Financialisation’ has been promoted by heterodox economists as the cause of the iniquities and failures of modern capitalist economies. Now an additional theory has been offered: ‘renterisation’. In a recent long article in the British Financial Times, its well-known economic columnist, Martin Wolf, offered this concept as the explanation of low productivity growth, rising inequality and the mountain of debt in the major economies.

Wolf reckons that capitalism has been “rigged” by monopolistic economic powers. “So why is the economy not delivering? The answer lies, in large part, with the rise of rentier capitalism. In this case “rent” means rewards over and above those required to induce the desired supply of goods, services, land or labour. “Rentier capitalism” means an economy in which market and political power allows privileged individuals and businesses to extract a great deal of such rent from everybody else…. While the finance sector is an important part of this monopolistic development, so that ‘financialisation’ has enabled monopoly sectors to create their own profits (if often illusory) and generate financial crashes, the real enemy of successful capitalism is “the decline of competition”. Wolf then cites all the recent empirical evidence of this ‘renterization’ of capitalism: market concentration; rising monopolistic profit mark-ups and ‘super star’ companies like the FAANGS making “monopolistic profits”.

But does this theory hold as the main reason for poor economic growth, rising inequality and financial crashes? Is it monopoly capitalism that is the cause, not the contradiction of capitalism as a whole? Well, let me remind readers of the empirical evidence for the renterisation theory. I have recounted that in previous posts and the evidence is doubtful at best. For example, you would expect the biggest profit mark-ups to be achieved by the ‘monopoly’ giants – in fact the data show it is the smaller companies that get higher mark-ups.

Again, low productivity growth appears to be much more closely correlated with low investment and in turn with low profitability, not with monopolisation. The biggest slowdown in productivity growth in the US began after 2000, as investment in productive sectors and activity dropped off. It is a fall in the overall profitability of US capital that is driving things rather than any change in monopoly ‘market power’. Again, for example, evidence shows that the ‘rent-seekers’ appear to have played no role in the low investment rate of the Eurozone: it’s just low profitability there. But such evidence is not convenient because it suggests that the cause of low productivity growth is due to contradictions in capitalist accumulation. It is more encouraging to argue that if profits are high, then it’s ‘monopoly power’ that does it, not the exploitation of labour in the capitalist mode of production. And it’s monopoly power that is keeping investment growth low, not low overall profitability.

Brett Christophers from the University of Uppsala in Sweden has published an important piece of work on renterisation (with a book to follow). Christophers rejects the term ‘financialisation’ as a cause of the current malaise in capitalist growth. Finance is too narrow a cause; because rents are being extracted in many other sectors like real estate. Christophers argues that “renterism’ in its various guises is today a significant, even dominant, dynamic, in contrast to during the period preceding the neoliberal turn.” He reckons the British economy “has been substantially rentierized.” Christophers renterization Christophers offers what he calls a hybrid definition of rent that tries to combine Marx’s view of rent coming from the monopoly ownership of a non-produced asset (land, minerals etc) with the mainstream view of “excess payment” over and above efficient production, namely payment above the ‘marginal productivity of labour or capital’.

I’m not sure that this hybrid definition is useful. It appears to fudge the key issue that Marx makes about how rent emerges: namely that it comes from the appropriation of surplus value created in the exploitation of labour in the production of commodities. For Marx, rent comes from the ability of monopoly owners of non-produced assets to retain surplus-value from being merged with the competitive process of capital flows. For Marx, ‘productive capitalists’ as appropriators of surplus value from the exploitation of labour are forced share some of that surplus value with owners of non-produced resources (rent) and finance (interest). Rent and interest are part of total surplus value created in the production of commodities. Value and surplus value must first be created by the exploitation of labour power. Then the surplus value gets redistributed and those with some monopoly power can extract a part of that surplus value in rent. “Excess payment’ over ‘efficiency’ implies that there is an acceptable payment to capitalists for exploiting labour power to benefit productivity and thus ignores these class relations.

Marx considered that there were two forms of rent that could appear in a capitalist economy. The first was ‘absolute rent’ where the monopoly ownership of an asset (land) could mean the extraction of a share of the surplus value from the capitalist process without investment in labour and machinery to produce commodities. The second form Marx called ‘differential rent’. This arose from the ability of some capitalist producers to sell at a cost below that of more inefficient producers and so extract a surplus profit. This surplus profit could become rent when these low cost producers could stop others adopting even lower cost techniques by: blocking entry to the market; employing large economies of scale in funding; controlling patents; and making cartel deals. This differential rent could be achieved in agriculture by better yielding land (nature) but in modern capitalism, it could be through a form of ‘technological rent’; ie monopolising technical innovation.

Undoubtedly, much of the mega profits of the likes of Apple, Microsoft, Netflix, Amazon, Facebook are due to their control over patents, financial strength (cheap credit) and buying up of potential competitors. But the renterization explanation goes too far. Technological innovations also explain the success of these big companies, not just monopoly power. Moreover, by its very nature, capitalism, based on ‘many capitals’ in competition, cannot tolerate any ‘eternal’ monopoly, namely a ‘permanent’ surplus profit deducted from the sum total of profits divided among the capitalist class as a whole. The battle among individual capitalists to increase profits and their share of the market means monopolies are continually under threat from new rivals, new technologies and international competitors. Take the constituents of the US S&P-500 index. The companies in the top 500 have not stayed the same. New industries and sectors emerge and previously dominant companies wither on the vine.

