession. After five years since the previous peak, this time the index is still 2% short. It’s a crawl.

No comments:

Post a Comment