The history of capitalism is one where the concentration and centralisation of capital increases, but competition continues to bring about the movement of surplus value between capitals (within a national economy and globally). The substitution of new products for old ones will in the long run reduce or eliminate monopoly advantage. The monopolistic world of GE and the motor manufacturers of the 1960s and 1990s did not last once new technology bred new sectors for capital accumulation. The world of Apple will not last forever.

‘Market power’ may have delivered rents to some very large companies in the US, but Marx’s law of profitability still holds as the best explanation of the accumulation process. Rents to the few are a deduction from the profits of the many. Monopolies redistribute profit to themselves in the form of ‘rent’ but do not create profit. Profits are not the result of the degree of monopoly or rent seeking, as neo-classical and Keynesian/Kalecki theories argue, but the result of the exploitation of labour.

Moreover, rents are no more than 20% of value-added in any major economy; financial profits are even smaller a proportion. Moreover, the rise of renterism in the recent period is really a counteracting factor to the decline in the profitability of productive capital.

There is another definition of a rentier economy based on Marx’s explanation of the division of surplus value into profits, rent and interest that is relevant. There are national economies where the capitalist sector appropriates much surplus value in the form of interest, dividends and profits through non-productive services like finance, insurance, and so-called business services. Britain is one of these ‘rentier’ economies; Switzerland is another – both much more so than the likes of Germany or Japan, or even the US, where the appropriation of surplus value is still predominantly through the direct exploitation of labour power (both domestically and abroad).

As the spoke person for the City of London recently said, “London is the capital of capital”. The City of London delivers a considerable inflow of income to the UK economy through its sale of financial services, bank interest and profits and allied business services. The UK financial sector plus real estate (oligarchs want to live in London) and other business services contributes a much larger proportion of GDP and cross-border income inflows to the balance of payments than most other major economies.

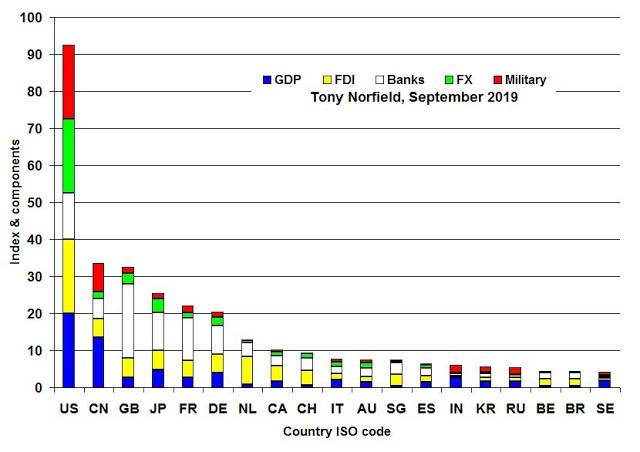

Tony Norfield has developed a power index of imperialist economies and in that index, the US leads, but it is followed by the UK. If you strip out of the index, the military and GDP constituents, Britain is way ahead of all as a rentier economy (at least in absolute dollar terms).

I did a little analysis from the WTO of commercial services exports of different countries. The export of financial, insurance and other business services as well royalties and fees collected could be considered a measure of rentier exports if you like. On this measure global rentier exports totalled $2trn in 2013. The US received export income of $365bn, or 18% of world rentier income; the UK obtained $180bn, or 9%, while Japan received $78bn or 4% and Germany had no cross-border rentier income at all. US GDP in 2013 was $16.7trn, the UK’s was $2.7trn. So the UK received rentier export income equivalent to 7% of its GDP while the US got just 2% of its GDP from rentier exports. In this sense, we can talk about a rentier economy and Britain as the poster child. But that makes Britain particularly vulnerable to financial crashes.

Joseph Stiglitz and Martin Wolf reckon that what is wrong with capitalism is that ‘financialisation’ and monopoly rentier interests have ‘rigged’/ruined the ‘progressive’ features of capitalism, namely its ability to expand the productive forces harmoniously for all. As Wolf puts it: “We need a dynamic capitalist economy that gives everybody a justified belief that they can share in the benefits. What we increasingly seem to have instead is an unstable rentier capitalism, weakened competition, feeble productivity growth, high inequality and, not coincidentally, an increasingly degraded democracy. Fixing this is a challenge for us all, but especially for those who run the world’s most important businesses. The way our economic and political systems work must change, or they will perish.”

But as LSE professor Jerome Roos perceptively pointed out in the British left journal, New Statesman, “By opposing the “bad” capitalism of the unproductive rentier to the “good” capitalism of productive enterprise, however, the conventional liberal narrative overlooks the fact that the two are inextricably entwined. Such thinking relies on an idealised but entirely theoretical version of capitalism that is pure, uncorrupted and far more benign than it is, or has ever been or, in all likelihood, ever will be. The reality is that the concentration of wealth and power in the hands of a few privileged rentiers is not a deviation from capitalist competition, but a logical and regular outcome. In theory, we can distinguish between an unproductive rentier and a productive capitalist. But there is nothing to stop the productive, supposedly responsible businessperson becoming an absentee landlord or a remote shareholder, and this is often what happens. The rentier class is not an aberration but a common recurrence, one which tends to accompany periods of protracted economic decline.(my emphasis)”.

In the past, this blog has posted overwhelming empirical evidence that the key to understanding the movement in productive investment remains in the underlying profitability of capital, not in the extraction of rents by a few market leaders, as Wolf and others suggest. If that is right, the Keynesian/mainstream solution of regulation and/or the break-up of monopolies (even if it were politically possible) will not solve the regular and recurrent crises in production and investment or stop rising inequality of wealth and income.

No comments:

Post a Comment